AmSher Collection Services is a collection agency in Alabama that’s been in the debt collection business since 1986.

They collect mostly telecommunications debt (including T-Mobile debts) as well as medical, utility, and property management debts. They were acquired by InDebted, an Australian fintech company, in July 2025.

What we know about AmSher Collection Services

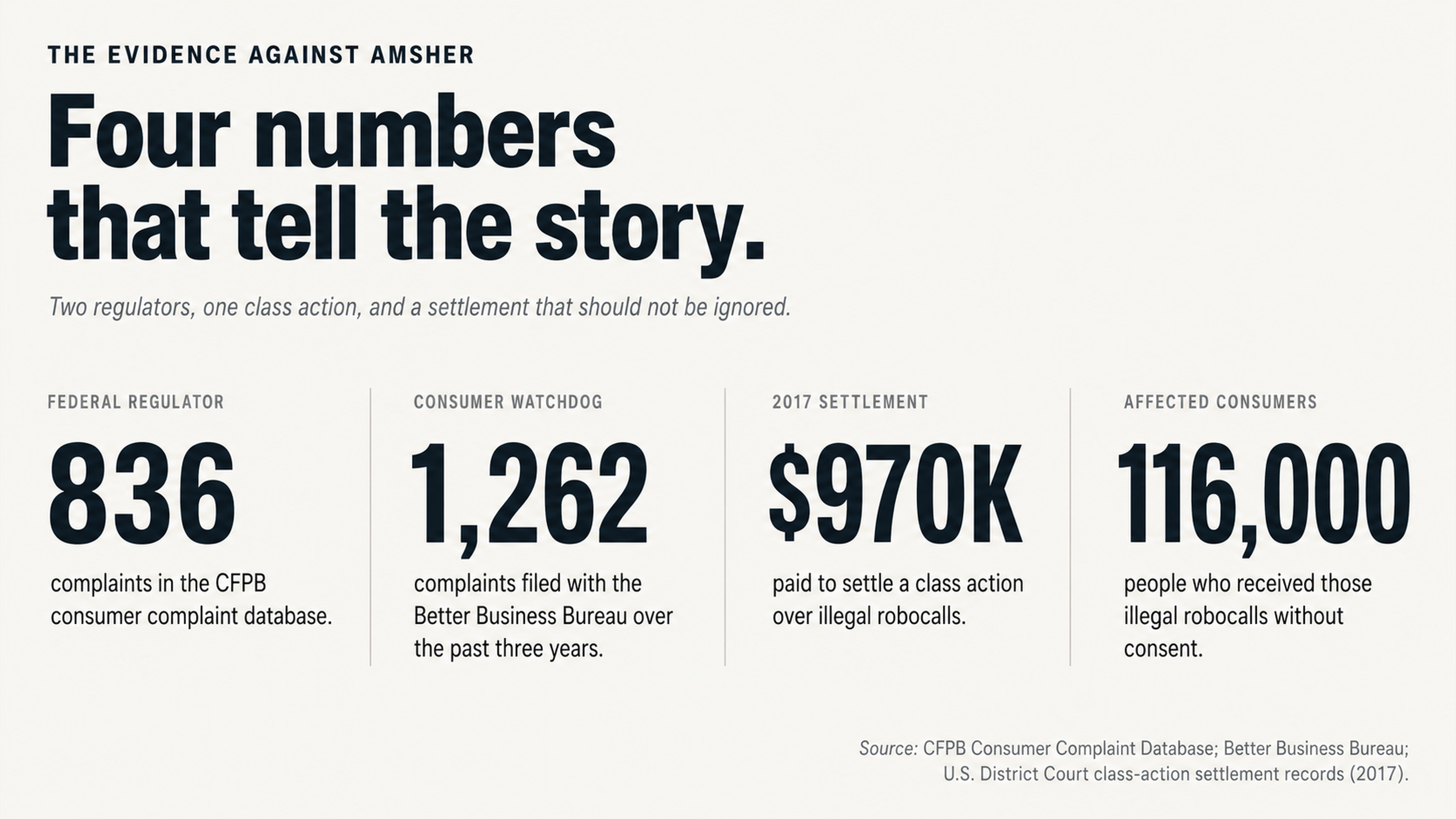

AmSher advertises itself as “Compassionate Collections,” but they’ve got a lot of skeletons in their closet. In 2017, they agreed to pay $970,000 to settle a class action alleging that they made illegal robocalls to 116,000 consumers without their consent. This forced them to revamp their calling policies.

But there are a lot of complaints about AmSher. We found 836 complaints in the CFPB’s consumer complaint database, 1,262 complaints in the past three years on the Better Business Bureau website (and 253 complaints in the past year), and 68 percent of people who reviewed AmSher on WalletHub gave the company a one-star rating.

