Americollect on your credit report? First, don't panic. Then, don't pay.

A collection account from Americollect is a red flag that warrants some serious investigation before you do anything else, including paying it.

In fact, before you do anything else, you should scrutinize that credit report entry very closely. There may be a red flag there already, signaling that there's a problem with the account. And if you catch it early, you can save yourself a whole lot of grief.

When you realize that 79% of credit reports contain an error or serious error, according to studies by U.S. PIRGs, you'll want to question everything about that collection account. Americollect has tried to position itself as a "ridiculously nice" collector, but thousands of consumers have filed complaints after finding errors, disputing debts, and even finding accounts on their credit report that shouldn't be there at all.

Your very first reaction might be to pay it and get it over with. Don't do that, either. When you pay a collection account, it changes from an unpaid collection to a paid collection. But that paid collection is still going to be there for seven years, dragging down your credit score.

What might seem like an easy way out now could end up being a permanent blot on your credit report. So who is Americollect, and why should you be wary of a collection account from this agency?

Who is Americollect?

Americollect is a medical debt collection agency based in Wisconsin that was founded in 1964. The company specializes in debt collection for hospitals and physicians and works with about 120 hospitals and 7,000 physicians across the country. Here is some basic information about Americollect:

What the Complaint Record Shows

Even though Americollect bills itself as "ridiculously nice collections," the Consumer Financial Protection Bureau database suggests otherwise. The company has between 1,800 and 2,000 complaints registered there, and between 2020 and 2024 the number of complaints grew by 233%.

