A credit report blemished by an AllianceOne collection is a difficult surprise to accept. Most consumers are quick to call and try to make it all better as quickly as possible.

Not only does the hurried approach usually result in the situation worsening rather than improving, but it also plays into the collection industry’s best tool for revenue generation — misconceptions.

Understanding how to handle an AllianceOne collection starts with debunking the myths that you are about to read. If there is one thing that the collection industry counts on, it is the consumer’s lack of understanding about credit reporting, consumer rights, and the fact that the power is in the consumer’s hands. Here is the truth about AllianceOne collection accounts that will help you get the resolution that you want.

Who is AllianceOne?

AllianceOne Receivables Management, Inc. is a third-party debt collection agency based in Pennsylvania. Here is the pertinent information that you should know about AllianceOne:

AllianceOne operates as a subsidiary of Teleperformance SE, a French multinational company that acquired AllianceOne in 2007. At the time of the acquisition, AllianceOne reported an annual revenue of $115 million and employed 2,000 people across multiple sites.

AllianceOne collects medical bills, credit card debt, parking tickets, toll fines, and government-owed debts for clients including the City of Los Angeles and health systems. AllianceOne has more than 4,350 hospital clients through its partnership with Premier Inc.

AllianceOne Consumer Concerns

Despite the size of the company and the significant number of clients and collections, AllianceOne has faced a few concerning issues over the years. Here are some of the consumer protection issues that have raised red flags:

