Do you have an ACAPayments listing on your credit report?

ACAPayments is a debt collection agency based in Massachusetts with nearly 60 years of history behind it, and a steadily increasing number of customer complaints in recent years. If you see ACAPayments as a collection account on your report, your immediate reaction might be to address it as an old matter.

However, the likelihood of it being truly old news is low. In this article, we will explore what ACAPayments is, what we can infer from the data, and how consumers have been responding to it.

A study conducted by U.S. PIRGs found that 79% of credit reports contain some error or inaccuracy. That is not a fact; it is a reality, a reality of how debt collectors submit data en masse and credit reporting agencies process that data with little verification. If ACAPayments is on your report, your initial response should not be to pay it. Your initial response should be to verify its accuracy.

What is ACAPayments?

ACAPayments is not actually a company. It is the online payment portal for Action Collection Agencies, Inc., which operates as a third-party debt collector under the trade name Action Collection Agency of Boston. ACAPayments is essentially a website address, acapayments.com, which leads to a PayStream-powered payment page found at clientaccessweb.com.

Below, you can find some key information about ACAPayments.

Date Founded: April 15, 1967 (58 years old)

Better Business Bureau (BBB) Rating: A- (Not BBB Accredited)

Chief Executive: Jay E. Gonsalves (President and CEO since 1991)

Analyzing ACAPayments and Action Collection Agencies

Action Collection Agencies, Inc. was first organized in 1967 and reorganized in 1991 when the company was purchased by its current president and CEO, Jay Gonsalves.

The company specializes in debt recovery for the healthcare industry but also offers collection services for financial services, utilities, education, retail, commercial, and debt portfolios. Action Collection Agencies has a single office location at 16 Commerce Boulevard, Unit #4, in Middleboro, Massachusetts (about 40 minutes south of Boston) and employs around 50 individuals.

Action Collection Agencies holds several industry certifications, including SOC 2 Type II, PCI, and HITRUST CSF. The company is also certified under the ACA International Blueprint Quality Management System.

Now, let us move on to the consumer complaint data to see if there are any red flags.

What the Consumer Complaints Say

Better Business Bureau (BBB) Complaints Have Nearly Tripled

The clearest trend in the recent history of ACA is the surge in new complaints filed with the Better Business Bureau.

