CCS Companies may contact you directly to collect a debt. Your initial reaction may be to call them and straighten out the situation. This is what they hope you will do.

Before you do anything, it is crucial that you understand the situation and why paying the debt or explaining it to them will not be to your advantage. Debt collection is a business and it does not work the way you might expect. Here is why.

Debt collection companies work on volume and speed. The faster they can process a debt the faster they get paid. Research from U.S. PIRGs found that 79% of credit reports contain mistakes or serious errors. The original creditor may sell off your debt without sending any documentation.

On top of the paperwork issue, the debt collection business has a high rate of employee turnover. What this means to you is that the person calling you today may not be there tomorrow to continue the conversation.

What is CCS Companies?

CCS Companies is a debt collection agency. They have been in business since 1966 and are headquartered in Massachusetts. CCS Companies also does business as Credit Collection Services, CCS Financial Services, CCS Offices, and CCS Payment. They provide debt collection for a wide range of industries including, health care, banking, insurance, telecommunications, utilities, and retail.

Who is CCS Companies? Are They a Scam?

There are actually several different entities that operate under the CCS Companies umbrella that perform different types of collections. The consumer collection arm is called Credit Control Services, Inc., while the commercial collection division is called CCS Commercial. The company also performs medical collections through an entity called ClaimAssist. This means you may see different names associated with the parent company, CCS Companies, depending on the type of debt they're collecting.

A History of Horrors

CCS Companies is a legitimate company that has been in business for nearly six decades. That doesn't mean they're not prone to using heavy-handed tactics, though. In fact, they have such a bad reputation that in just the past three years, the Better Business Bureau has logged nearly 4,000 complaints about CCS Companies. That works out to an average of about 90 complaints per month! Over the past year alone, the BBB closed 1,074 complaints about the company.

There are also over 2,000 complaints about CCS Companies in the Consumer Financial Protection Bureau’s consumer complaint database. Clearly, thousands of consumers have had problems with this debt collection agency.

