Are you worried that you have an account with a collection agency called Atlantic Recovery Solutions on your credit report?

Don’t panic. You’re not alone. Every day, thousands of people just like you receive collection notices from debt collectors they’ve never heard of for debts they don’t remember owing.

It’s not about whether or not you actually owe the money. It’s about whether or not the information the credit bureaus have on you is accurate, up-to-date, and compliant with the law.

According to a study by U.S. PIRG, 79% of credit reports contain errors or disputes. Nearly 4 in 5 credit reports contain mistakes. Before you accept any collection account as legitimate, it’s time to take a closer look at the system.

Your next 5 days are crucial.

Most people react emotionally. They pull out their wallet and pay. Sometimes, this doesn’t work out so well. A paid collection can still hurt your credit report. It can still ding your credit score years after you’ve paid.

Atlantic Recovery Solutions, LLC is a third-party debt collection agency. It has a mailing address in New York. Before we go any further, you should know exactly who is trying to collect from you.

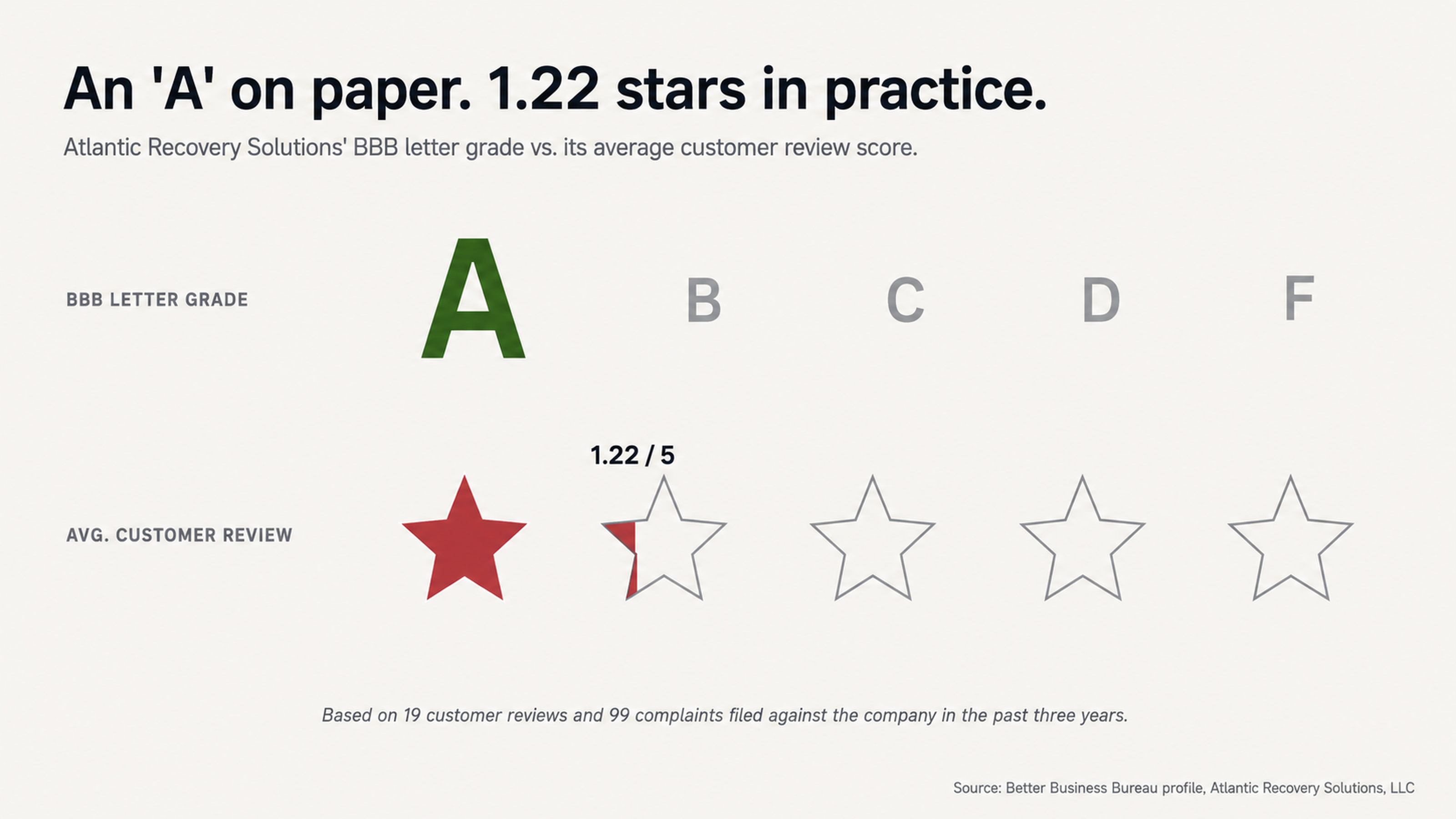

Do you see what’s happening here? This collection agency has an A rating from the Better Business Bureau. At the same time, it has an average customer review of just 1.22 out of 5 stars. The disconnect between a collection agency’s official rating and what’s actually happening to consumers tells you something about how little you can trust these ratings.

Publicly Available Information

Over the last three years, Atlantic Recovery Solutions has racked up 99 complaints with the BBB. In the last year alone, it has closed 47 of these complaints. Since 2013, the Consumer Financial Protection Bureau’s database contains 87-123 complaints about this collection agency.

At least 31 federal lawsuits have been filed against Atlantic Recovery Solutions. The most significant was a class action settlement in 2024. The company agreed to pay $51,975 to approximately 297 California consumers who received unlawful voicemails and text messages. Although the company did not admit any wrongdoing, actions speak louder than words.

Many consumers have complained about Atlantic Recovery Solutions calling them 20-50 times a day. They complain about the company contacting family members and employers. They complain about trying to collect time-barred debts or debts they don’t actually owe.

Do You Actually Owe This Debt?

Could It Be a Case of Mistaken Identity?

When was the last time you confirmed that the debt Atlantic Recovery Solutions is trying to collect actually belongs to you?

