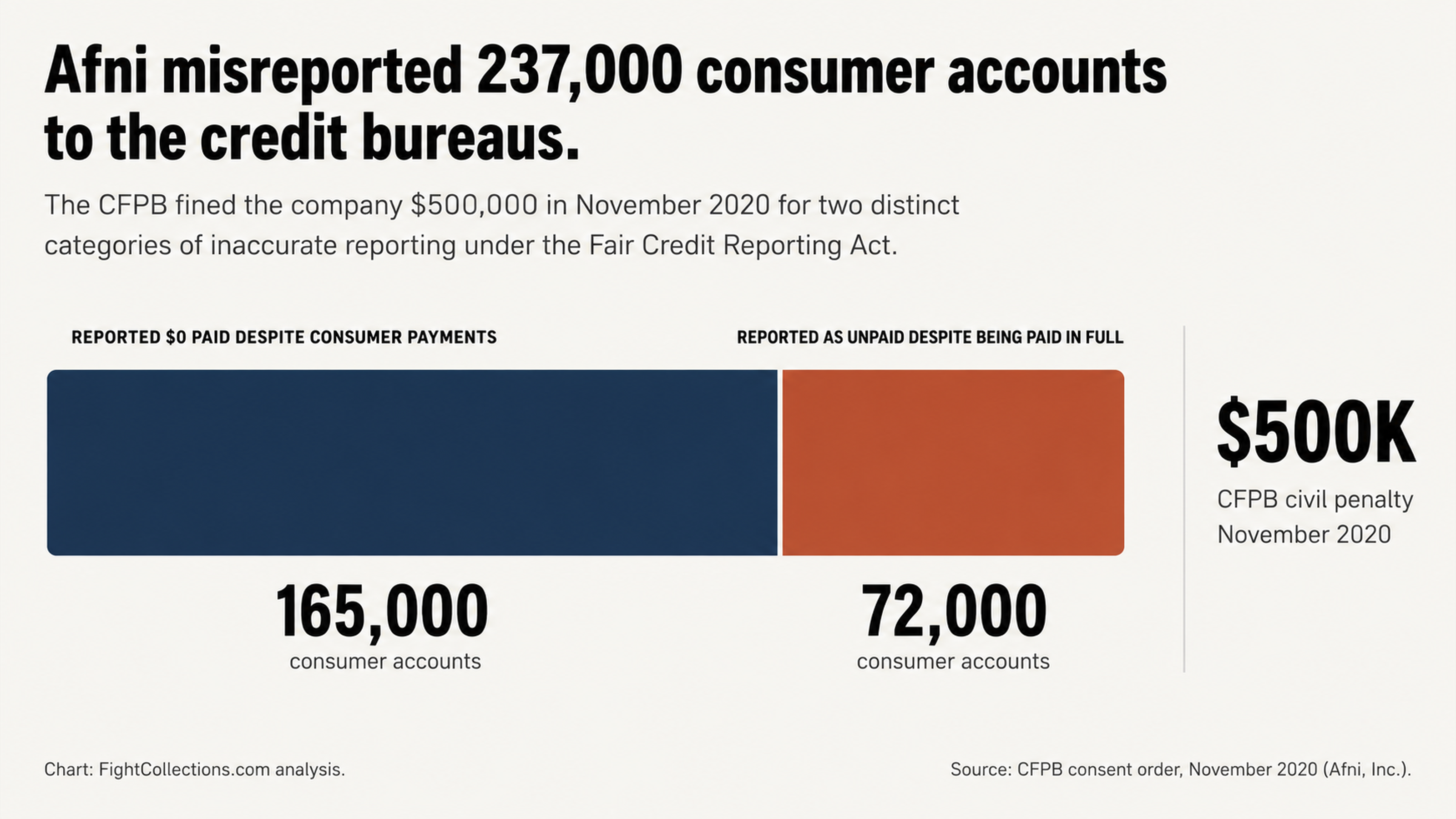

Afni Inc. is the debt collector whose name most frequently appears on consumer credit reports. This is not speculation — federal regulators have already caught this company misreporting over a quarter of a million consumer accounts to the credit reporting bureaus (CRB).