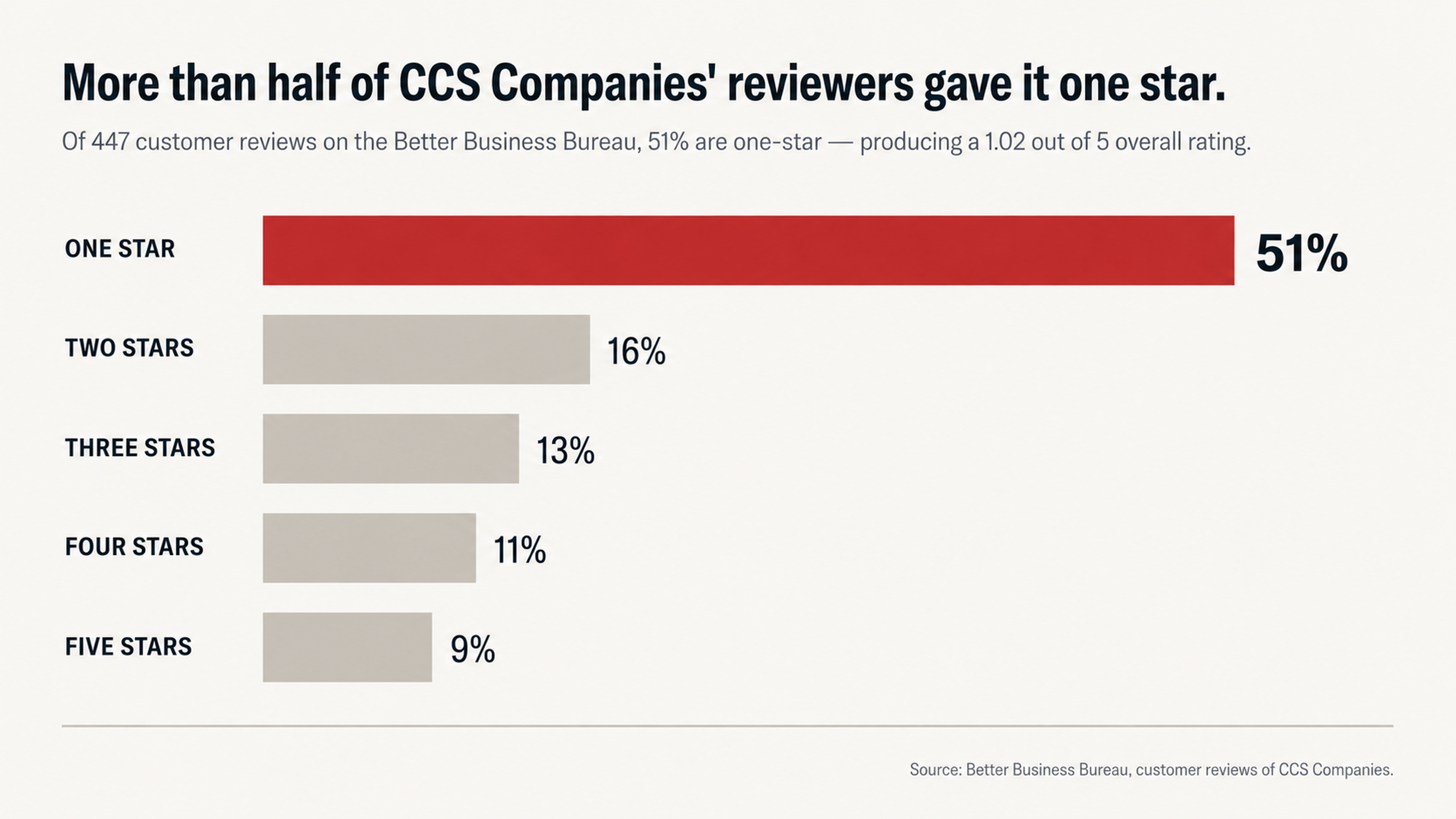

The same trend holds true when it comes to consumer reviews of the company. The Better Business Bureau gives CCS Companies a rating of just 1.02 out of 5 stars, based on 447 customer reviews. Over half of those reviews — 51% — are one-star reviews.

CCS Companies Lack of Documentation

What Information Do Debt Collectors Get?

When CCS Companies purchases debts or accepts assignment of a debt from an original creditor, they're typically given electronic access to information including:

The consumer's name and address

Their Social Security number

The amount they owe

This doesn't mean they have access to the underlying documentation that proves the debt is valid, though. Many times, debt collectors don't get copies of the original contract or agreement that created the debt, nor do they receive detailed payment records. They might not even have the proper documentation to establish the chain of title for the debt.

This isn't a problem that's unique to CCS Companies, either. Instead, it's a common issue in the debt collection industry. When debts are sold, the original creditor might sell thousands of accounts at a time, often for just pennies on the dollar. The debt buyer gets electronic access to basic information about each debt, but they don't receive file folders full of documentation.

Many consumers who have filed complaints about CCS Companies have said the company was unable to provide them with copies of their original agreement or payment records when they requested this information.

In October 2025, a consumer named Troy D. filed a complaint with the Better Business Bureau. He said he received calls from CCS Companies claiming he owed a debt related to his GEICO insurance account. After spending three hours on the phone with GEICO, though, the insurance company couldn't find any records indicating that he owed them money. When Troy asked CCS Companies to provide him with a copy of his agreement and invoices, the company couldn't do so.

Inconsistent Credit Reporting

The lack of documentation in the possession of CCS Companies and other debt collection agencies can lead to inconsistencies in credit reporting.

In December 2025, one consumer filed a complaint with the Better Business Bureau after discovering that CCS Companies was reporting the same debt to the three major credit reporting bureaus inconsistently. According to her complaint, two credit bureaus were showing the debt as closed, while the third was still reporting it as open. "You cannot have an account that is both opened and closed at the same time," she wrote. "This makes the information they are reporting on me inaccurate."