In April 2025, the California Department of Financial Protection and Innovation issued a Desist and Refrain Order against AmSher, fining them $3,500. And in 2024 and 2025, new FDCPA lawsuits were filed against them in federal court.

What AmSher Collection Services hopes you don’t realize

They hope you’ll panic

Collection agencies count on fear to get what they want. The moment you see an unfamiliar collection account on your credit report, your heart sinks. You feel pressure to respond right away, without investigating whether or not you actually owe the debt. But this is exactly what you shouldn’t do.

When you see a negative account on your credit report, you’re likely to worry that it will hurt your chances of getting approved for a mortgage, car loan, apartment, or maybe even a job. This fear is intentional. It’s designed to make you pay the debt without verifying whether or not you owe it.

But the truth is that there are federal laws that protect you from collectors who try to coerce you into paying debts you don’t owe. When a collector contacts you, you have the right to request verification of the debt, which means they have to prove that you owe it and that they have the right to collect it.

They assume you’ll pay without requesting verification

Most collection agencies collect debts that were originally owed to someone else. They buy or are assigned debts, and often don’t receive much documentation on these debts. That’s okay, because they assume you’ll pay the debt without asking for proof that it’s yours.

But the truth is, most credit reports are full of errors. A study by U.S. PIRG found that 79 percent of credit reports contain errors or confirmed inaccuracies. If you have an account on your credit report from AmSher, it could easily be one of them.

Consider what happened to this reviewer on the Better Business Bureau website, who claimed that AmSher reported a T-Mobile debt to their credit report without notifying them first: “They have placed a debt on my credit report for $275 owed to T-Mobile. I called to dispute it because I had just found it on my credit report this morning. The representative hung up on me while I was explaining that I had just pulled my credit report this morning and this was the first time I had seen this.”

There are plenty of other consumers who report that AmSher doesn’t notify them before reporting debts to their credit reports.

What happens when you pay a debt

Paying a debt doesn’t remove it from your report

If you pay a collection account, you may be surprised to learn that it doesn’t get removed from your report. Instead, the status of the account changes from “unpaid collection” to “paid collection.” But the account itself remains on your report, and it still signals to lenders that you had a collection account reported against you at some point.

Paying a collection account doesn’t erase the seven-year clock that starts when you first fail to make a payment. And it doesn’t get the account removed. You’ve just paid for a change in the account status.

That’s why it’s so important to investigate a debt before deciding whether or not to pay it. Before you consider whether you should negotiate and pay, it’s crucial to verify that the debt is accurate, that you owe the correct amount, and that the statute of limitations in your state hasn’t expired.

Why goodwill letters usually don’t work

Some consumers pay a debt and then write a goodwill letter to the collector asking them to remove the account from their credit report as a goodwill gesture. But goodwill letters almost never work when dealing with a collection agency. Unlike the original creditor, who may decide to remove an accurate account because you ask nicely, a third-party collection agency has no incentive to remove a debt that it knows is valid.

Collection agencies aren’t in the business of doing consumers favors. They’re in the business of collecting debts. Once they have your money, you have no leverage to negotiate. If you want an account removed, it’s crucial to do this before you pay, not after. And it’s best to negotiate removal through a strategic dispute, rather than a letter asking for a favor.

How to flip the script and remove a collection account

Why collectors are afraid of the FCRA and FDCPA

The Fair Credit Reporting Act (FCRA) and Fair Debt Collection Practices Act (FDCPA) exist to protect you from collectors who try to coerce you into paying debts you don’t owe. The FCRA requires collectors to verify disputed information within a certain timeframe. If they can’t, they have to remove it. The FDCPA ensures that collectors don’t use abusive or deceptive practices to collect debts. These laws aren’t loopholes. They’re the law.

We already know that AmSher has violated these laws in the past. In 2014, they were sued in federal court by consumers who claimed their collection letters violated the FDCPA because they didn’t properly explain their right to request verification of the debt. The letters also included a deadline for consumers to respond if they wanted to settle their debt, but this deadline was designed to expire before the 30-day deadline that consumers have to request verification.

But to use these laws effectively, you have to understand the intricacies of the procedures involved. There are timing requirements, documentation requirements, and strategic decisions that can determine whether your dispute is successful or not.

The burden of proof is on them

When you dispute a debt, the burden shifts. Instead of assuming you owe the debt and just trying to get you to pay, the burden is now on the collector to prove that you owe the debt and that they have the right to collect it. This can be harder than you think. For example, AmSher may be collecting thousands of debts, and may not have documentation for all of them. The debt may have been sold multiple times, and the documentation may not have been transferred with it.

