Are you seeing CCS Offices on your credit report? If so, you may have felt a knot in the pit of your stomach, thought of all the consequences this could have on your credit score, or even felt embarrassed enough to close your laptop and pretend you didn't see it.

While it is easy to react that way, know that you're not alone. As a matter of fact, this is exactly what CCS Offices wants you to do. But before we dive into that, let's discuss what CCS Offices is and what they do.

Credit Collection Services, Inc., also known as CCS Offices, is a third-party debt collection agency that operates under The CCS Companies umbrella. Below is some basic information about the company:

CCS Offices collects debts from various original creditors in industries such as healthcare, insurance, telecommunications, and financial services. They also go by the names Credit Collection Services, CCS Collections, and CCS Payment.

What The Public Record On CCS Offices Reveals To Consumers

Before Making Any Decisions On Your Account With CCS Offices, Here's What You Need To Know About The Company's History Of Behavior.

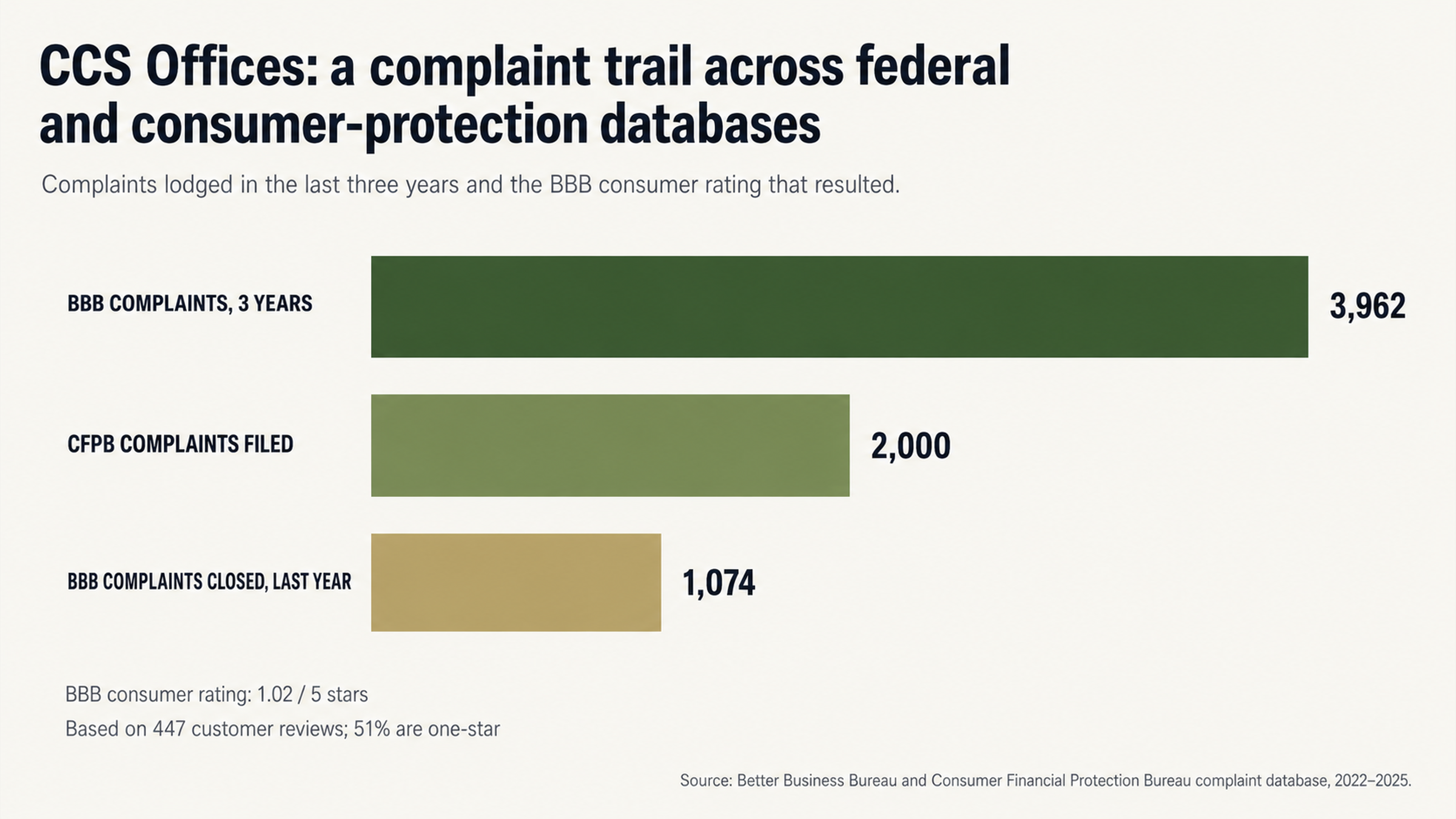

According to the Better Business Bureau (BBB), in the last three years, they've had 3,962 complaints lodged against them, with 1,074 of those complaints closed within the last year. Their rating with the BBB is only 1.02/5 stars.