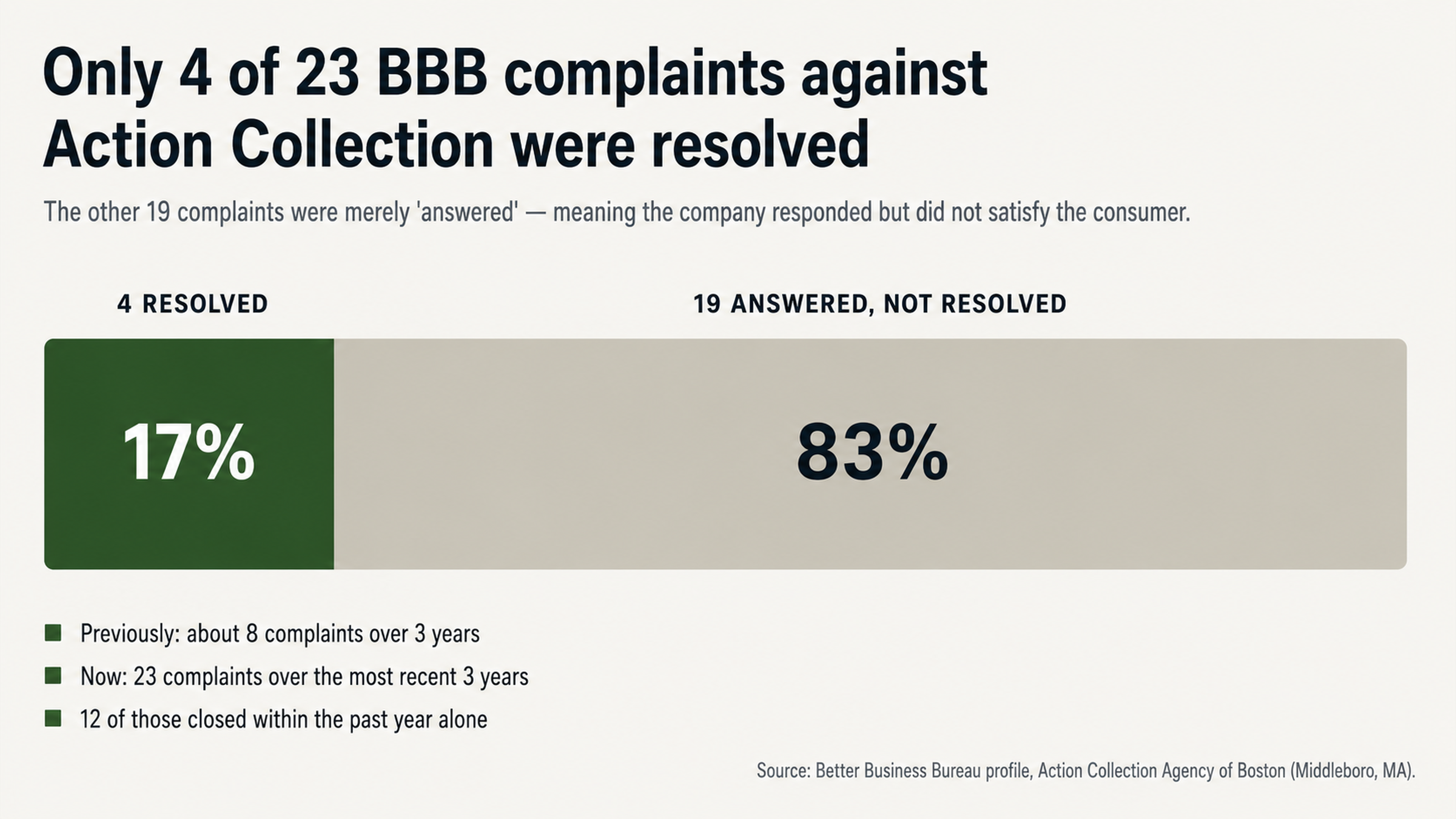

In previous versions of the Action Collection Agencies BBB profile, you could see that the company had attracted around 8 complaints over a three-year period. The current BBB profile for ACA now shows 23 to 24 complaints over the most recent three-year period, with 12 of those complaints closed within the past year alone. That represents nearly a threefold increase.

The resolution status of those complaints tells an even more compelling story. Of the 23 complaints filed, only 4 of them were classified as “resolved” by the BBB. The other 19 complaints were merely “answered,” which means the company responded to the complaint but failed to resolve it satisfactorily in the eyes of the consumer.

A resolution rate of only 17% is not indicative of a good faith effort to resolve customer complaints. It is indicative of a company going through the motions. If this is how they handle complaints, you can’t expect them to give your complaint any special treatment. They don’t have an incentive to make you happy. They have an incentive to make you comply.

Patterns in Complaints Against Action Collection Agency

Complaints to the BBB suggest a pattern of behavior. There are consumers who report leaving voicemails without letters. There are those who say they’re being contacted about debts they don’t remember or don’t think they owe. And there are those who claim that what ACA says they owe doesn’t match what their insurance company says they owe.

In one 2025 complaint, a BBB user indicated that she was attempting to assist a developmentally disabled family member who was making payments of just $10 a month when a $20 payment was not applied. “I question if someone is trying to scam my disabled son,” the complainant wrote.

A 2025 complaint from a different user indicated that when they called the original creditor (a hospital), they were told there was no outstanding balance even though ACA was trying to collect the debt.

Yet another 2025 complaint describes calls where “my phone rings for less than a second then instantly goes to voicemail and leaves me an automated message.” The complainant described the approach as “very predatory.” These aren’t isolated incidents. These are patterns in the complaints.

Federal Lawsuits Against Action Collection Agency

In addition to complaints, ACA has been a defendant in federal lawsuits, including FDCPA actions.

The Suarez Class Action

The largest single case is a class-action suit called Suarez v. Action Collection Agencies, Inc. (Case No. 1:18-cv-22337-RNS). It was filed June 12, 2018, in the U.S. District Court for the Southern District of Florida. According to the class-action complaint, ACA sent “thousands of unlawful collection letters to Florida consumers,” each of which contained the same FDCPA violations.

The specific problem the complaint identified was a “Notice of Important Rights” that ACA includes in collection letters. The plaintiff contends that the notice “falsely describes” the rights afforded consumers under the FDCPA by suggesting that they must send written notifications that are post-marked within 10 days.

The suit alleges violations of 15 U.S.C. Section 1692e(5) (threatening to take any action that cannot legally be taken) and 15 U.S.C. Section 1692e(10) (using any false representation or deceptive means to collect or attempt to collect any debt). If a debt collection agency is sending letters with built-in violations of federal law, that is a serious issue.

This is not a matter of someone at the agency making a mistake. This is a matter of the agency using a template that contains a violation. If that is the case, consumers would be right to question whether anything else in the letter, like balance information, is accurate.

Other Federal Lawsuits and Lack of Regulatory Action

ACA has been a party to other federal cases. The company successfully moved for summary judgment in Deleon v. Action Collection Agency of Boston (Case No. 1:2017cv08899, S.D.N.Y.) in May 2018.

Other cases include Witherell v. Action Collection Agency of Boston (Case No. 1:15-cv-14130-PBS) and Reed v. Action Collection Agency, Inc. (Case No. 3:17-cv-01598). No CFPB, FTC, or state attorney general enforcement actions were found. That does not mean the company has not committed any violations.

It means that the relevant regulators have not acted. There is a big difference between those two things. The absence of enforcement is not proof of absence of violations. It is just proof that regulators have not gotten involved. That bar is much lower than a lot of consumers realize.