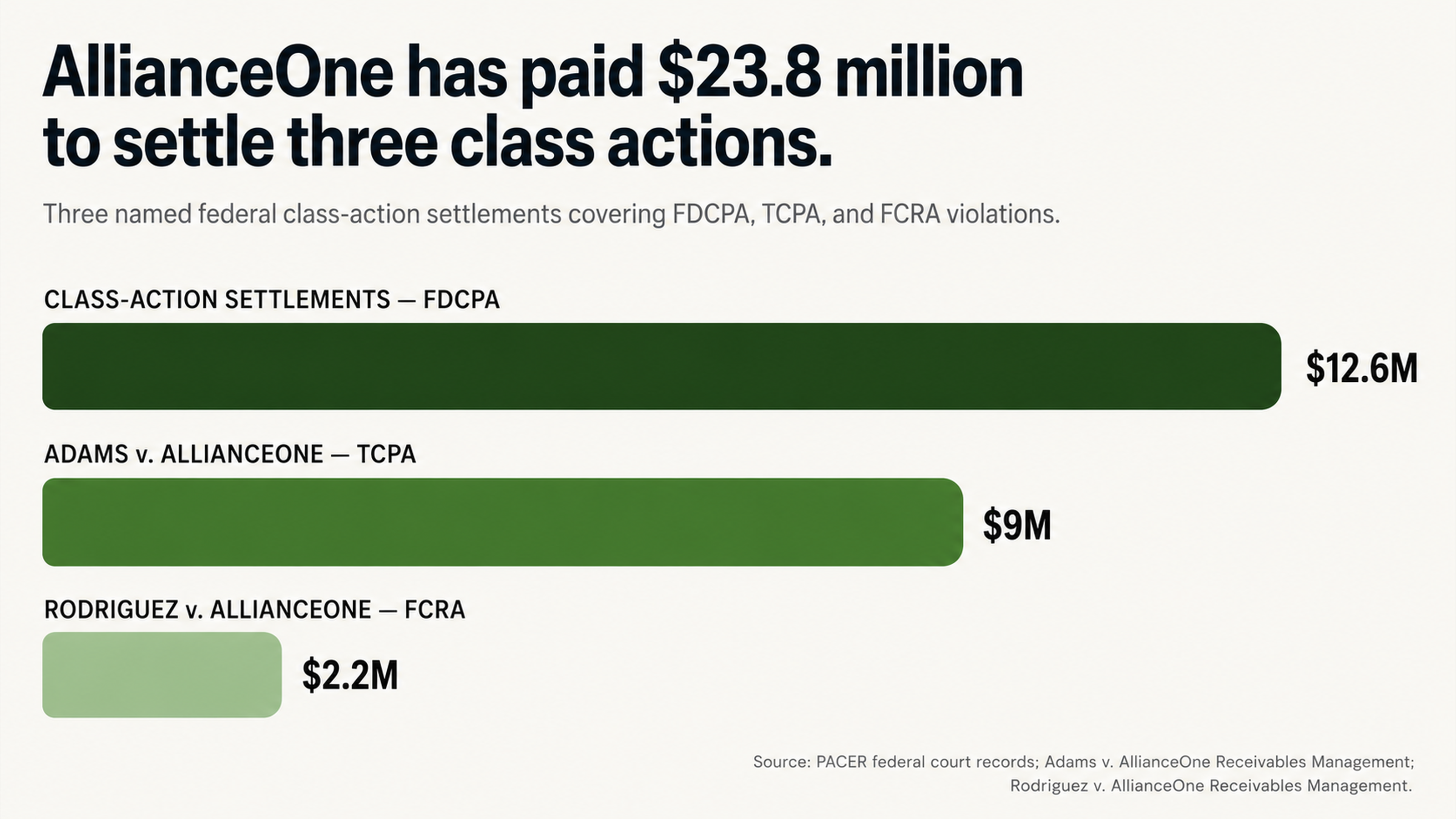

AllianceOne paid $12.6 million to settle class-action lawsuits for violating federal consumer protection laws.

AllianceOne paid $9 million to settle the Adams v. AllianceOne class-action case for violating the Telephone Consumer Protection Act.

AllianceOne paid $2.2 million to settle the Rodriguez v. AllianceOne class-action case for pulling credit reports on nearly 15,000 consumers without a permissible purpose.

The Consumer Financial Protection Bureau (CFPB) received 654 complaints about AllianceOne, making AllianceOne 39th out of 2,458 debt collection companies.

The CFPB complaint database reports more than 400 federal lawsuits filed against AllianceOne.

These statistics represent consumers who felt as though the company violated their rights.

Myth 1: You Have to Pay Collections Right Away to Fix Your Credit

Why Paying a Collection Will Not Help Your Credit Score

One of the biggest misconceptions about paying off collections is that doing so will help your credit score. Unfortunately, this is just not true. When you pay a collection, the status of the account is updated to reflect that it is now paid. However, the fact that you had a collection on your credit report in the first place still exists, and the paid collection will remain on your credit report for seven years from the original delinquency date.

Furthermore, some lenders may view a paid collection as a negative mark on your credit report. For these lenders, the fact that you had to have a third-party debt collector to get you to pay the debt in the first place says a lot about your creditworthiness, regardless of whether the account is paid or unpaid.

How a Collection Impacts Your Credit Report

Having a collection on your credit report can greatly impact your ability to get a loan for a house or a car or to qualify for a credit card. Additionally, many employers and landlords will not hire you or rent to you if you have negative marks on your credit report. This is why it is so important not to rush into paying off a debt without first having a plan.

Charge-Off: What it Means and Why it Matters

If AllianceOne is collecting a debt from you, it is likely because the original creditor charged off the debt. What is a charge-off? A charge-off is when a lender writes off a debt because it is very unlikely that it will be collected. When a debt is charged off, the lender is required to report the loss on its tax return, which means that the lender is ultimately footing the bill for the debt. A charge-off will remain on the borrower’s credit report for seven years from the original delinquency date of the debt. Typically, a charge-off occurs 180 days after the borrower has missed a payment.

Once a debt is charged off, the original lender may attempt to collect it or may hire (or sell the debt to) a third-party debt collection agency to collect the debt.

Why the Charge-Off Matters

So, why does a charge-off matter? Well, for starters, it is important to understand that, once a debt is charged off, the original lender is not likely to care whether the debt is collected or not because the debt has already been written off and a tax deduction has been claimed. Therefore, if a debt collection agency, like AllianceOne, is attempting to collect a charged-off debt, the debt collection agency does not have nearly as much leverage as you might think. In fact, the debt collection agency may have purchased your debt from the original lender for pennies on the dollar.

