When you find an unexpected debt collection on your credit report, it can feel like someone has placed a boulder in the middle of the road on the way to your financial objectives.

If the collection agency is a medical debt collector with a questionable reputation like ARstrat, you might start feeling a bit of panic.

Here is the truth: this is not the end of your credit story. In fact, it is just the beginning of a new chapter, a chapter in which you learn your credit rights and exercise them to delete any reporting inaccuracies or unverifiable information from your credit history. Did you know that a study done by U.S. PIRGs found that 79% of credit reports contain errors or other major mistakes? Based on that figure alone, the ARstrat collection on your report may not be as solid as the debt collector wants you to think it is.

In this article, we will explain what ARstrat is, why the debt collector has a questionable reputation, and, most importantly, why disputing the account may be the first step to your credit repair.

Who is ARstrat?

ARstrat, LLC (Account Resolution Strategies) is a Texas debt collection agency that focuses on medical debt collection. The company was founded in 2007 and is based out of several locations throughout Texas. Here is the business information for ARstrat:

ARstrat collects debts for hospitals, clinics, physician groups, labs, imaging centers, and other medical facilities. They report their collection accounts to the three major credit reporting bureaus (CRAs), which means you may see the collection on your Equifax, Experian, or TransUnion credit report.

A History of Consumer Complaints

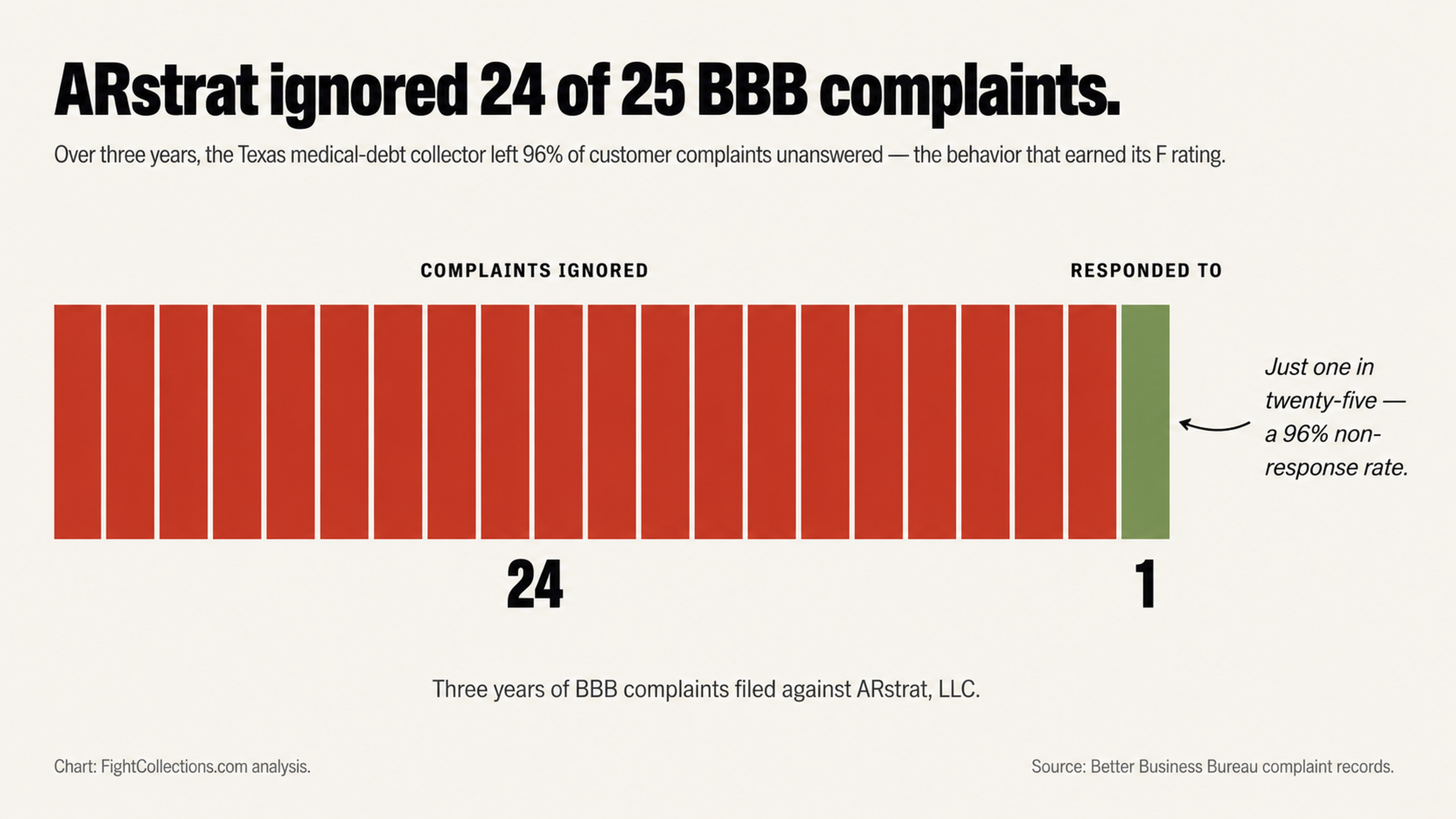

The Better Business Bureau (BBB) rates ARstrat an F, the lowest rating possible. The reason for the failing grade? Of 25 customer complaints filed against ARstrat in the last three years, the debt collector failed to respond to 24 of them. That means ARstrat has a 96% non-response rate to customer complaints.

ARstrat has been named as a defendant in more than 60 federal court cases, according to the Consumer Advocates website. At least 12 class-action lawsuits alleging Fair Debt Collection Practices Act (FDCPA) violations have been filed against ARstrat between 2016 and 2025, reports ClassAction.org. The Consumer Financial Protection Bureau (CFPB) complaint database lists 14 complaints related to ARstrat’s debt collection practices.

As for consumer reviews, here is what one BBB customer wrote: “This company has called SEVERAL times a day and SEVERAL times a week. Each time I answer I’m placed on hold for 4 to 30 minutes. Then when someone comes on they go through their whole deal of being a collection company... She then hung up on me. I have received NOTHING in the mail from them.”

Debt collection agencies do not rely on customer service for their business model. That is why poor ratings and complaints will not change their behavior. Unlike other service-based industries, debt collectors get paid by the original creditor, not the consumer. Understanding this may help you recognize why direct communication with a debt collector rarely results in a positive outcome for consumers.

Why You Should Not Pay ARstrat First

The “Pay and Forget” Problem

When you find a debt collection on your credit report, you may feel the urge to pay it immediately and forget about it. We understand. The reaction is very common. However, before you pay, recognize how the payment will affect your credit report.

When you pay a collection account, the account does not get deleted from your report. Instead, the collection status changes from “unpaid collection” to “paid collection,” and the account remains on your report for approximately seven years.