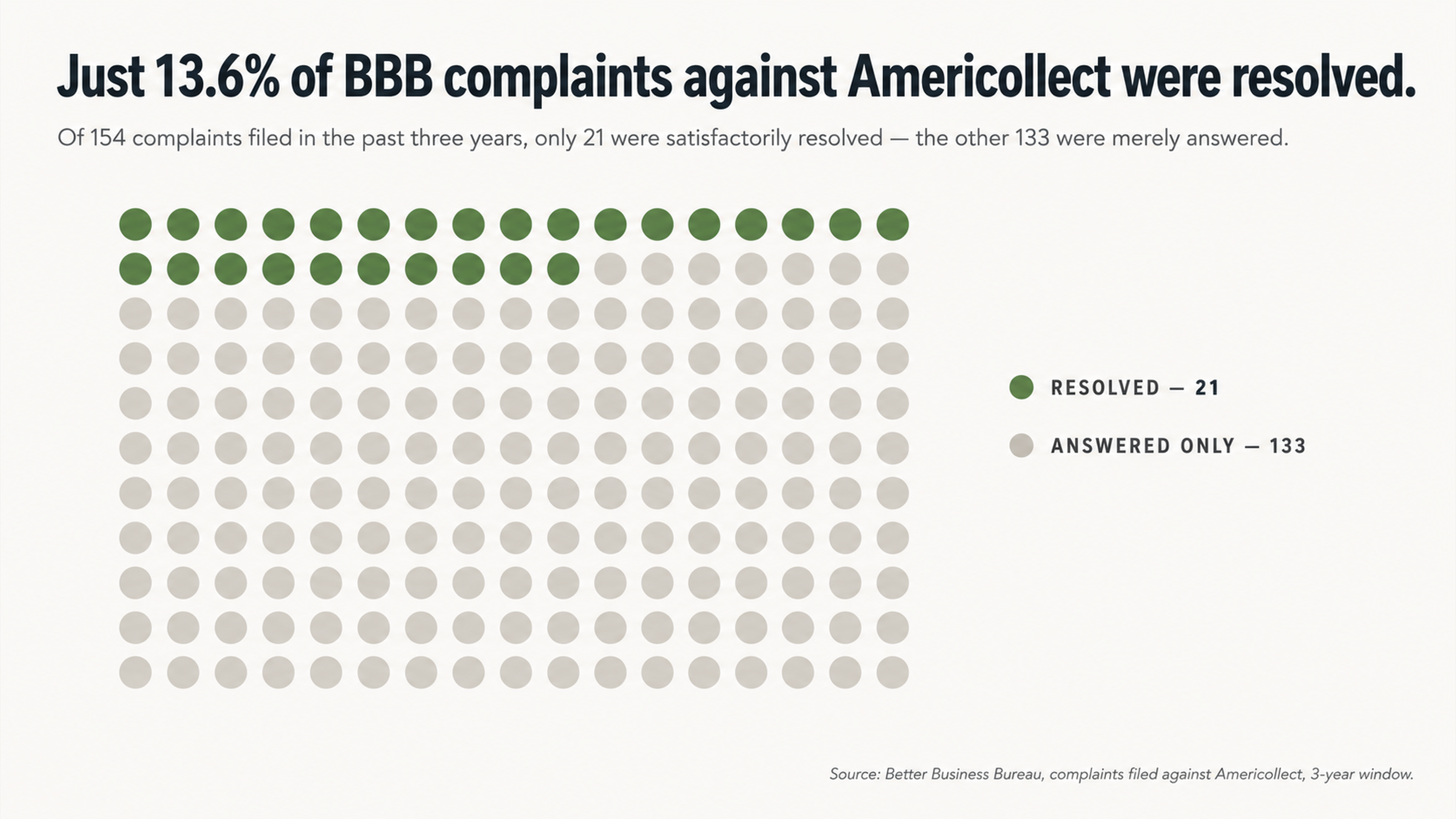

In 2016, Americollect was the most complained-about debt collection company in the entire state of Wisconsin. The Better Business Bureau (BBB) paints a similar picture. Though Americollect is accredited through the BBB, the company has an average customer review rating of just 1/5 stars.

Of 154 complaints filed within the past three years, only 21 (13.6%) were considered satisfactorily resolved; the other 86.4% were merely answered. There have been multiple federal class action lawsuits filed against the company alleging violations of the Fair Debt Collection Practices Act.

For example:

Martin v. Americollect, 2024

Kijek v. Americollect, 2018

These cases allege violations like the use of confusing collection letters, failure to properly disclose the balance due, and a general failure to validate debts. This is important, because it suggests that Americollect may have a tendency to act in ways that might impact your account as well.

Red Flags to Look for With Your Americollect Account

When you pull your credit report and see the Americollect entry, look carefully at the dates and details provided. In some cases, you may find that there are red flags built right into the entry.

Suspicious Dates and Timeline Inconsistencies

Look at the dates on your credit report. When did you supposedly open the account? When was the first reported delinquency? And when did Americollect start reporting the account? All of those dates should make sense in relation to any medical care you received.

One very common red flag to watch out for here is a manipulation of dates to make an old debt appear newer than it actually is. Under federal law, there's a limit to how long negative information can stay on your credit report. Some collection agencies will try to get around that by "re-aging" the debt. If the dates seem fishy to you, then that's a good starting point for a dispute.

Consumer complaints against Americollect often mention debts that "just showed up" without any prior contact. As one consumer explained in a BBB review: "They call me almost daily, between 6am and 10pm. I have repeatedly asked for proof, because the bill they are claiming I owe I never received."

Reporting a debt without proper notification is a violation of federal validation rules.

Missing or Incomplete Account Details

Look closely at what information is included on your credit report entry about this debt. A typical collection account should include some very specific details, such as the name of the original creditor, the amount you owe, and an account number. If any of that information is missing or vague, that's a red flag right there.

When you're dealing with a medical debt, information has to be transferred from the healthcare provider to the billing company to the collection agency. At any point in that chain, information could become corrupted, misattributed, or simply lost.

Given that 89.9% of the CFPB complaints about Americollect relate to debt collection issues, it seems safe to say that these documentation gaps are a real problem and not just an isolated incident. You have a right to demand documentation of your debt. This should include:

The name of the original creditor

The exact amount that you owe

The date of service

Proof that you owe the debt

You also have a right to require the collector to prove that information. If they can't do it, then it's going to be very difficult for them to continue reporting the information.

Why You Shouldn't Rush to Pay

When a debt collector is calling you every day, it can be tempting to just pay the debt and make it all go away. But that's exactly what the collector is hoping for. And once you've made a payment, you've just acknowledged the debt and made it much harder to get help if you need it.

The Psychology of Collection Pressure

Debt collection agencies make money when consumers pay up quickly. There's not a lot of profit in a long, drawn-out battle, so collectors are incentivized to get consumers to pay as fast as possible. In fact, every single day you spend deciding what to do rather than paying them costs the collection agency money.

So there's a reason all those phone calls can be so scary and urgent. As one Americollect consumer described it: The harassment from this company is unreal. They call me daily before and after business hours. I have asked to be taken off the call list, but it never happened. I have blocked about 100 phone numbers and they still manage to call me from a new number daily.

The reason for all that pressure is simple: Your silence is a powerful weapon. When you refuse to engage with the collector directly and instead force them to communicate through proper channels, you're taking away a lot of the leverage they have. And information is power, so when the situation starts to shift a little more in your favor, you're much better off.

The Payment Trap

When you make a payment on a collection account, you could be making a big mistake. Not only could you be acknowledging a debt you don't owe, but you could also be restarting a clock in the statute of limitations for an old debt.

Here's how one consumer put it in a review: "They refused to provide documentation of the payment plan unless I make a payment first. They know once you make a payment you cannot dispute the debt."

Understanding the economics of your debt can help you understand why making a payment isn't the moral obligation you think it is. When your healthcare provider sells a debt to a collection agency, the provider has already written that debt off. They've already gotten the tax benefit of the loss and closed the account. The company calling you now bought your debt for pennies on the dollar and has no connection whatsoever to the care you received.