Why ACAPayments Confuses Consumers

ACAPayments specifically confuses consumers in one way. When you visit acapayments.com, you’ll see that this website redirects to a third-party payment processor, clientaccessweb.com. There’s no landing page that explains what ACA is or does. There’s no link to consumer rights resources. There’s no information about FDCPA rights or how to dispute a debt.

acapayments.com has a 1.4-star rating (out of 5) on the ScamAdviser website. Some consumers have complained that they can’t see their payment history on the portal, that payments are debited from their accounts but never credited to their debt accounts, and that they can’t reach anyone who can help resolve the issue.

This is the online front door of the ACAPayments company, and it’s building distrust rather than trust.

Phone-First Contact and Missing Documentation

Several consumers have reported that the first time they heard about an ACA collection was through phone contact rather than mail. This theme repeats itself in a series of 2025 BBB complaints about ACAPayments.

Here’s an example: “I am receiving voicemails with no written communication. I do not owe anyone money as far as I know. With all the scam advisories for this company, I will not return phone calls.”

Starting with phone contact disadvantages consumers and advantages the debt collector. When a collector contacts you by phone first, they are in control of the communication. The consumer doesn’t have a paper trail to review, dispute, or attach to a complaint. And that’s why it’s almost never a good idea to engage with a debt collector by phone.

Why Disputing ACAPayments Works

The Paper Trail is Your Leverage

ACAPayments collects both purchased debt and healthcare debt.

When debts are sold or resold, sometimes the paperwork that should follow them does not. The original contract, the full payment history, the chain-of-title paperwork, these records are often lost, incomplete, or not transferred properly. Each resale introduces the risk of a paperwork gap, and each paperwork gap is a potential deletion opportunity.

Under the FCRA, a debt reported to a credit bureau must be verified. If you dispute the debt and the collection agency cannot verify it within the dispute period, the CRA must delete it. This is not a loophole or trick. It’s how the system is designed to protect consumers from reporting errors.

The business model of debt collection also plays to your advantage here. Debt buyers purchase debts for a few cents on the dollar. Their business model depends on collecting as many debts as possible in as short a time as possible. They don’t have time to maintain accurate paperwork. So when you force them to verify a debt by disputing it, they may not have time to respond.

Why Paying First Fails

Paying off a collection seems like the way to make it go away, but it usually isn’t. When you pay a debt collection, you’re changing its status from “in collections” to “paid.” But the collection itself will still appear on your credit report for years. In some cases, making a payment can even re-age the debt, extending the reporting period. Instead, you should start with a dispute.

If any information about the debt is inaccurate, balance, date, owner, validity, you have grounds for deletion. Consumer complaints to the BBB saying the original creditor stated there was no amount due demonstrate that verification issues are real here. They are on record.

The Industry Insider Perspective

A CEO Who Writes the Rules He Plays By

Jay Gonsalves is the president of Action Collection Agencies. He also serves as the chair of ACA International’s Federal Affairs Committee, which oversees the debt collection industry’s lobbying efforts at the federal level.

In the past, he served as the president of ACA International itself in 2008 and 2009 and was named the organization’s Speaker of the Year as recently as 2025. ACA’s president thus oversees the company’s debt collection activities while also playing a key role in writing the rules that apply to those activities.

This is not against the law. However, it is a structural conflict that consumer advocates need to be aware of. The debt collection industry’s approach to self-regulation is being set by a person whose company has seen its BBB complaint rate triple in three years.

What Poor Reviews Cannot Do to a Collector

Unlike other businesses, which rely on consumer satisfaction to drive revenue, debt collection agencies are paid by the original creditor or current debt owner. This means that negative BBB ratings, Google reviews, and complaints cannot affect a debt collector’s bottom line because consumers do not choose their debt collector, one is assigned to them.

This is also why simply damaging a collector’s reputation will never change their behavior. The only language they understand is that of formal complaints, regulatory challenges, and legal liability. Consumers have more power in this situation than they think, but only if they use the tools the law gives them instead of relying on a company’s incentive to protect its reputation.

Conclusion

ACAPayments is the online bill pay interface of a debt collection agency whose BBB complaint rate has tripled in three years, whose form collection letters are the subject of a federal lawsuit claiming they are deceptive, and whose president also plays a leading role in the industry’s federal lobbying efforts. The fact that the company is certified, accredited, and has been around for a while does not shield consumers from the trends in its complaint record.

Whether you actually owe the money Action Collection Agency says you do should never be taken for granted. No debt showing on your credit report is valid unless the complete documentation for that debt is available. If the documentation is incomplete, incorrect, or cannot be verified, the law says it must be deleted.

What You Should Do Next

If you see ACAPayments on your credit report, do not call the phone number on the collection letter you received.

Do not go to the website listed and make a payment online to make the debt go away. Not only can these steps confirm the debt if it is in question, but they can also restart the clock for credit reporting and give up your most powerful option for dealing with the situation before you have even had a chance to use it.

Instead, consider partnering with a reputable credit repair firm that understands how to challenge collection accounts properly.

At FightCollections.com, we start with a thorough analysis of your credit report to identify all of the errors and unverifiable information, then file formal disputes that force collectors to prove their claims or have them removed.

The system is rigged in favor of consumers who know how to work within it. The debt collectors are hoping you do not know that. But now you do.