Debt collectors get it wrong all the time. Sometimes it’s a case of mistaken identity. Sometimes they confuse you with someone who has a similar name. Other times they confuse you with a family member.

The debt collection industry makes money buying up defaulted debt portfolios from original creditors. They pay just pennies on the dollar. Each time the debt changes hands, pieces of information can get lost or corrupted.

By the time Atlantic Recovery Solutions reaches out to you, they may not have all the original information about your debt. They may not have any information about your debt at all.

Have you ever had an account with the original creditor? Do the dates add up? Does the amount make sense? If any single piece of information seems off, that’s what you should focus on.

What Proof Do They Actually Have?

Here’s a question most consumers never ask. Can this debt collection agency prove that you actually owe this debt?

Under federal law, a debt collector must verify a debt if you request it. They must provide documentation of the original creditor, the original amount, and the chain of ownership.

The truth is, most collection accounts can’t pass this test. Most of the time, the documentation simply doesn’t exist. When debts are bought and sold and bundled together, the paperwork gets lost. The debt collector may have a spreadsheet with your name and a balance due, but a spreadsheet isn’t proof.

Many of the complaints about Atlantic Recovery Solutions revolve around their failure to validate a debt. One consumer reported asking for a letter to show they owed the debt. Instead, the agent became rude and threatening.

Another consumer reported that they never received written communication even though the company claimed they had sent letters. These patterns suggest that when consumers request verification, they may be exposing a weakness in the debt collection process.

Can You Spot the Warning Signs?

Which Behaviors Should Raise a Red Flag?

Does this debt collector demand immediate payment without giving you time to verify the debt? Are they threatening to sue you, garnish your wages, or have you arrested? Are they refusing to provide you with written information about what you owe?

These behaviors aren’t just pushy. They may actually be against the law.

The whole purpose of the Fair Debt Collection Practices Act is to prevent debt collectors from using fear and urgency to force consumers to pay debts they may not owe. Real debt collectors will provide you with documentation. They will give you time to respond. They will operate within the bounds of the law.