So now the situation looks a little different, doesn't it? You aren't refusing to pay a debt you owe your doctor or hospital. Instead, you're refusing to pay a debt that a completely different company is trying to collect from you. And they bought your debt for pennies on the dollar and are now trying to make a profit on it.

The Dispute-First Approach

Your Right to Verification

Under federal law, you have the right to require proof of a debt before you pay it. The Fair Debt Collection Practices Act says you can request verification of the debt, which should include:

The amount of the debt

The original creditor's name

Documentation of the chain of ownership for the debt

Proof that you're actually responsible for the debt

This isn't a loophole or a technicality. This is a law that's on the books because debt collection is a shady business that's full of errors, misattributions, and outright fraud. Given that 9.2% of the complaints the CFPB has logged about Americollect relate to credit reporting issues (separate from debt collection practices), it seems safe to say that reporting errors are a real issue here, too.

And when a collector can't verify the information it's reporting, the credit bureau has to remove the entry. Collection accounts rise and fall on their documentation, and in many cases the collector won't have the documentation to back up its claims if you push it to verify.

Documentation Failures as Dispute Leverage

Every single documentation failure is a point of leverage for your dispute. Medical debts get passed through so many different hands before they land at a collection agency that it's easy for errors to creep in at any point along the way. Patient misidentification, balance errors, insurance payment misapplications... all of those things can render a collection account inaccurate and unverifiable.

Pointing to procedural failures and documentation shortcomings in order to dispute a collection account isn't somehow cheating or gaming the system. These are protections that are built into the system to help consumers cope with a debt collection industry that's rife with errors and abuse.

The Fair Credit Reporting Act requires that any information in your credit report be both accurate and verifiable. And if it's not, the prescription is simple: The credit bureau has to remove the information.

The class action cases filed against Americollect outline specific documentation problems that are affecting large numbers of consumers. Cases alleging everything from misleading letters with confusing balance information to failure to properly validate debts suggest systemic problems that probably affect a lot more people than just the ones named in the complaint.

Why Professional Help Matters

Removing Emotional Manipulation From the Equation

Working with a credit repair professional to dispute a collection account isn't just about bringing in some expert-level help. It's also about inserting a layer of insulation between you and the emotional manipulation that debt collection agencies specialize in. When a pro is handling your disputes, those phone calls and letters suddenly don't pack the same punch.

Consumers have filed a lot of complaints against Americollect describing practices that are clearly designed to distress people.

Here's one example: "They called my house 11 days before my brother passed away. Then, they proceeded to call me about my deceased brother's debt for a year after his passing." Those kinds of pressure tactics lose all their potency when consumers are working with a pro.

In addition, there's a huge information imbalance when you're dealing with a debt collection agency directly. They have millions of accounts and know every trick in the book for getting consumers to pay up. You don't. But a credit repair pro does.

Systematic Dispute Strategies

Professional credit repair firms have systematic strategies for identifying and challenging information that's inaccurate or can't be verified. That means going through your credit report with a fine-tooth comb and looking for any discrepancies or potential problems. It also means knowing how to craft a good dispute letter, what documentation to request, and when to escalate your dispute. In a lot of cases, consumers who are working with a pro can get a lot better results than they could on their own.

Credit reporting law is complex and the system contains millions of errors. So it's no surprise that professional help can often root out problems that consumers might miss on their own. And when Americollect only manages a 13.6% complaint resolution rate through the BBB, it's clear that consumers benefit from having a professional advocate in their corner.

Conclusion

If you see an Americollect collection account on your credit report, don't panic and don't pay. Instead, take a closer look at the entry to see if there are any built-in red flags you should know about. Look for suspicious dates and timeline inconsistencies, and watch for missing or incomplete account details. And don't rush to pay the debt just because a collector is breathing down your neck.

You have a right to dispute information that's not accurate or can't be verified, so don't be afraid to use it. The original creditor has already written your account off and moved on. The company that's reporting you now bought your debt for pennies on the dollar and has no connection to you whatsoever. Your credit report will affect your ability to find housing, get a job, and qualify for credit and loans for the next several years. Make sure you're protecting it from information that isn't accurate.

So don't let an Americollect collection account drag you down without a fight. For a free consultation on your credit report, contact the pros at FightCollections.com today. We'll help you identify potential problems, craft an effective dispute, and push back against collection agencies that are refusing to follow the law. You don't have to go up against those aggressive collectors by yourself. And you shouldn't be making any decisions about how to proceed without getting a clear picture of your options, either.

Your credit report is one of the most important reflections of your financial history and health. You owe it to yourself to protect it from inaccurate information. So why wait any longer? Get the professional help you need to push back against abusive collection practices and reclaim your good credit today.