On the Consumer Financial Protection Bureau complaint database, over 2,000 complaints have been filed against CCS Offices for trying to collect debts from consumers that they didn't actually owe, refusing to verify debts when consumers requested it, and inaccurately reporting information to credit reporting bureaus.

In fact, multiple federal class-action lawsuits have been filed against CCS Offices for violating the Fair Debt Collection Practices Act.

In the case of Schneider v. Credit Collection Services, Inc., the class-action suit alleged that CCS's collection letters were placing additional requirements on consumers to exercise their right to validation.

In the case of Gonzalez v. CCS Credit Collection Services, the class-action suit alleged that CCS was failing to properly disclose information about debts owed, such as whether interest was still being accrued on the debt.

Why You Shouldn't Pay CCS Offices First

With The Pressure To Pay A Collection Account Looming Over You, Here's Why You Shouldn't Pay CCS Offices Before Disputing The Debt.

The minute you see a collection account on your credit report, your initial response is to pay the account off. Who wouldn't want to just make it go away and be done with it? However, this is exactly what CCS Offices is counting on.

The "Payment Paradox" essentially says that when you pay a collection account, you're changing the account status from unpaid to paid, but you're still allowing the negative account to remain on your credit report for the full seven years. Not only that, but you could have just paid a debt that was inaccurate, unverifiable, or even completely fraudulent.

In fact, a study done by the U.S. Public Interest Research Group found that 79% of credit reports contain errors or other major mistakes. This coupled with the fact that thousands of complaints have been filed against CCS Offices for trying to collect debts that aren't owed and refusing to verify debts, it's probably in your best interest to dispute the debt before paying it.

What Information CCS Offices Knows That You Don't

To understand why it's so important to dispute a debt before paying it, you have to understand the information imbalance that's occurring. Debt collectors like CCS Offices have information that you don't have about the account. They have access to records, histories, and resources that consumers just don't have. They understand the system in a way that consumers don't, and they use that system to their advantage by leveraging fear and urgency to get consumers to pay up quickly.

CCS Offices is a pretty large company with about 847 employees and a revenue of $53M per year. They know what they're doing and they have the resources to back it up. If you go into this blindly without knowing your rights and how the law protects you, you're going to end up with the short end of the stick.

Many consumer reviews mention this lack of information and resources. On WalletHub, one consumer wrote, "I called to tell them that they had the wrong person and they said I needed to fill out a form. The account I had with Progressive was paid in full on April 21st. I called CCS and talked with a representative who was unwilling to listen and help me resolve the matter. He told me that I needed to fill out the form even though I had the cancelled check in front of me."

Consumers who try to navigate this process without the proper resources and knowledge of the system end up frustrated and defeated.

Use The Law To Your Advantage

How Debt Verification Works

Before you pay a debt, the Fair Debt Collection Practices Act (FDCPA) says that you have the right to request that the debt collector show proof of the debt they're trying to collect. This means you can require them to verify the amount of the debt, the name of the original creditor, proof that the debt belongs to you, and the date of the last payment. This isn't a "nice-to-have." This is the law.

The burden of proof is on the debt collector, not the consumer. They must prove that the debt is valid, that the consumer is the right person, and that the amount is accurate. If they can't verify the debt, they can't collect on it.

Consumers have filed many complaints against CCS Offices for their failure to verify debts. On December 2025, a consumer filed a complaint with the BBB saying, "I am requesting full validation of this account. I have yet to receive these documents. Generic responses will not suffice as validation."

Another consumer filed a complaint saying, "I received a collection notice from my credit report. However, there was no explanation as to what the charge was for, what business the charge was associated with, or any details regarding the unpaid credit."

Why You Should Dispute The Debt First

The intuitive course of action when dealing with a debt collector is to verify the debt first, then decide what to do with it. However, when you do this, you're giving up your leverage. It's actually better to dispute the debt first, then let the collector prove that the debt is valid.

When you dispute a debt, the debt collector must: Stop reporting the debt to credit bureaus until it's verified, provide documentation that proves the debt is valid and belongs to the consumer, and if they can't verify the debt within a certain amount of time, they must remove the item from the consumer's credit report altogether.

Because CCS Offices has had class-action lawsuits brought against them for their collection letter practices and verification processes, it's better for consumers to dispute debts first. The law is actually on the side of the consumer in these cases, not the debt collector. It's just that consumers don't know that.

The Ugly Truth about CCS Offices Re-aging and Zombie Debt

Perhaps the ugliest truth about CCS Offices is their practice of re-aging accounts. Re-aging is the process of changing dates to make a debt stay on your credit report longer or make an old debt appear newer than it is.