Additionally, the debt collection agency did not lend you any money, nor did it provide you with any goods or services. Instead, the debt collection agency simply purchased the right to attempt to collect the charged-off debt from you.

Myth 2: AllianceOne Already has the Documents They Need

Why AllianceOne Struggles with Documenting Debts

If you are dealing with a debt collector like AllianceOne, it is likely because the debt collection agency is collecting debts that are owed to someone else. Because debt collection agencies like AllianceOne collect so many debts, it is not always easy to keep track of the necessary documentation for each debt. In fact, AllianceOne has been found liable in court for failing to properly document debts.

For example, in the case of Rodriguez v. AllianceOne, AllianceOne was sued in federal court for pulling credit reports on nearly 15,000 consumers who owed money for parking tickets. The court ultimately found AllianceOne liable because parking tickets are not consumer-initiated credit transactions and therefore do not meet a permissible purpose for pulling someone’s credit report.

Consumer reviews of AllianceOne on the CFPB website also document the company’s failure to verify and validate debts. One reviewer claimed that AllianceOne attempted to collect two citations from 1995 that were already paid. Despite the fact that the debts were nearly 15 years old and paid in full, AllianceOne continued to attempt to collect the debts.

What’s more, data from credit reports shows that as many as 79% of credit reports contain some type of mistake or error. When you combine this with the documentation issues that debt collection agencies already face, the margin for error becomes enormous. For example, one consumer reported that AllianceOne attempted to collect the same debt eight to nine times across all three credit bureaus (Equifax, Experian, and TransUnion). Every time the consumer had a credit reporting agency remove the debt from his report, AllianceOne would report the debt again using a different account number.

If AllianceOne is attempting to collect a debt from you and cannot verify the debt, you may have grounds for disputing the debt and requesting its removal from your credit report. Debts can be disputed and removed if they are inaccurate, if they contain errors, if they are fraudulent, or if they cannot be verified within a reasonable amount of time. The burden of proof is on the collection agency to show that the debt is valid and that it belongs to you.

Myth 3: You Should Talk to the Debt Collector and Try to Work Things Out

Why You Should Not Talk to a Debt Collector Without a Plan

Debt collectors are professionals who are trained to get you to pay debts as quickly as possible. Most consumers, on the other hand, are not professional debt negotiators and are not experienced in dealing with debt collectors. Debt collectors know what to say to make you feel like you have to pay a debt right away. They may also use high-pressure sales tactics or attempt to intimidate or harass you into paying debts.

If you talk to a debt collector without a plan, you may end up accidentally saying something that will hurt your case and ultimately cause you to pay debts that you do not owe. Additionally, anything you say to a debt collector can and will be used against you. Confirming your identity, admitting that you owe the debt, discussing payment amounts, or revealing financial information can all weaken your case against the debt collector.

Furthermore, debt collectors may attempt to overshadow the required 30-day dispute period by making demands for immediate action. For example, in the case of Yunker v. AllianceOne, AllianceOne attempted to collect debts in a way that overshadowed the required 30-day dispute period.

Instead of making a plan and trying to negotiate a settlement or figure out whether the debt is valid, many consumers will talk to a debt collector without doing their research ahead of time. Before you have any communication with a debt collector, it is important to talk to a credit repair professional who can help you understand your rights and come up with a strategy for how to proceed.

The Silence is Golden Approach

There is no law that requires you to talk to a debt collector on the phone or communicate with a debt collector in any way. In fact, you have the right to remain silent and to ask that the debt collector not contact you again until it has verified the debt. If a debt collector is attempting to collect a debt from you, you can request that it stop contacting you and send you written verification of the debt instead.

You can also request that the debt collector validate the debt, which means that it must provide you with proof that the debt is valid and that you owe it.