Alexus filed a complaint in June 2025 after an old debt that she had closed two years prior suddenly popped back up on her credit report, causing her credit score to drop. Again, these aren't isolated incidents — they're symptoms of a larger issue with the way debt information is being reported and maintained.

If debt collectors can't even keep their records straight when reporting information to all three credit reporting agencies, that's a sign of a serious problem. Every time you catch an inconsistency in reporting, that's a potential avenue for disputing the debt entirely.

Don't Make This Common Mistake

The Problem with Paying Collections

If you do owe money to a creditor, your first thought might be to simply pay a collection agency and move on. Before you do, though, you should realize that paying a collection isn't a permanent solution. When you pay a collection, you're changing the status of the debt from unpaid to paid, but the derogatory mark will still remain on your credit report for up to seven years. That means lenders will still see that you had a collection account, and paying it might not even improve your credit score very much.

Sadie Uneberg wrote a review of CCS Companies on WalletHub, saying that she paid the amount they claimed she owed, but the account was still showing up as a collection account on her report. She claimed the company was manipulating the date of the account in order to keep it on her report with what seemed like a perpetual six-year history. "This debt collector seems to have no interest other than to cause harm," she wrote.

Collectors know that consumers are eager to get collections off their credit reports, so they might use high-pressure tactics to try to get you to pay without taking the time to investigate whether you actually owe the debt, whether the correct amount is being demanded or whether you have other options.

The Goodwill Gesture That Rarely Works

Why Goodwill Letters Don't Work

Some consumers have tried writing what's known as a goodwill letter to CCS Companies, asking them to voluntarily remove the collection account from their credit report as an act of kindness or because of extenuating circumstances. Unfortunately, that strategy rarely works when you're dealing with a collection agency. CCS Companies bought your debt as a commodity — they're not in the business of doing you any favors.

One consumer filed a complaint with the Better Business Bureau after a representative from CCS Companies told them they would need to pay $88 if they wanted the negative information removed from their credit report. That's a common response from collection agencies.

If you write a goodwill letter or explain your situation to a representative, they're unlikely to respond with sympathy. Instead, they'll treat this as a business transaction — because that's exactly what it is. Don't appeal to their better nature. Understand that you're in a business negotiation where you have more power than you think.

How to Remove a Collection Account

What the Law Says

Under the Fair Credit Reporting Act (FCRA), credit bureaus are required to investigate any information that a consumer disputes within 30 days. The Fair Debt Collection Practices Act (FDCPA) requires debt collectors to verify debts when consumers request this and to stop collection activities until they provide the requested verification.

Here's the thing: Often, debt collectors can't meet those verification requirements when consumers dispute their debts. They might not have access to all of the information they need to prove the debt is valid, thanks to the reasons outlined above — incomplete records, high-volume processing and the documentation gap. If they can't verify the debt within the allotted timeframe, the credit bureau has to delete it.

CCS Companies has been the target of more than 650 federal lawsuits, including multiple class action suits alleging violations of FDCPA. In two of those cases — Schneider v. CCS Companies and Gonzalez v. CCS Companies — the plaintiffs claimed the company was violating FDCPA based on the language it used in collection letters it sent to consumers. That suggests the problems weren't isolated — instead, they were company-wide policies.

In cases where the debt collector is engaging in systemic non-compliance with federal laws, filing a proper dispute can be an especially effective way to get the collection removed.

Put it in Writing

The Danger of Phone Calls

Any time you communicate with a debt collector or credit bureau, put it in writing so there's a paper trail. If you talk to someone on the phone, they might promise you the world — but there's no record of the conversation. By the time you need to follow up, the person you spoke to might be long gone, and their replacement will have no record of your conversation. The debt collection business has notoriously high turnover rates.

