Are you concerned about a collection on your report from Aldous and Associates? If so, you’re not alone.

Each month, thousands of people are contacted by debt collectors that they may or may not owe money to. So, what is Aldous and Associates and how did they end up on your report?

Here’s some basic information about this collection agency:

What Our Research Found on This Collection Agency

Aldous and Associates is a law firm and collection agency that was specifically created to collect debt from the fitness industry. Their largest clients include fitness centers such as Crunch Fitness, Gold’s Gym, Blink Fitness, and VASA Fitness, as well as property management and telecommunications companies.

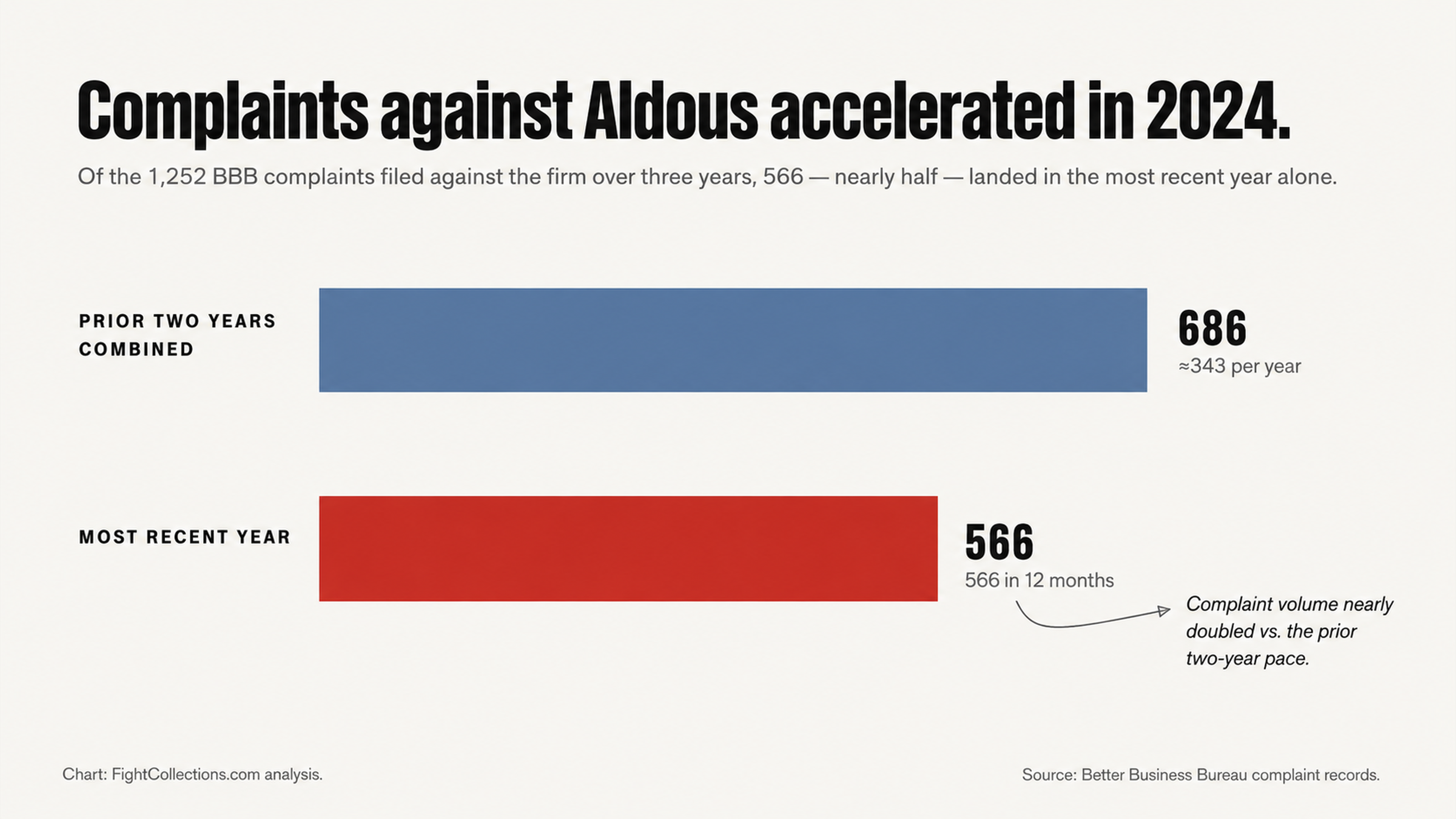

Aldous and Associates has racked up a surprising number of complaints. According to the Consumer Financial Protection Bureau, they’ve had over 1,700 complaints in the past year alone. They’ve also had 1,252 complaints in the last three years to the Better Business Bureau, with 566 of those complaints coming in the last year. Their BBB rating is a B, and they are not accredited.

