Before we dive into the details, here’s the most important thing to keep in mind: if you see a CCSPayment collection on your report, do not call them.

While this might seem counterintuitive, hear me out. Every time you talk to a debt collector, you risk saying something that will hurt your case.

When it comes to dealing with collection agencies, it’s essential to remember that they know the laws and their limitations much better than you do. That is how they make their money. Every time you say something that helps them, you’re giving them more leverage. You don’t have to do that.

So, what should you do instead? Here’s what we know about CCSPayment and how you might be able to get them off your credit report for good.

Collection agencies like CCSPayment, which has nearly 4,000 documented complaints, prey on consumers’ lack of knowledge and urgency to settle debts. It’s how they stay in business. In the following sections, we’ll take a look at the best strategies for navigating a debt with CCSPayment.

Who is CCSPayment?

CCSPayment is the online payment portal for Credit Collection Services, a debt collection agency based out of Massachusetts. They were established in 1966 and their website, which can be found at ccspayment.com, will redirect you to their self-service payment system.

Credit Control Services, Inc. operates as a subsidiary of The CCS Companies, which also encompasses Credit Collection Services (consumer debt), CCS Commercial (commercial debt), Customer Contact Solutions (call center services), and ClaimAssist (healthcare RCM). The company places over $5 billion in debt from large clients in the banking, insurance, health care and telecommunication industries.

Steven Sands is the President and CEO, Jeffrey Stoddard is the Chief Compliance Officer, and Michael Kraft is the General Counsel. The company employs 847 people and is licensed by the Massachusetts Division of Banks.

A Company with a Bad Rep

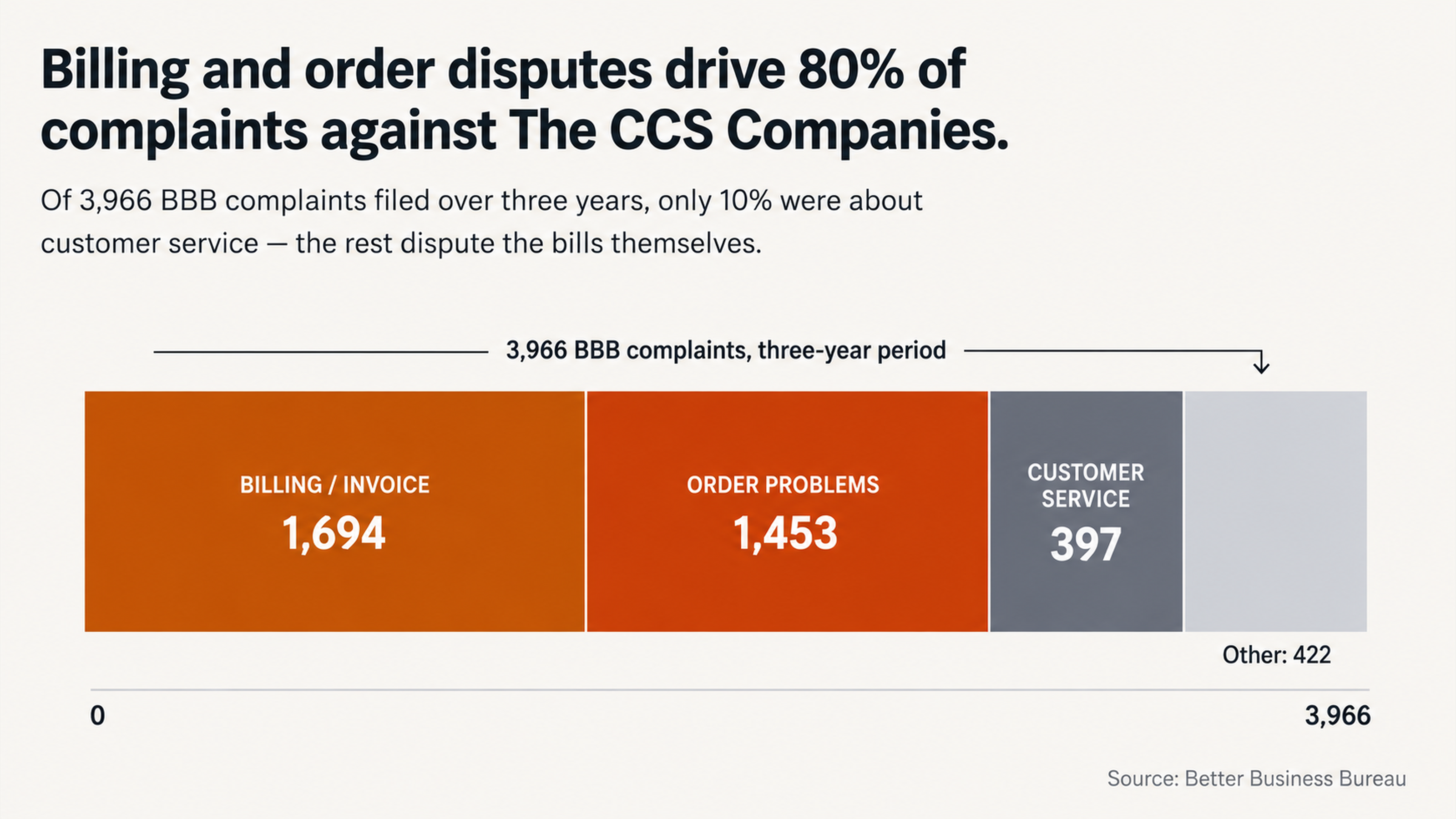

CCS Companies have received 3,966 complaints on the Better Business Bureau website in the past three years alone. That’s almost 90 complaints a month from people who were upset enough to file a formal complaint. Of those complaints: 1,694 complaints were about problems with a bill or invoice (43%). 1,453 complaints were about problems with an order (37%). 397 complaints were about customer service issues (10%). The customer review rating is 1.02 out of 5 stars (the lowest possible rating).

