Marcus was reviewing his credit report prior to applying for a mortgage when he saw an unfamiliar account. Cavalry SPV I LLC was listed as a collection agency and the account reflected an alleged debt of $4,200.

Marcus had never heard of the agency, never received a letter from them, and could not identify the debt as one that he owed or had ever owed.

Marcus’s situation is far from unique. U.S. PIRGs has reported that as many as 79% of credit reports contain errors or other mistakes. Consumers often find mysterious collection accounts that they cannot identify, debts that were previously paid, or balances that do not correspond with any obligation the consumer has ever incurred.

The desire to simply call the phone number on the credit report and clear up the issue is very tempting. But giving in to this temptation frequently leads consumers into snares that work to the advantage of collectors and to the disadvantage of consumers attempting to correct their credit report.

Who is Cavalry SPV I LLC?

Cavalry SPV I, LLC is a Delaware corporation that was registered with the Delaware Secretary of State on June 5, 2002. The company is registered as a Special Purpose Vehicle (SPV) that purchases and owns portfolios of delinquent debts. The SPV is a business entity that is separate and distinct from other aspects of the business and ownership of Cavalry Investments, LLC.

A History of Regulatory Issues and Customer Complaints

Over 3,450 complaints have been filed against Cavalry entities with the Consumer Financial Protection Bureau database, of which 83.6% involve debt collection issues. The Better Business Bureau has received 617 complaints over the past three years alone. And 71% of 124 reviews on WalletHub have a one-star rating.