You can look up the details of the case. By reading the case history, you can gain an understanding of the company’s business practices, which may be useful to you in dealing with them. In this article, you’ll find an overview of Afni and some of the common issues consumers experience with them, based on data from the Consumer Financial Protection Bureau (CFPB) and the Better Business Bureau (BBB).

Afni, Inc. is a large debt collection agency founded in 1936 and employs approximately 10,000 people in the U.S. and offshore locations, including the Philippines and Mexico. They collect for a number of major corporations, including AT&T, Verizon, T-Mobile, Sprint, Comcast, DirecTV, and GEICO.

Federal Penalties Against Afni

In November of 2020, the Consumer Financial Protection Bureau (CFPB) ordered the company to pay a $500,000 penalty. The reason for the fine was that Afni had been reporting consumer accounts to the credit reporting agencies (CRA) with significantly incorrect information. In fact, the company reported that payments of $0.00 had been made on 165,000 accounts when, in fact, consumers had made payments.

In addition, they reported 72,000 accounts as still owing balances when those debts had already been paid in full. That’s a total of 237,000 accounts with materially incorrect information! The CFPB determined that the company had violated the Fair Credit Reporting Act (FCRA), Regulation V, and the Consumer Financial Protection Act (CFPA).

They weren’t through yet! In 2021, the company paid another penalty of $1.85 million to settle a class action lawsuit after the company’s data breach exposed Social Security numbers, driver’s license numbers, and financial information of over 261,000 people.

If the company can’t handle the information it has, and can’t furnish correct data to the CRAs, how do you know the information they are reporting about the debt they say you owe is any good?

Afni Collecting Debts From the Wrong People

If you look at the complaints filed against Afni with the BBB or the CFPB, you’ll see a number of people who say that Afni has attempted to collect a debt from them when they don’t owe it. Often, the consumers say they don’t even know the person the debt belongs to. Here’s one example, from a complaint filed in 2025:

“I was the witness to an auto accident. I have been extremely cooperative with the insurance company as well as the Police Dept. in their investigation. Now, they are attempting to claim I am responsible and owe them $2,895 for subrogation. They placed me into collections because I was a witness to an auto accident and had nothing to do with it.”

Here’s another one, filed in Sept. 2025:

“I received a letter from Afni, Inc. stating I owed them $10,030.16 because I was involved in an auto accident on a specific date in 2022. I was not involved in any type of auto accident on that date. I called Afni and asked for their information. They could not provide a driver license number, accident report, police report or any documentation that tied me to the auto accident claim. They stated they obtained my address from a people search.”

Why You Should Question Their Documentation

Here’s the important thing about these stories: If the company has a history of attempting to collect from people who don’t owe the debt, based on a people search match, how do you know they’ve correctly identified you as the debtor? And if they haven’t correctly identified you, how do you know they have any of the other correct documentation for the debt?

It’s worth noting that, according to a study done by U.S. Public Interest Research Groups, 79% of credit reports contain errors or serious errors. If the CRAs are already error-prone, and if Afni has a history of documentation problems, it’s certainly reasonable to challenge this debt and make them verify it before you pay.

Paying a Collection Doesn’t Remove It From Your Credit Report

Many people believe that, once they’ve paid a debt that has gone to collections, it will be removed from their credit report. Unfortunately, that’s just not true. When you pay a collection, the only thing that changes on your credit report is that the debt goes from being an “unpaid collection” to a “paid collection.” The debt remains on your report for the full 7 years from the original delinquency date.

So, what’s the big deal about that? The big deal is that the negative mark on your credit report can keep you from getting a loan or other credit. Or, you may pay a higher interest rate on a loan because of the derogatory mark. You may not get a job you want, or be able to rent the apartment you prefer. The negative mark can even cause you to pay more for insurance!

