Account Services Collections, Inc. is a Texas-based debt collection agency that has been collecting from consumers since 1970.

While it has a few other names that it goes by that may confuse consumers trying to identify who is reporting on their credit report.

Here is the basic information about this agency:

What the research reveals

Although it has an A+ rating with the Better Business Bureau, it has an abysmal rating when looking at the reviews from actual consumers that have dealt with them. It has a 1.1-star rating on Google Reviews, which is one of the lowest-rated debt collection agencies we’ve come across.

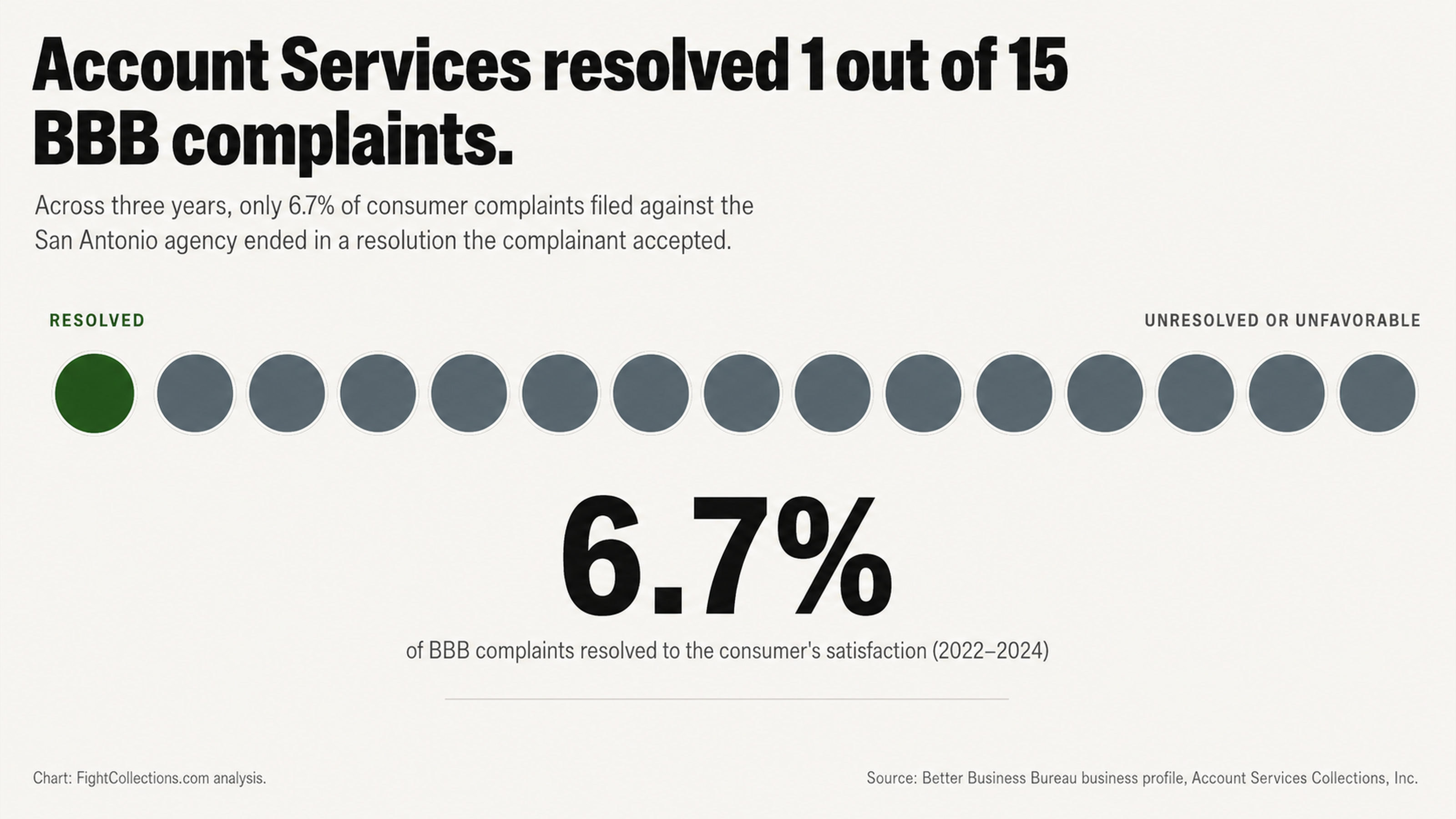

Even more concerning is the number of complaints that have been filed against them through the Better Business Bureau. Over the last three years, 15 complaints have been filed against Account Services. Of those complaints, only one has been resolved to the consumer’s satisfaction. That means it has successfully resolved only 6.7 percent of the complaints filed against them.