Their ratings on consumer review websites are even more dismal. They have a 1.8 out of 5-star rating on WalletHub, with 76% of reviews being one star. This trend holds true across all the major review websites they appear on.

Why You Should Never Pay First

The #1 Trap Consumers Fall into When a Collection Notice Arrives

When you receive a collection notice or start getting calls from a debt collector, you may be tempted to pay whatever balance they say you owe and move on with your life. This is exactly what the collection agency wants you to do. What they aren’t telling you is that when you pay a collection agency, you’re simply changing the status of the account on your report from “unpaid collection” to “paid collection.” The account itself isn’t removed, and will stay on your report for up to seven years.

If a paid collection is still hurting your credit score, it’s likely because the original negative mark on your report has already affected your score. When you pay a collection account, it doesn’t remove the mark entirely. It will still say on your report that you had an account that was sent to collections, and that fact will still be considered when you apply for financing.

In fact, a study by the U.S. Public Interest Research Groups found that 79% of credit reports contain errors or other serious issues. If you pay a debt without verifying that it’s legitimate first, you may end up paying a debt that never should have been on your report in the first place.

What Can Happen if You Dispute the Debt Instead

Collection accounts can be removed from your credit report if the information is incorrect, if the account can’t be verified, if it’s fraudulent, or if the collector fails to respond to a dispute within a certain amount of time. When you dispute the debt, the burden of proof is on the collection agency, not on you.

Debt collection agencies often buy debts in batches and may not have much information on the individual accounts. When they’re challenged to verify the account details, they often can’t come up with the original contract, a complete payment history, or proof of ownership for the debt.

This isn’t a matter of trying to game the system. It’s a matter of exercising your legal right to a dispute under the Fair Debt Collection Practices Act (FDCPA) and the Fair Credit Reporting Act (FCRA). Both laws were enacted to protect consumers from incorrect reporting and unverifiable debts.

What We Found Out About This Debt Collector

Harassment and Excessive Contact

By far, the most common complaint about Aldous and Associates is their persistent phone contact. Many consumers have complained about being called every day, and even after requesting that the calls stop, the calls continued. Others reported that when they tried to talk to the representative, they hung up the phone.

Here’s what one consumer said about their experience with Aldous and Associates: “Harassing me constantly every day. Due to these people, I had to use an AI as a buffer but these people still try to talk or leave a message. These people are asking for money for a gym in my area who would not let me cancel my gym membership after several attempts.”

This is why it’s so important not to engage in verbal communication with a debt collector. Phone calls can’t be tracked for posterity, and they leave a lot of room for miscommunication. Plus, if you talk to a debt collector on the phone, it’s easy for them to use high-pressure sales tactics or trick you into saying something that can be used against you later.

Failure to Validate and Credit Damage

Many consumers have complained that Aldous and Associates failed to validate their debt, as is their legal obligation under the FDCPA. Some consumers didn’t even know they had a debt in collections until they saw it on their credit report.

Here’s what one consumer said about the experience: “A female representative from Aldous and Associates called and threatened to ruin my credit, then hung up. Then they reported to the credit reporting agencies and as a result of this single dispute, my credit score went from 783 to 580. Destroyed my credit because of this.”

If a debt collector can’t validate a debt, they aren’t legally allowed to collect it or report it to the credit reporting agencies. This could be a very good reason to dispute the debt and have it removed from your report.

Their Regulatory History

Consent Order in Connecticut

In May 2018, the Connecticut Department of Banking issued a consent order against Aldous and Associates. The department found that the company had acted as an unlicensed consumer collection agency in the state even though their license had expired.

On January 1, 2017, the company’s license to act as a consumer collection agency in Connecticut expired, but they continued to try to collect debts in the state even after it expired. At least two consumers complained about their practices during that time.

As a result, the company violated Section 36a-801(a) of the Connecticut General Statutes and was ordered to pay a $5,000 civil penalty. According to the consent order, penalties of up to $100,000 per violation could have been imposed.

This regulatory action against the company shows that they have a history of disregarding the law. When you’re disputing a debt, this can be an important factor to bring up.

Federal Litigation

The company has been the subject of several class action lawsuits alleging violations of the FDCPA. In one of those cases, called Powell v. Aldous and Associates, the consumer alleged that letters from the company implying they were attorneys constituted a threat.

According to court documents, “The Collection Letters fail to state that Aldous is a law firm, but instead, imply that an attorney has reviewed the consumer’s account and threaten to take legal action to collect the Debt. In fact, neither an attorney nor anyone else has reviewed Plaintiff’s account.”