Sadie Uneberg (via WalletHub in June 2024) reports, Paid the agreed-upon debt and now it is a settlement that has been paid but it is still showing as a collection. They keep aging it to keep it on my credit report. It has a perpetual 6-year age. Meanwhile, I am in excellent standing with the original creditor.

Many other consumers report the same experience. One explains, How can they reopen something that has been closed and put it back on your credit? Once it is closed it should stay closed.

Another consumer adds, They keep reopening this account and it has been reported several times. They will not remove it and I keep disputing it.

Inconsistent Reporting to Credit Bureaus

Credit reporting requires consistency. A collection agency must report the same information to each credit bureau. If different information is reported to different bureaus, it might be a sign of an error.

A December 2025 BBB complaint reads, Equifax and Transunion show the account as Open while Experian shows the account as Closed. A single collection account cannot be open on two bureaus and closed on another.

That kind of error is the kind of error that can get an account removed from your credit report.

In a December 2025 complaint, another consumer reports, The account is labeled Installment/Collection Attorney yet there is no original creditor identified, no account number from the original debt, and no documentation.

The Fair Credit Reporting Act requires credit bureaus (and the entities that furnish them with data) to ensure that reported information is accurate. Missing documentation is often a valid reason to dispute a credit reporting error.

Why You Need Help with Disputes

It isn't enough to know your rights under the Fair Credit Reporting Act and the Fair Debt Collection Practices Act. To remove a collections account from your credit report, you need to understand how to dispute the account effectively. That means you need to understand the process, timing, documentation, etc.

Take the experience of these consumers who tried to resolve disputes on their own:

Hours and hours on hold and when I finally spoke to someone, they gave me generic responses that failed to meet FCRA validation standards.

I felt helpless when they would not investigate my identity theft issues.

Credit repair experts know the language to use, documentation required, and process to follow to force a collections agency to respond appropriately. They understand how to identify errors, inconsistencies, and failed verifications and how to use them to your advantage. They also know how to escalate a dispute if the initial response is unsatisfactory.

The difference an expert can make is that they understand how to apply pressure in the right places. They can identify failed verifications, credit reporting errors, and other issues that make it possible to remove a collections account from your credit report.

With a collections agency like CCS Offices that has almost 4,000 complaints at the Better Business Bureau in just three years, almost 2,000 complaints at the Consumer Financial Protection Bureau, and a history of federal lawsuits for its practices, it's especially important to have expert help on your side.

Credit repair specialists work with CCS Offices all the time. They recognize the tactics and responses of the agency and understand how to use the law to force CCS Offices to take appropriate action. They can recognize when the agency fails to verify a debt, inaccurately reports to credit bureaus, and when a collections account can be lawfully removed from your report. And they can force the agency to remove the account.

Perhaps the best benefit of working with a credit repair expert, though, is that it takes the burden off your shoulders. You don't have to feel helpless or frustrated as you deal with a collections agency that doesn't want to cooperate. You have an expert advocate who understands the system and can navigate it on your behalf so that you can focus on other things.

Now Is the Time to Take Action

From Embarrassment to Empowerment

When you have a collection account on your credit report, it's easy to live in embarrassment and shame. You might even be tempted to ignore the letters and phone calls from a collections agency and hope the problem goes away on its own. But ignoring the problem only lets it continue. And the longer you ignore a collections agency, the longer it has to coerce and trick you into doing something that isn't in your best interest.

That changes when you understand the truth about collections agencies like CCS Offices. When you understand that the agency has nearly 4,000 complaints registered at the Better Business Bureau in just three years, that it has been the subject of federal lawsuits, that consumers routinely report problems with documentation and verification, you realize that you don't have to live under the oppression of the agency.

You have the right to remain silent. You don't have to respond to every call and letter. You don't have to explain yourself or justify your situation. And you have the right to representation as you navigate the process of dealing with a collections agency.

Your Next Steps

If you have a credit report that includes a collection account from CCS Offices, you have the right to know whether the account is accurate, whether it is properly documented, and whether it can lawfully remain on your credit report. You have the right to an advocate who understands credit law and debt collection practices. And you have the right to a plan to get your credit report corrected that prioritizes your well-being above the profits of a collections agency.

The team at FightCollections.com is here to help. We specialize in getting results as we dispute collection accounts and demand verification. We understand the process and timing of an effective dispute. We understand how to identify errors, inconsistencies, and documentation errors that support the removal of a credit report error.

Don't wait any longer for CCS Offices to remove a potentially inaccurate (or otherwise invalid) collection account from your credit report. Don't pay a debt that you don't owe or a debt that the agency can't validate. Contact us at FightCollections.com today for a free consultation. We'll evaluate your situation and help you understand your options so that you can make an informed decision about your next steps.