You may have heard of “pay for delete” agreements in which a debt collector agrees to delete the account from your report in exchange for payment. Unfortunately, such agreements rarely work as promised. The debt collector may agree to delete the account and then fail to follow through. Alternatively, the collector may delete the account, and then the account comes back after a few months. Either way, the outcome is the same: you paid the account, which reactivates the collection process, but the negative account remains on your report.

Instead of paying the account, you may consider disputing it first. This is not a strategy to avoid your legitimate financial obligations. Instead, this is a strategy to ensure only accurate and verifiable information is reporting on your credit report, which is your right under the Fair Credit Reporting Act (FCRA).

The Missing Information Problem

Medical debt often changes hands several times before it ends up at the desk of a debt collector like ARstrat. The original healthcare provider may send the debt to their in-house billing department, then to their internal collections department, and then to a third-party debt collector like ARstrat. With each transfer, the risk of lost documentation, errors, or broken chains of ownership increases.

Several FDCPA lawsuits against ARstrat have alleged the debt collector’s failure to identify the original creditor, use deceptive collection letters, and issue inadequate debt validation responses. Instead of isolated incidents, these may be patterns that indicate a problem with documentation.

If a debt collector cannot verify a collection account, you can dispute it and potentially remove it from your report. The systematic credit repair process relies on these common documentation problems to dispute questionable information on credit reports. There is nothing shady or unethical about using documentation and process to challenge credit report information. In fact, that is your right under consumer protection laws that exist because the debt collection industry has a history of abusive practices.

The Problem with Talking to Debt Collectors

Phone Calls Can Be Hazardous to Your Wealth

If you are getting calls from ARstrat, do not respond. Phone calls with debt collectors present a significant risk to consumers. Not only do phone calls lack a paper trail of what was discussed, but phone calls can also lead to miscommunications about the terms of a payment agreement. Moreover, debt collectors can use phone calls to fish for information or manipulate you into saying something that incriminates you.

Several BBB complaints accuse ARstrat of making aggressive phone calls, including calling several times a day, calling as early as 6:00 a.m., robocalls that place consumers on hold for several minutes before connecting to an agent, and one consumer claimed the company called more than 100 times in a single month. These calls are designed to harass you until you respond.

Debt Collectors Are Trained Persuaders

Debt collectors are trained to get a response out of you. They know which psychological buttons to push, which words to use, and how to use your emotions against you. They understand how to create a sense of urgency, how to prey on your fear of the unknown, and how to make you think paying the debt is the only option.

When you get a call from a debt collector, you are at an informational disadvantage. The debt collector has all the information about your account and knows exactly what to say. In contrast, you may know little about the debt or your rights under federal and state law.