One review on the BBB website reported being belittled and harassed over the phone about a time-barred debt. Another complaint reported being talked down to because she was a woman. When debt collectors try to shame you or intimidate you or talk down to you, they’re trying to bypass your rational brain and trigger an emotional response.

Are They Involving People They Shouldn’t?

Has Atlantic Recovery Solutions contacted your family members, your employer, or other third parties?

This is one of the most common complaints about the company. Under federal law, debt collectors may contact third parties to request location information. However, they are not allowed to discuss your debt with your family members, your coworkers, or your neighbors.

One particularly egregious complaint reported that Atlantic Recovery Solutions contacted three different family members in a single day. They called an ex-spouse, a daughter, and a brother. Another complaint reported that the company called a 15-year-old grandchild.

In 2015, a federal lawsuit alleged that the company contacted an 83-year-old mother and told her she was required to give them her son’s contact information. They scared her so badly that she inadvertently gave them her own credit card information. They charged her over $5,000.

When debt collectors are calling your family members or your friends or your employer, they’re counting on your embarrassment or your sense of social obligation to get you to pay up. This is using your relationships against you. In some cases, it may be against the law.

What Are Your Rights?

Do You Know What Federal Law Says?

You might not be aware that federal and state laws offer considerable protections from debt collection abuse. Most people aren’t. Debt collection companies rely on this fact. They act as if they have authority, as if you have no choice but to do what they tell you.

Federal laws like the Fair Debt Collection Practices Act (FDCPA) bar harassment, misrepresentation, and other predatory practices. The Fair Credit Reporting Act (FCRA) requires credit report data to be both accurate and verifiable. If a debt collection company can’t verify information it’s reporting, then credit reporting agencies (CRAs) have to delete it.

Individual states may offer additional legal protections. Some states impose statutes of limitation on debt collection. This means that debt collection companies can’t sue you for debts older than a certain age. Some states offer greater protection against wage garnishment, bank account levies, and other asset seizures than federal law does. The threats a debt collector makes may not even be legal in your state.

Why Ignoring Them Strengthens Your Position

Have you considered that ignoring them might be the best thing you can do?

Every time you communicate with a debt collector, you’re giving them an opportunity. You might provide them with information they need, confirm your identity, or agree to some sort of payment plan. Meanwhile, you’re not getting anything in return.

Debt collection representatives receive training in persuasion. They know which emotional buttons to push. They can make you feel guilty, fearful, or desperate. They may tell you that you’re lucky they’re willing to settle with you. They may warn you that refusing to cooperate will have serious consequences. These are sales tactics, not statements of fact.

When you dispute a debt through the proper channels instead of negotiating directly with the debt collector, you shift the burden of responsibility to them. They must prove their claims. They must provide documentation. They must meet deadlines. The less you interact with them directly, the more power you retain.

Should You Just Pay Them?

What Happens To Your Credit Score

Will paying Atlantic Recovery Solutions help your credit score? This is a question that we think consumers should ask themselves more often. The answer seems so obvious: yes, of course. Pay the debt. It will go away.

The truth is more complex. Paying a debt collection does not remove it from your credit report.

Yes, you read that right.

If you allow a collection to remain on your credit report and then pay it, the status of the account will change from “unpaid collection” to “paid collection.” The negative account will still be on your report, though. And, according to the current rules of credit reporting, it can continue to harm your credit score for as long as 7 years from the date of the original delinquency.

Some credit scoring models no longer count collections against you if you pay them. But many lenders still use the older models that do include paid collections. In particular, mortgage lenders may use credit scoring models that penalize consumers for any type of collection account, even if it’s paid.

You could pay Atlantic Recovery Solutions today. But you might still be denied a loan or face higher interest rates 5 years from now because of it.

What If Any Part of It is Incorrect

Do You Know Whether the Information Is Accurate

Have you confirmed that every piece of information about this collection account is true? The balance? The dates? The original creditor? Your contact information?