In September 2025, a consumer named Katie L. filed a complaint with the Better Business Bureau, saying she didn't find representatives of CCS Companies to be either polite or professional. "I was spoken to in an arrogant and rude manner," she wrote. "I can only assume that bullying type behavior is accepted by CCS."

When you communicate in writing through proper dispute procedures, you create a paper trail, ensure you get responses within the proper amount of time and eliminate the opportunity for the debt collector to make empty verbal promises. You change the conversation from an adversarial confrontation to a bureaucratic process where the letter of the law dictates the response.

When to Call in the Pros

The Emotional Toll of Debt Collection

Hiring a professional credit repair company to help you deal with a debt collector has benefits beyond just knowing what to say and do. The debt collection process is emotional, and that's exactly what collection agencies count on. When consumers get collection notices or calls, they might feel ashamed, anxious or urgent. That impaired emotional state can cloud their judgment and cause them to make decisions they wouldn't otherwise make, such as paying a debt they don't owe or can't afford. Debt collectors are trained to push those emotional buttons and make consumers feel as bad as possible.

If you hire a credit repair company, though, you remove that emotional element entirely. Instead of fielding calls and letters designed to make you feel like the lowest of the low, you have a professional who is acting as a buffer between you and the collector.

Information is a powerful thing. In most collection situations, the debt collector has the upper hand when it comes to information. They know what documentation they have. They know what the legal requirements are. And they know that most consumers will simply pay up rather than fight. When you hire a professional, though, you level the playing field. You now have someone on your side who knows the system and the laws just as well as the debt collector does.

The Power of Ignoring Them

Sometimes the best way to deal with a debt collector is to say nothing at all. Every single time you interact with a debt collector, you're giving them an opportunity to get information from you, confirm your identity or pressure you into admitting you owe a debt. Sometimes ignoring them is the best option.

When you have professional representation, all communication goes through proper legal channels and must be responded to within a certain amount of time. The debt collector can no longer call you multiple times per day. They can no longer contact you at work. They can no longer use harassment as a tactic. Instead, they must follow dispute procedures.

CCS Companies employs 847 people whose job is to process thousands of accounts per month. They're not going to devote a lot of resources to fighting a properly disputed account when they have thousands of other accounts they can pursue that won't be nearly as difficult. The economics of the debt collection business dictate that accounts which are properly disputed and handled within the system are the ones they're least likely to pursue. That works to your advantage if you understand how the system functions.

Conclusion

CCS Companies has been around for 59 years, but that doesn't mean they always get it right or play fair. Nearly 4,000 complaints with the Better Business Bureau, over 650 federal lawsuits and a 1.02-star rating from consumers all tell you there's a problem here. This is a volume business that doesn't always verify the information it's using. In some cases, that might mean they're reporting information that's not yours. In others, it might mean they're pursuing you for a debt you don't owe at all.

Either way, the problem for CCS Companies is that they can't always document the debts they're pursuing. That creates an opening for consumers to file a dispute and have the information removed. A collection account can be removed from your credit report if it's inaccurate, if it's an error, if it's fraudulent or if the collector can't meet verification requirements. That's why the dispute process exists — because the credit reporting system recognizes that collectors often report bad information. So don't be afraid to use it. It's not cheating or gaming the system; it's making the system work the way it's supposed to.

Are you ready to get started?

Contact us today at FightCollections.com for a free consultation. We'll review your credit report and identify any potential inaccuracies or inaccuracies, then talk you through the process of challenging the collection account and getting it removed from your report. You have more power in this situation than you think you do.

Know your rights

The Fair Credit Reporting Act and the Fair Debt Collection Practices Act exist because Congress recognized that consumers need to be protected from inaccurate credit reporting and abusive debt collection practices. Those aren't technicalities or loopholes — they're your rights, and they impose real obligations on debt collectors.

So don't let a collection account from CCS Companies or any other debt collector damage your credit report without challenging it first. The same documentation problems or processing errors that resulted in the error in the first place might also be the key to removing it.