Silence Is Your Best Defense

Not returning a debt collector’s calls is not avoidance; it is a strategy. With each call, you give the debt collector another opportunity to build its case against you. When you let a professional handle the communication on your behalf, you protect yourself and preserve your options.

Compare ARstrat’s claims of compliance to its actual practices. On its website the debt collector claims it has a “strong emphasis on compliance” with federal consumer protection laws. Yet the 60-plus federal court cases, the F rating from the BBB, and the recurring customer complaints tell a different story. That contrast should tell you to approach any direct communication with the company with caution.

Written disputes through proper channels create a paper trail and invoke specific legal protections. Under the FDCPA, debt collectors must validate disputed debts. Often, when debt collectors receive a proper validation request, they cannot produce the necessary documentation. That is how the dispute process gives you leverage that phone calls never can.

Starting Your Credit Repair Story

The Dispute Process Is Your First Step

Removing an ARstrat debt collection from your credit report is not just a defensive action; it is also the first step to your credit repair story. When you remove inaccurate, erroneous, fraudulent, or unverifiable information from your credit report, you make room for positive credit information to tell the story of your true creditworthiness.

The FCRA says information on your credit report must be accurate, complete, and verifiable. If any of those three elements is missing from the ARstrat collection on your report, you have a reason to dispute it. Given the documentation issues that have arisen in FDCPA cases against this debt collector, you may have reason to believe the ARstrat account on your report cannot meet those standards.

Credit Reporting Bureaus (CRAs) have 30 days to investigate disputes. If a debt collector cannot verify a disputed account during the allowed time, the CRA must delete the disputed information. This is not a loophole or trick; this is the law working the way it is supposed to work to protect consumers from unsubstantiated negative reporting.

Why You Need a Professional

Debt collectors and credit reporting bureaus understand the dispute process and may have experience with it. Chances are good you do not. If you try to handle the dispute yourself, you can easily make a mistake that may strengthen the debt collector’s position.

A credit repair professional, however, works with these situations every day. The professional understands which documentation problems are most common, how to word an effective dispute letter, and how to escalate a dispute that is not resolved through the first round. The professional also knows when a debt collector is likely to push back and when it will delete the account. With professional help, you can tailor your approach to your circumstances.

The complexity of medical debt collection makes professional help especially valuable. Medical billing involves insurance adjustments, provider networks, charity care policies, and medical billing codes, all of which can create points of error. A debt collection account may look solid to the debt collector but have significant problems that only a professional may recognize.

Life After an ARstrat Dispute

Your Future Credit Is Not Defined by Your Past

Seeing an ARstrat collection on your credit report may feel like a judgment about your past. The truth is, however, the collection is only an accusation. The debt collector’s assertion that you owe a debt does not make it true, complete, or verifiable. The debt collector’s decision to report the debt to the CRAs does not mean the debt will remain on your report after you challenge it.

Every day, consumers successfully dispute and remove collection accounts from their credit reports. In fact, the 79% error rate in credit reporting exists because debt collectors like ARstrat report as aggressively as possible without always having the documentation to back their claims. You could be one of those errors waiting to be corrected.

Imagine where you want to be in six months, one year, or five years. Do you want to buy a house? Qualify for lower interest rates? Enjoy the peace of mind that comes with a clean credit report? Whatever your goal, the process starts with cleaning up any obstacles currently standing in your way. ARstrat does not have to be a permanent part of that obstacle course.

The Choice Is Yours

You can continue to get calls, feel anxious whenever you see an unknown number on your phone, and watch as the collection account harms your credit score. Or you can take the first step toward resolving the account by challenging whether it belongs on your report at all.

The data is in: ARstrat has a history of complaints, lawsuits, and regulatory issues. The debt collector’s 96% non-response rate to BBB complaints suggests it may respond the same way to validation requests. That behavior could work to your advantage if you approach the account through the proper dispute channels.

Your credit report tells a story about you. Right now, it may include a chapter written by ARstrat. However, you have the power to edit that chapter, dispute information that does not belong, and author a new chapter that reflects your true financial responsibility.

Conclusion

Start Your Credit Repair Journey Now

ARstrat debt collections do not have to remain on your credit report. With the right strategy, you can dispute and remove unverifiable or inaccurate collection accounts and start your journey toward the credit report you deserve.

FightCollections.com helps consumers fight debt collectors and remove questionable collection accounts from their credit reports. We understand the documentation issues that plague debt collection agencies like ARstrat, and we know how to use those issues to your advantage.

Do not let another day go by with an ARstrat collection affecting your credit and your quality of life. Contact FightCollections.com today for a free consultation. Let us evaluate your situation, review the ARstrat account on your report, and explain how the dispute process can help you start your credit repair journey. Your next chapter starts now.