If any one piece of information is incorrect, you may have grounds to dispute the entire account.

The credit reporting agencies (CRAs) must investigate any disputes you initiate. They must remove any information that they cannot verify. Debt collection agencies must respond to these investigations within a certain amount of time. If they don’t meet this deadline – or if they can’t provide adequate documentation to support their claims – then the CRAs must delete the account from your report.

According to research from consumer advocacy groups, nearly 80 percent of credit reports contain some kind of error. This means that the chances are high that something is wrong with this account.

Disputing errors isn’t about trying to get out of a legitimate debt. It’s about making sure that only legitimate, verifiable information appears on your credit report.

Can You Do This On Your Own

Do You Have the Time

How much time and effort can you spare to research your debt collection rights, craft a proper dispute letter, monitor deadlines, and follow up with CRAs?

The process of disputing a debt collection account is technical. There are procedures you must follow and deadlines you must meet. One misstep at any point in the process could invalidate your entire dispute.

Debt collection companies have experience with debt collection disputes. In fact, that’s what they do. They have people on staff whose only job is to respond to consumer disputes. When you try to represent yourself, you’re going up against professionals whose job it is to know more about this than you do.

There’s also an enormous information disparity between debt collection companies and individual consumers. They know what documentation they have and what they don’t. They know which of their allegations will stand up under scrutiny and which won’t. They use this information to decide how hard to pursue individual consumers. You’re playing a game without knowing all the rules.

What a Professional Can Do For You

Have you considered what a credit repair expert can do for you that you can’t do for yourself?

Professionals who specialize in disputing collection accounts know the rules of the game. They understand the technical procedures and the legal technicalities. They have experience dealing with companies like Atlantic Recovery Solutions. They know which types of disputes are most likely to succeed. They know how to document everything properly. They know how to force CRAs to take additional steps when their initial response isn’t adequate.

Most importantly, they can save you the time and hassle of doing all of this yourself so that you can get on with your life.

You’re not trying to get out of a debt that you legitimately owe. You’re trying to make sure that your credit report is an accurate reflection of your history and habits as a consumer. And you’re trying to make sure that debt collection companies obey the law when they pursue you.

When the stakes are this high, expert guidance can make a big difference.

In Conclusion

A representative from Atlantic Recovery Solutions has contacted you. Now what?

You can respond emotionally. You can pay what they say you owe and hope that your credit score improves. Or you can step back, ask yourself the right questions, and come up with a strategic plan.

The public record indicates that this is a company with almost 100 complaints through the Better Business Bureau (BBB) over just a 3-year period. It’s a company that just paid a class-action settlement of almost $52,000. It’s a company that has been sued in federal court at least 31 times. It’s a company with a customer review rating of just over 1 star.

Complainants accuse the company of harassing phone calls. Of communicating with third parties. Of trying to collect debts that the consumer doesn’t think are legitimate or that are too old to collect.

This is the kind of information you should keep in mind when you formulate your response.

Remember that paying a debt collection doesn’t mean it will disappear. Remember that debt collectors use urgency and fear to get you to do something without thinking. And remember that you have legal rights that protect you from both harassment and abuse.

Most importantly, remember that you always have the right to verify any information that a debt collector says you owe before you pay them a dime.

What’s Your Next Move

If you want to protect your credit score, the first thing you should always do is dispute any information on your credit report that you believe is inaccurate, erroneous, or unverifiable.

This isn’t about trying to get out of something you owe. This is about making sure that only correct information appears on your credit report.

At CollectionsRelief.com, we specialize in empowering consumers to dispute collection accounts they don’t think belong on their credit reports. We understand the dispute process. We understand your legal rights. And we understand the games that companies like Atlantic Recovery Solutions play.

We prepare all of the documentation. We track all of the deadlines. And we do all of the follow-up so that you don’t have to go through this process by yourself.

If you’re looking at a credit report and you see an account from Atlantic Recovery Solutions on it, then we encourage you to contact us today to schedule a free consultation. We can help you understand your options before you do anything that may impact your credit report for years to come.