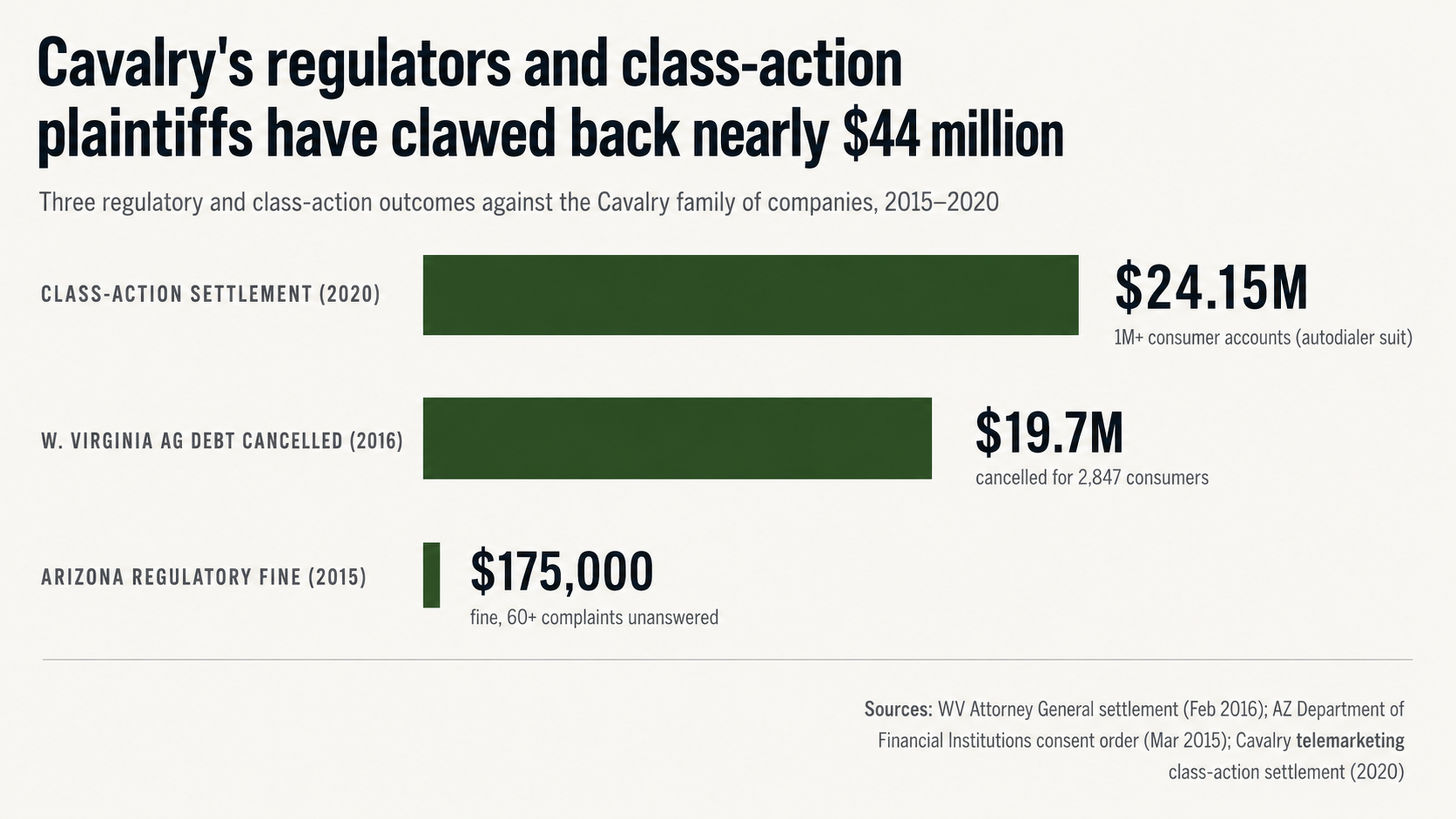

So what types of problems have other customers encountered? Well, In 2016, West Virginia Attorney General Patrick Morrisey reached a settlement with Cavalry, following an investigation that revealed the company had been attempting to collect debts in the state without being properly licensed or holding a surety bond, as required by law. As a result of the settlement, 2,847 consumers saw 19.7 million in debt canceled and Cavalry paid 350,000 to the state.

In March 2015, Arizona regulators fined Cavalry 175,000 after looking into more than 60 customer complaints filed between 2007 and 2013. The investigation revealed that Cavalry had consistently failed to respond to customer requests to validate debts, which is a right protected under federal law.

Why Calling the Collection Agency is a Recipe for Disaster

The Urgency Game

Marcus was very close to making a huge mistake. When he clicked on the Cavalry SPV I LLC listing, he noticed a phone number was displayed and seriously considered calling to clear up the matter. But that is exactly what debt collectors want you to do.

Debt collection representatives are incentivized to create a sense of urgency. They may indicate that a payment is needed right away in order to avoid a lawsuit, that a settlement offer is only good for a short period of time or that a consumer’s credit score is in such bad shape that it requires immediate attention.

In nearly all cases, however, the sense of urgency is fabricated. A debt that has already been sold to a third party, such as Cavalry SPV I LLC, has probably already been delinquent for months or even years. So it isn’t going to hurt anything to wait a few days or weeks to confirm the debt is valid. The phone number on your credit report is there for one reason and one reason only: to facilitate your request for the debt collector to prove the debt is valid, not to set up a payment plan.

Phone Conversations Can Establish Liability

When you call a debt collector, the conversation is recorded. And anything you say can be used to establish that you acknowledge the debt, restart the clock on the statute of limitations or serve as ammunition for future collection attempts. Even stating something as seemingly innocuous as My name is and my Social Security number is or Can you tell me how much I owe? can have legal implications.

Cavalry, in particular, has a history of using phone calls as a collection tactic. In fact, the company just paid 24.15 million to settle a class-action lawsuit covering more than 1 million consumer accounts, alleging it used an automatic dialing system to call consumers without their consent between 2009 and 2016.

One consumer complaint described the experience like this: Calvary Portfolio Services has called my place of employment 5 times. Calvary Portfolio Services calls my personal phone at least 10 times a day everyday. Needless to say, such behavior benefits the collector, not the consumer.

Inside the Debt Buying Industry

Debts Are Sold for Pennies

Debt buyers, like Cavalry SPV I LLC, do not pay full price for the accounts they purchase. In fact, portfolios of charged-off debt generally change hands for three to seven cents on the dollar, or even less in some cases. So if there is a 4,200 collection account from Cavalry on your credit report, it’s possible the company paid less than 300 for it.

That would explain why debt collectors are so eager to collect the full amount and why they’re often willing to settle for far less. It also means any amount the consumer pays (above what the debt collector paid for the debt) is pure profit. And if the debt collector is willing to settle, it’s a sign they know they may have trouble validating the debt.

Incomplete Documentation Offers Opportunity

Michigan litigation has shined a light on how Cavalry may handle instances where documentation is missing. In the Partridge et al v. Weber and Olcese lawsuit, the plaintiffs alleged that Cavalry used robo-notarized affidavits to file collection lawsuits. According to a complaint filed in the case, false verifications were used to circumvent the cost of actually verifying that the company owned the debt, creating a false sense of burden on consumers, who then believed they had to respond to what they thought were valid legal claims.

One customer review relayed a similar experience: They report inaccurate information on your credit. They intimidate and harass people. They use illegal tactics like fake affidavits and filing multiple lawsuits. If a debt collector cannot verify that it actually owns what it claims it owns, consumers who challenge it through the proper channels often emerge victorious.

A Guide to Disputing a Debt

How Credit Reporting Works

Marcus learned that credit bureaus serve as middlemen between data furnishers (in this case, a debt collector) and consumers. Under the Fair Credit Reporting Act (FCRA), the credit bureau has 30 days to investigate a dispute. It will reach out to the data furnisher, request verification and, if the data cannot be verified or is found to be inaccurate, it must be removed from your credit report.

This process allows you to bypass the debt collector. Instead of negotiating with Cavalry SPV I LLC directly, you file a dispute, and then the credit bureau demands the debt collector prove the account is both accurate and yours.

Given that Cavalry has been fined for not responding to such requests for validation (that’s why Arizona imposed a 175,000 penalty), filing a dispute offers consumers a lot of leverage. In cases where the debt collector cannot respond or fails to verify, the account must be deleted.