Ultimately, the case was dismissed, but the allegations themselves are instructive. They suggest that the company may be engaging in practices that are at odds with the law.

In 2017, other FDCPA lawsuits were filed alleging that the company failed to include a disclosure of a consumer’s right to dispute a debt and failed to notify consumers of their rights. There are several law firms currently accepting FDCPA cases against this company.

How Collection Debt Actually Works

Debt is a Commodity, Not a Moral Obligation

There’s something that the debt collection industry doesn’t want you to know: once a debt has been sold to a collection agency, it stops being a moral obligation that you owe to another company and starts being a commodity that can be bought and sold like any other.

Aldous and Associates is a third-party debt collector that works on a contingency basis for its clients. That means they didn’t loan you any money, provide you with any services, or extend you any credit. Instead, they bought your debt from the original creditor, or they’re collecting on behalf of a creditor for a fee.

When you think of it this way, the dynamic changes entirely. Instead of being a matter of personal responsibility and obligation, it’s nothing more than a business transaction between two companies. And if you approach it as nothing more than a business transaction, you’ll be a lot better off.

The Asymmetry of Information

When the debt collector is calling you and sending you letters, they have a lot of information at their disposal. They have sophisticated computer systems, a team of attorneys, and representatives who are trained to get you to do what they want.

But you, on the other hand, are likely to be getting a call or letter from a debt collector for the first time. You don’t know your rights, you don’t know the law, and you don’t know how to make the collector stop contacting you.

This information asymmetry is no accident. Collectors rely on it to make money. They know that if they can get you to act out of urgency or fear, you’re more likely to pay them money that you may or may not owe.

But if you know your rights and understand how the system works, the playing field is leveled. So, what can you do to protect yourself?

The Importance of Not Talking

When you talk to a debt collector on the phone, you’re playing the game on their turf. They know how to use psychology to get you to do what they want. They know which buttons to push to make you feel guilty or scared.

And once you say something to them, they can use it against you. They may try to tell you that you’ve acknowledged the debt, or that you’ve agreed to pay it. But if you don’t give them the opportunity to talk to you, they can’t take advantage of you that way.

In fact, you don’t have to respond to them at all. You don’t have to call them back or write them a letter. Most of the time, they’re simply trying to get you to respond so that they can establish that you’ve received their letters or phone calls.

The Case for Getting Help

Why You Should Hire a Credit Repair Professional

Debt collection calls are designed to get a rise out of you. They want to make you feel guilty or scared so that you’ll pay them money as soon as possible. When you handle a debt collection on your own, you’re engaging with them on their level. And that means you’re fighting a battle you can’t win.

When you work with a credit repair professional, you’re not just getting help from someone with a lot of expertise. You’re also creating distance between yourself and the situation so that you don’t get caught up in the emotional manipulation that debt collectors use.

Your very first move when you get a collection notice should always be to call a credit repair expert, never the debt collector. Before you have any contact with them at all, you should understand what’s going on, what your options are, and how to proceed.

Why You Need to Understand the Technical Details

Disputing a collection requires you to understand some technical details about how the process works. You have to know what timelines apply, what your options are, and how to document everything. If you don’t understand the process correctly, you could end up filing a dispute incorrectly, which means you’ll just end up wasting time and potentially causing more damage to your credit.

Do you know which credit reporting bureau to contact? Do you know what language you should use when you dispute the debt? Do you know what to do if they verify the debt anyway?

A credit repair professional understands how to identify errors in reporting, documentation issues, and procedural problems that can help you get the collection removed from your credit report. And they know how to succeed where others fail.

Plus, when you’re dealing with a collector like Aldous and Associates that has over 1,700 complaints with the Consumer Financial Protection Bureau in a single year and a history of failing to validate debts, it’s especially important to get some help.

What to Do Next

Now you know what to expect if you’re dealing with Aldous and Associates. But what does it all mean for your credit report?

If you see a collection account from this agency on your report, it doesn’t have to be the end of the world. In fact, it could be the beginning of the process to remove it entirely.

So, what should you do? Here are a few “don’ts” to keep in mind:

- Don’t call the agency directly

- Don’t try to negotiate with them or explain yourself

- Don’t pay them money unless you’re sure that the debt is legitimate and you owe it

Instead, call us. Here at FightCollections.com, we specialize in helping consumers deal with debt collectors and remove questionable collection accounts from their credit reports. We understand their tactics and we know how to fight them.

So why not get in touch with us today? We’ll do a free consultation to talk about your case and your options. And then we’ll help you develop a strategy that’s tailored to your needs.

The debt collection industry relies on consumers not understanding their rights. We’re here to change that. So contact us today and let’s get started.