It has also been sued in federal court multiple times for violating consumers’ rights while attempting to collect a debt. One example is the case Traylor v. Account Services Collections Inc., (Case No. 3:2018cv03352). It has been accused of:

Failing to identify the current creditor

Attempting to collect a debt that the consumer claims they do not owe

According to consumer advocacy attorneys, Account Services has a history of making threats to consumers.

How Marcus discovered the problem

Marcus is a 34-year-old project manager in Houston. He was preparing to apply for a mortgage, so he decided to request copies of his credit reports to review for any errors. That is when he found the problem.

There was an $847 collection on all three of his credit reports from Account Services for a medical bill that was two years old. The problem was, Marcus had insurance that covered the procedure. He had never received a bill for the procedure and never received any correspondence from a collection agency. He certainly never agreed to pay Account Services for the procedure. So, why was it on his credit report?

Marcus’ story isn’t unique. In fact, researchers have found that 79 percent of credit reports contain some sort of mistake or serious error. This isn’t a coincidence. This happens because collection agencies will purchase debts from original creditors without verifying the information. Then, they report the information to the credit bureaus without verifying its accuracy.

The pressure campaign begins

It didn’t take long for Marcus to start receiving calls from Account Services. Within days of pulling his credit report, his phone began ringing. Sometimes he would receive multiple calls in a single day.

When he answered the phone, the representative from Account Services would tell him that he owed the debt and that he needed to pay it immediately to avoid any further damage to his credit report.

This is a common tactic that collection agencies use. They will attempt to create a sense of urgency for consumers to pay a debt in hopes that they won’t take the time to validate it. The reality is, there is rarely an urgency to pay a debt. Once a debt has been reported to the credit bureaus, paying it today versus paying it a month from now isn’t going to make a difference in the amount of damage it’s causing to your credit report.

One consumer filed a complaint with the Better Business Bureau after receiving 23 phone calls, 13 text messages and three letters attempting to collect on a single debt. Another consumer complained that when they asked to be removed from their call list, the representative responded by saying, “Never.”

Why paying first can backfire

The paid collection trap

Marcus’ initial reaction was to pay the debt and be done with it. He was applying for a mortgage and didn’t want the debt to affect his credit score. Luckily, he decided to do some research before paying the debt.

If you pay a collection account, you are essentially admitting that you owe it, and the status will be updated to reflect that it is a paid collection. The problem is, the paid collection will remain on your credit report for seven years from the original delinquency date. You’re paying for the debt, but the damage on your credit report remains.

This can be especially troubling when dealing with a collection agency like Account Services that has such a low consumer satisfaction rating. Many consumers have complained that the debts that Account Services is attempting to collect are debts that should have already been paid by their insurance provider. Others have claimed that they paid the debt to the original creditor years ago. Others have said they never incurred the debt in the first place, so why would they pay it?

What collection agencies don’t want you to know

Collection agencies like Account Services have a lot of power when it comes to information. Not only do they have access to databases and the documentation for the original account (in some cases), but they also have the resources to defend themselves if necessary.

There’s something else that collection agencies don’t want you to know — many of the debts they’re attempting to collect can’t be validated.

When a debt collection agency purchases a debt from an original creditor, they may only receive very basic information. They may receive the person’s name, address and the amount that they owe, but they may not receive much of the documentation that proves that the person actually owes the debt. They may not have a copy of the original contract or the monthly statements that were sent to the consumer. They may not have proof that the debt was not paid. They may not even have documentation that proves they own the debt.

Consumer law firm Credit Glory explains their experience with Account Services: “Their aggressive approach to debt collection is likely a significant factor behind the negative feedback… many reviews state that they are untrustworthy, often making a negotiation deal and then not following through.”

The strategic response

Choosing silence over engagement

After researching his options, Marcus decided that he was going to stop answering the phone when Account Services called. While this may seem like an unproductive approach, it can actually be a good strategy when dealing with a collection agency.

Every time you speak with a collection agency on the phone, it provides them the opportunity to gather more information from you that can make it easier for them to collect the debt. They may be able to record your conversation, which can be used at a later date. They may be able to get you to admit that you owe the debt, which can make it more difficult for you to dispute later. They may be able to get you to provide your personal financial information, such as where you work or your bank account information, which can make it easier for them to collect the debt.

Instead of speaking directly with a collection agency, you should work with a professional who has experience in these situations and knows how to protect your rights. Do not provide a collection agency with any information about your personal finances, including where you work or your bank account information. Do not admit that you owe the debt or agree to a payment plan. Instead, allow a professional to communicate with the debt collection agency on your behalf.

Bringing in professional help

Instead of continuing to deal with Account Services directly, Marcus decided to reach out to a credit repair company for assistance. Sometimes bringing in a third party can go a long way in dealing with a debt collection agency. Not only can they communicate with the agency on your behalf, but they also have the resources and knowledge to help you protect your rights as a consumer.