Grounds for Dismissal

You can have a collection account removed from your credit report if the information is inaccurate, the debt cannot be verified within the allotted time, the account is not yours or if no documentation exists to support the debt. That last point is particularly relevant when dealing with debts that have been sold to a third party.

Marcus realized he had a few potential problems with the Cavalry listing on his credit report. For starters, the amount did not match any debt he recognized. The original creditor was a company he had never heard of. And the dates did not match any of his financial activity.

Each of those represents a legitimate reason to dispute a credit report listing. (Credit repair experts are trained to identify such discrepancies and properly document them in a way that will result in removal, whenever possible.)

When Paying a Collection Account Hurts

Paid Collection Accounts Don’t Always Disappear from Your Report

Perhaps counterintuitively, paying a collection account does not mean it will be removed from your credit report. When you pay, the status will be updated to paid, but the collection account will still remain on your credit report for up to seven years from its original delinquency date.

Lots of people pay off debts because they think doing so will get the account removed from their report, but they are often surprised to find the account is still listed, long after they’ve paid. In fact, in some credit scoring models, a paid collection account may actually have a negative effect.

Here’s how one Cavalry customer described a similar experience: An offer was sent to Cavalry. The debt was approx 6500. They charged me with $23,136.45. I sent an offer and they sent me a letter of acceptance to release the lien and negative credit report. I certified a check in the agreed balance, plus sent it certified mail with return signature. Both returned signature and certified bank check cleared. They have not released the lien or said anything on my credit report.

Why Removal Offers More Permanent Results

If a collection account is successfully disputed and removed from your credit report, it is likely to stay that way. A debt collector generally will not have the mechanism or the incentive to get the account re-reported, since the same dispute would simply be repeated.

That’s why, in many cases, disputing is a better option for consumers than paying a debt they find questionable. (For more, check out our guide on Pay for Delete letters.)

I would like to go back to the drawing board and try to mediate, one customer wrote on the Consumer Affairs website. I did not ask them to report this account to the credit bureau in the first place and would like for it to be removed at this point. That’s the right strategy.

Professional Help

Professional Help Is Often Necessary — Here’s Why

Consumers who try to deal with debt collectors on their own are at a distinct disadvantage. The debt collection agency has all the leverage. Debt collectors understand the credit reporting system inside and out. They know which tactics work and which mistakes consumers can make to their disadvantage. And they deal with thousands of consumers every month. They’ve seen every technique consumers try.

Consumers, on the other hand, generally only deal with debt collectors every few years, at most. They may not know if the situation they find themselves in is normal or not. And they may not recognize when a debt collector is violating their rights or how missing documentation can help their case.

Here’s what one Cavalry customer wrote: The debt cannot be validated despite many attempts over the years to have them do so. They refuse to remove the account despite not having the correct information from whoever they bought it from. In many instances, consumers who can’t succeed on their own need professional help to remove inaccurate information.

What a Credit Repair Expert Can Do

A credit repair expert can offer the expertise consumers often lack. They can help figure out which discrepancies are most important and how to document them properly so they can be most effective in a credit report dispute. They’re familiar with federal and state laws governing credit repair, including the Fair Credit Reporting Act (FCRA) and the Fair Debt Collection Practices Act (FDCPA).

And, perhaps most importantly, they can handle all communication so consumers do not have to. That means consumers can avoid phone calls with debt collectors that could establish liability and ensure all communication with collectors and credit bureaus happens the way it is supposed to — the right way.

This process should not be about helping consumers game the system to get out of debts they owe. Rather, it’s about ensuring consumers are not held responsible for debts they do not owe or for accounts that are not reported correctly.

The End Result

In total, Cavalry SPV I LLC (and its affiliates) has been forced to pay more than 24 million in settlements for a class-action lawsuit, 19.7 million in debt cancellations, stemming from a state’s attorney general’s investigation, and hundreds of thousands of dollars in fines imposed by various state regulators. And that’s not counting the number of consumers who have successfully had debts invalidated.

Given the company’s history of failing to validate debts, its use of abusive telemarketing tactics and its history of faulty documentation procedures, there are probably a lot of people who can have the same success that Marcus did.

The big takeaway Marcus learned, one that would help anyone who discovers Cavalry SPV I LLC on their credit report, is that no response and a formal dispute are your friends. The phone number on your credit report isn’t there for you to call to work out a deal. The urgency a debt collector tries to create is manufactured. And the fastest way to a clean credit report may not involve paying a collection account but disputing it instead.

Take the First Step Right Now

If you have a Cavalry SPV I LLC listing on your credit report and you’re not sure what to do or need help navigating the process, you should know that FightCollections.com specializes in empowering consumers in disputes with collection agencies like Cavalry. We know all of the particular weaknesses in Cavalry’s documentation and credit reporting processes and we know which types of disputes work and how to pursue them.

For a free consultation, contact us today. We can take a closer look at your credit report, help you identify any potential inaccuracies and come up with a plan for how to tackle your collection accounts the right way. You have the right to a credit report that accurately reflects your history, not one marred by unverified debts being collected by a company with a history of compliance issues.