So, if paying a collection isn’t going to make it go away, what’s the point of paying it? And what if you settle the debt for less than the full balance? Sometimes it makes sense to negotiate a settlement with a collector, but be aware that it may not help your credit situation much. For one thing, if it’s reported as a settlement, it’s still a negative mark. For another thing, the way it affects your credit score depends on the individual facts of your credit report, so you can’t predict the outcome.

Broken Promises From Afni Representatives

Sometimes, consumers report that they are lied to by representatives of Afni. Here’s one story from a consumer complaint filed on the BBB website:

“We agreed to pay the $229 if AFNI would remove it from our credit. The representative agreed and said if it was paid in full they would remove it from credit reporting agencies. We paid the $229 and it wasn’t removed from the credit bureaus. We contacted AFNI and they said it would be removed in 7 years from when it was paid.”

Here’s the thing about this story: The consumer called Afni and agreed to pay based on a promise about what would happen to their credit report. But when they paid the debt, Afni did not follow through on their promise. The consumer is now out the $229 and still has the derogatory mark on their report. And, in experience, you can’t rely on verbal promises from debt collectors. Once you pay them, they have what they want and they don’t care what you want any more!

Information Is Power in Debt Collection

The debt collection business works because information is power. The debt collector has lots of information about your debt and about ways to collect it. You have very little information about how the system works or your rights within it. So, when you talk to a debt collector, they may be trying to get information from you that helps them pressure you into paying the debt.

The collector may ask if you can access funds today. If you say yes, they may demand that you pay immediately. If you say no, they may offer to accept a partial payment today and set up a plan for you to pay the rest later. In either case, you may not be doing what is best for your situation. But you are likely to be doing what the debt collector wants you to do.

Your Right to Demand Debt Verification

One thing you can count on when you are dealing with a debt collector is that they will try to get you to talk to them immediately. They will send you emails, letters, text messages and will call you. But you don’t have to talk to them today. You can put them off until you get your ducks in a row.

In fact, you can make them put their money where their mouth is. If they are telling you that you owe a debt, you can demand that they verify the debt and prove that you owe it. Under the Fair Debt Collection Practices Act (FDCPA), you have the right to challenge the debt collector to verify the debt. If they can’t do it, they have to cease collection activity and delete the account from your credit report.

Given the history Afni has of attempting to collect from the wrong people and mis-reporting debt information to the credit reporting agencies, the guess is they won’t be able to verify all the accounts they are collecting.

The Risks of Challenging Debt Collectors on Your Own

Many consumers attempt to challenge debt collectors on their own. Sometimes that works, but other times consumers end up in a worse place than when they started. For example, a consumer who is negotiating with a debt collector may inadvertently acknowledge that they owe a debt or restart a clock on the statute of limitations. They may agree to pay a debt without getting it in writing that the collector will delete the account from their credit report.

One BBB complaint against Afni demonstrates the procedural trap:

“I settled subrogation with Afni and paid settlement in full on January 17th, 2025. I was assured on my date of payment I would receive a letter of debt paid within the next 30 days. Fast forward from that date 55 days and I STILL have not received any letter. My license is suspended, I cannot drive, my debt is paid and I have no proof.”

If you hire a credit repair expert to help you deal with the debt collector, you can avoid pitfalls like these. Credit repair experts understand the rules governing debt collection practices. They know how to make the system work for consumers, not debt collectors.

How Credit Repair Experts Can Help

The goal of credit repair experts is to help consumers avoid the credit damage that results from collection accounts. They know how those accounts can affect consumers’ lives, from their ability to buy a home or finance a car to their ability to get a job or rent an apartment.

So, if you have a collection account on your credit report from Afni, Inc., don’t assume it’s valid just because they placed it there. Make them prove it! If you need help, contact us here at FightCollections.com. We will be happy to give you a free consultation about your situation.