When you enlist the help of a professional to deal with a debt collector, it sends a message that you will not be pushed around. You will not be taken advantage of. Many debt collection agencies will become less aggressive in pursuing you once they find out you have professional representation. They may even be more willing to remove the debt from your credit report to avoid having to deal with further disputes.

Keep in mind that having a credit repair company request information about the debt multiple times will not affect your credit any more than you requesting it.

The dispute process in action

Demanding validation

The credit repair company began by disputing the Account Services collection with all three credit bureaus. They requested that Account Services validate the debt by providing documentation that proved Marcus owed it.

The Fair Credit Reporting Act requires that when a consumer disputes information on their credit report, the furnisher of that information must investigate and verify it. They have 30 days to complete the investigation. If they are unable to verify the information or fail to respond within the allotted timeframe, the credit reporting agency must remove the disputed information from the consumer’s credit report.

One of the most common complaints about Account Services is that they’re unable or unwilling to provide documentation to consumers who request it. Here are a couple of examples of complaints that were filed with the Better Business Bureau:

“I am not liable for this debt… they did not provide me with original contract as I requested.”

“I did not receive any text or calls about this bill from a 3rd party… I would really appreciate this being taken off the credit report being that I had no contract with the collection agency.”

The investigation window

Once the dispute is filed with the credit reporting agency, the 30-day window for investigation will begin. During this time, the credit reporting agency will reach out to the furnisher of the information and request that it be verified. If the furnisher is unable to verify the information or fails to respond within the allotted timeframe, the information must be removed from the consumer’s credit report.

In Marcus’ situation, the investigation proved that the information Account Services was reporting was inaccurate. The medical provider had received payment from Marcus’ insurance provider for the procedure. Marcus had paid the remaining balance that he owed directly to the medical provider years earlier. Apparently, Account Services had somehow gotten an old bill from the provider that did not reflect the payments that had been made.

Because Account Services could not validate the debt, the credit reporting agencies were forced to remove it from Marcus’ credit report.

Understanding your rights against Account Services

FDCPA protections

The Fair Debt Collection Practices Act is a federal law that was created to protect consumers from abusive debt collection practices. There are several protections provided by the FDCPA that consumers should be aware of when dealing with a debt collection agency like Account Services.

You have the right to be free from harassment. Debt collectors are not allowed to harass or abuse consumers while attempting to collect a debt.

You have the right to be free from false or misleading representation. Debt collectors are not allowed to misrepresent the debt they are attempting to collect. They are not allowed to lie about their identity.

You have the right to dispute a debt. If you do not believe you owe a debt, you have the right to dispute it with the debt collector.

You have the right to request debt validation. If you dispute a debt, the debt collector has the right to request validation of the debt.

You have the right to request that a debt collector stop contacting you. If you do not want a debt collector to contact you, you have the right to request that they stop. Keep in mind that this will not eliminate the debt. The debt collector can still sue you to collect the debt.

Account Services has been accused of violating many of the protections provided by the FDCPA. Here are a few examples of complaints that have been filed against them:

“This should be paid entirely by my insurance I’ve spoke to several reps to try to resolve and they continue to ignore or use the incorrect insurance info.”

FCRA requirements

The Fair Credit Reporting Act is a federal law that regulates credit reporting agencies and the information they are allowed to report on a consumer’s credit report.

One of the protections of the FCRA is the right to dispute inaccurate or unverifiable information on your credit report. Information on your credit report must be accurate and verifiable. This means that if you dispute information on your credit report, the furnisher of that information must be able to prove that it is accurate. If they cannot, the credit reporting agency must remove it.

Here are some common reasons why information on your credit report may be removed: Incorrect balance, incorrect date of service or delinquency, someone else’s account, paid or settled accounts, accounts outside of the statute of limitations, unable to verify.

Account Services operates under several different names, which it admits can cause confusion for consumers. This can lead to errors on your credit report, which you can dispute to have removed.

Conclusion

What Marcus learned

Marcus learned a lot during his experience with Account Services. First, he learned that just because there is a collection on your credit report does not mean that you owe it. Second, he learned that paying a collection agency without disputing the debt first can leave the negative account on your credit report. Finally, he learned that working with a professional can make all the difference when dealing with a debt collector.

The $847 that Account Services was demanding was removed from Marcus’ credit report because the company could not prove that he owed it. He was able to apply for his mortgage without the collection dragging down his credit score.

Take action today

If Account Services is on your credit report, you don’t have to accept it. You don’t have to pay it. You have rights under federal law that you can use to your advantage when disputing the debt.

At FightCollections.com, we can help. We specialize in helping consumers deal with collection agencies like Account Services. We know their tactics. We know their weaknesses. We know the laws that they must follow.

We can help you determine if the collection on your credit report is legitimate. We can help you determine if it’s been properly validated. We can help you determine if it should be on your report at all.

Contact us today for a free consultation. Our experts can help you understand your rights and develop a strategy to use them to your advantage.