Consider what happened to this consumer, who posted on WalletHub about their experience with AmSher: “They are attempting to collect on a fraudulent charge that they put on my credit report from Charter Communications. I have never done business with Charter Communications. I called them and they told me that I had no record of transactions with them. I disputed it with Experian and they told me that AmSher verified that I owed the debt. This is totally and completely fraud.”

This is a perfect example of what can happen when a collector confirms a debt without documentation.

When the consumer disputed the debt with Experian, AmSher confirmed that the debt was valid. But this doesn’t mean they verified it with documentation. To force a collector to truly verify a debt, you need to request actual proof in a dispute letter.

Why professional help is the best way to dispute a debt

The knowledge gap

Collection agencies are staffed with professionals who understand credit reporting and the laws that govern it. They understand what language keeps them safe. They understand how to document files so they can survive consumer challenges. And they understand timing tricks and verification shortcuts.

But consumers have a lot of other things going on in their lives. They’re working, taking care of kids, and trying to manage their daily lives. The information gap between consumers and collectors is huge. Collectors deal with challenges like this every day. Most consumers only have to deal with them once or twice in a lifetime.

This is why it’s so important to have professional help. Credit repair professionals understand not just what the law says, but how to use it to your advantage. They understand which disputes trigger which obligations. And they understand the procedure technicalities that can invalidate a collection account entirely.

Remaining silent can be golden

One of the most important things to understand when dealing with a collection agency is the importance of silence. When you talk to a collector on the phone, everything you say can be used against you. If you admit that you owe a debt, or promise to pay it, you can restart the clock on the statute of limitations. And you can create a trail of evidence that the collector can use against you.

But professional credit repair works differently. Written disputes create a paper trail that works in your favor. And silence prevents you from making dangerous verbal admissions.

Consider what happened to this reviewer on the Better Business Bureau website, who claimed that a manager at AmSher called them and was “one of the rudest people I’ve ever spoke with in my life.” The manager allegedly told the consumer, “I know you can afford this payment because I know you have a mortgage in your name.”

Direct interactions with collectors can go wrong like this. And there’s rarely a benefit to engaging with them directly.

Reclaiming your financial identity

It’s not just about your credit score

The purpose of disputing a collection account isn’t just to improve your credit score. It’s to reclaim your financial identity. When someone else gets to decide what your credit report says about you, they define your financial identity for you. When you allow an unverified collection account to remain on your credit report, you allow someone else to describe your financial history.

If you don’t force the collector to verify that a debt is accurate and valid, you’re allowing them to control your financial identity. Based on what we know about AmSher, this could mean allowing a company that doesn’t always notify consumers before reporting debts to their credit reports, may be collecting debts you don’t actually owe, and may not have the documentation to prove its debts collect debts from you.

Reclaiming your financial identity means refusing to allow someone else to control your financial story. It means exercising your legal right to force anyone who reports information about you to the credit reporting agencies to prove that it’s accurate.

What to do when you see AmSher on your report

The path forward

If you see AmSher Collection Services on your report, there’s no need to panic. Instead of allowing fear to force you into paying a debt you may or may not owe, it’s time to take a step back.

Based on AmSher’s history, it’s entirely possible that you can get this account removed from your report. In fact, AmSher paid almost $1 million to settle claims that it made illegal robocalls to consumers, and it has received more than 2,000 complaints from consumers.

Remember, collection accounts can be removed from your credit report if they contain inaccurate information, or if they’re simply invalid, erroneous, or fraudulent. Given that most credit reports contain errors, you should always assume the burden is on the collector to verify the account, rather than on you to assume you owe it.

So the real question isn’t whether you should challenge the account. It’s whether you should do it yourself or work with a professional to help you. Given the procedural technicalities, strategic considerations, and documentation requirements for a successful dispute, the answer is clear.

Conclusion

AmSher Collection Services has been around for nearly 40 years, racking up regulatory actions, class-action settlements, and thousands of consumer complaints along the way. The company relies on consumers who react to accounts from AmSher with fear, pay debts without requesting verification, and never learn their rights under federal law.

But you don’t have to play along. Instead of paying a debt without investigating whether you owe it, it’s time to turn the tables. Investigate before you negotiate. Verify before you pay. And get professional help before you try to go it alone. These principles can help you challenge the debts that collectors assume you won’t challenge.

Get help today

At FightCollections.com, we can help you fight back against debt collectors like AmSher Collection Services. We understand the procedure technicalities, documentation requirements, and strategic decisions that can help you successfully dispute invalid collection accounts. We’ll analyze your situation and identify any inaccuracies that can help us get the account removed.

Don’t let a company with AmSher’s history define your financial future. Contact us at FightCollections.com today for a free consultation. We’ll help you fight back against collectors who assume you won’t challenge them. Your credit report is your financial story. Make sure it’s an accurate one.