Debt collectors will not continue to attempt to collect a debt if it is going to cost them more money than the debt is worth. Disputing debts, requesting validation, and filing complaints through agencies like the CFPB all cost money. If you understand your rights and are willing to advocate for yourself, there is a good chance that a debt collector will decide that your debt is not worth pursuing.

One reviewer of AllianceOne reported that a representative from the company called her every day, seven days a week, between 8:15 am and 9:00 pm every 20 minutes. This type of excessive contact may be a sign that the debt collector does not have a strong case against you.

Myth 4: You Can Handle a Debt Collector on Your Own

Why You Should Not Handle a Debt Collector on Your Own

Federal and state laws are in place to protect consumers from debt collectors who attempt to harass, intimidate, or mislead them into paying debts. Some of the main laws that protect consumers from debt collectors include:

The Fair Debt Collection Practices Act (FDCPA): This law prohibits debt collectors from engaging in unfair, deceptive, and harassing behavior.

The Fair Credit Reporting Act (FCRA): This law protects consumers’ rights to privacy and accuracy when it comes to their credit reports.

The Telephone Consumer Protection Act (TCPA): This law limits the ways in which debt collectors can contact consumers over the phone.

If you are dealing with a debt collector, it is likely because you owe debts to the debt collector’s client. Understanding your rights under these laws can help you determine whether the debt collector is violating federal law and whether you have grounds for a lawsuit. However, reading and understanding federal laws and determining how to proceed can be difficult and time-consuming.

Most consumers do not have the time or the expertise to understand federal laws and to advocate for their rights in the same way that a credit repair professional can. For example, AllianceOne was found liable in federal court for violating the FDCPA. In the case of Foster v. AllianceOne, AllianceOne was sued for using misleading language in collection letters regarding IRS reporting. Unless you have experience reading and understanding collection letters, you may not recognize when a debt collector is violating federal law.

In fact, AllianceOne has paid $12.6 million in settlements for violating federal consumer protection laws, including violations of the FDCPA. These settlements were the result of class-action lawsuits against AllianceOne brought by attorneys who understood federal law and recognized that it was being violated. Most consumers do not have the resources or the expertise to bring a class-action lawsuit against a debt collector for violating federal law.

How a Collection Affects Your Credit Score

If you have debts in collections, it is likely affecting your credit score. In fact, collections can greatly impact your ability to get a mortgage, a car loan, or a credit card because lenders view consumers with collections as riskier than consumers without collections.

Some employers and landlords also perform credit checks on potential employees or tenants. Having a collection on your credit report may prevent you from getting the job you want or the house you want to rent.

Because the stakes are so high, attempting to handle a debt collector on your own can be risky. In fact, it may end up costing you money and weakening your case against the debt collector. Credit repair professionals understand federal law and your rights under the law. They can help you come up with a strategy for how to proceed and can communicate with the debt collector on your behalf to negotiate a settlement or help you determine whether the debt is valid.

Conclusion

AllianceOne Receivables Management is a legitimate debt collection agency with a long history of collecting debts for its clients. However, the company has also been the subject of several recent class-action lawsuits for violating federal consumer protection laws. In fact, AllianceOne has paid more than $12.6 million in settlements, including a $9 million settlement for violating the Telephone Consumer Protection Act and a $2.2 million settlement for pulling credit reports without a permissible purpose. The company has also had more than 654 complaints filed with the CFPB and more than 400 federal lawsuits.

The truth is that many consumers do have the power to dispute inaccurate debts and have them removed from their credit reports. In fact, simply disputing the accuracy of the debt is a great first step for consumers who want to take control of their credit reports and ensure the information is accurate. However, paying a debt without first verifying that it is valid is not likely to help your credit report.

Before you pay a collection, it is important to make sure that it is valid and that paying it will actually help your credit score. You should also be aware of your rights when it comes to dealing with debt collectors and make a plan before talking to a debt collector or responding to collection letters.

Are you ready to take the first step in reclaiming your good credit? Contact our office today to arrange a free consultation with a knowledgeable and experienced credit expert who can help you understand your rights and make a plan for how to proceed.