They lost a $2.05M class action lawsuit in Washington State (Michael Stephens v. Omni Insurance Company and Credit Control Services, Inc. and Rajvir Panag v. Farmers Insurance Company of Washington and Credit Control Services, Inc.). The class action resulted in both a settlement payment and a permanent injunction against the company’s collection practices. The class period extended from May 2000 to July 2004, and included Washington State residents who received certain collection letters.

They have not been subject to any federal enforcement actions from the FTC or CFPB as of January 2026. However, this does not necessarily mean they follow the law. Sometimes it just means regulators are not paying as much attention to this company… yet.

Why You Shouldn’t Prioritize CCSPayment

In the event that you pay off a collection account, one of the following will be true: The account will now be marked as paid on your credit report. It will not be deleted. The paid collection will remain on your credit report for approximately 7 years from the original delinquency date.

The Paid Collection Paradox

The paradox of paying off a collection account is simple: Paying it may not help your credit score, and not paying it might not hurt your credit score. When you pay an account the status changes from unpaid to paid, but the entry does not necessarily get removed. A paid collection can still hurt your credit score. This is what collection agencies will not tell you when they’re calling you to ask for money. They want the money. They do not care about your credit score. Once the check clears, they’re done with you. You’re on your own.

In some states, if you make a payment on a collection account it can revive the debt. This means if you make a payment on a time-barred debt, it once again becomes a debt you can be sued for.

79% of credit reports contain errors or inaccuracies. This is according to a study by the U.S. Public Interest Research Group. This means that almost 4 out of every 5 consumers have mistakes on their credit report. Before you pay a collection agency you should at the very least verify that the information is accurate.

The Strategic Value of Ignoring the Creditor

All collection agencies survive based on the same business model. They want as many easy resolutions as possible as fast as possible. The longer you drag something out the more it costs them. For this reason, there is a strategic value in ignoring their attempts at contact. This means that every time you answer the phone you are doing them a favor. Every time you return a call you are doing them a favor. Every time you give them information you are doing them a favor.

When they call you and ask you questions about where you work, or other debts you owe, or how much money you have in the bank, they’re doing it for a reason. They’re doing it because every single piece of information about you that they have is something they can use against you during negotiations. Ignoring them takes away their power.

How CCSPayment’s Business Practices Leave Them Vulnerable

The CCS Companies are a debt collector that has the following complaints registered with the BBB: They attempt to collect debts from consumers who don’t owe them. They fail to provide verification when consumers ask for it.

One customer complaint on the BBB’s website says: “They called saying I owed money from GEICO, after 3 hours on hold with them they could not verify anything I owed. Asked for copies of agreement and invoices and they could not produce anything.”

Another customer complaint says: “They claim I owe Allstate Ins. a monthly payment and just sent me three mailers with different dollar amounts. I just found out through my credit alert today that they reported me for yet another different dollar amount.”

This is not an isolated incident. There are many, many complaints about the same issue. Federal law requires a debt collector to provide you with written verification of a debt if you request it, under the Fair Debt Collection Practices Act. They cannot continue to attempt to collect the debt until they provide verification.

Many customers have also complained about credit reporting errors. One customer review on the WalletHub website says: “They buy debt and then harass you. They never check to see if the debt is valid. They reported on my credit for an account that I never owed a penny to. I disputed and got it removed, but it hurt me for 2 years before I figured out how to dispute it.”

The credit reporting errors can, at a minimum, damage your credit score. At worst, it can cause you to apply for a loan or a credit card with a higher interest rate than you deserve. You may end up paying more for car insurance, a home loan, or an apartment than you have to.

The 30-Day Dispute Window: How It Affects You as a Consumer

When you dispute something on your credit report, the credit bureau has 30 days to respond. This means that they have 30 days to: Investigate your dispute. Determine whether or not your dispute has merit. If your dispute has merit, remove the item you’re disputing from your report.

Many debt collection agencies don’t have the ability to meet this deadline. The business model of most collection agencies relies on volume and speed. They want to place as many phone calls as possible to as many consumers as possible. In their rush to collect as much money as possible as fast as possible, they often don’t have the capacity to properly investigate consumer disputes.

If they can’t verify a debt within the 30-day window, the credit bureau is required to remove the disputed information. It isn’t a guarantee, but it’s a rule. There are certainly instances where credit bureaus will leave items on your report even if they can’t be verified. However, this is not legal. They’re supposed to remove it, and if it happens again in the future you may have grounds for a lawsuit.

This means that you, as a consumer, actually have a structural advantage when it comes to your credit report. If you file a dispute with a credit bureau about an item on your credit report, and the collection agency cannot verify that it’s valid, then it must be removed. This is not a difficult concept to understand. It’s the law.

If you are involved in a dispute with a debt collection agency over the legitimacy of an account they’re reporting on your credit report, you have 30 days for a resolution. If that resolution is not forthcoming, the item will be removed. The agent on the phone with you doesn’t want you to know that. The fact that you know this means that you have a little bit of power in this situation, and that the balance of power is shifting in your direction.

Red Flag Warning Signs of Bad Practices by Debt Collectors

There are several “red flags” you can look out for when determining whether a debt collector is engaging in practices that violate your rights under the FDCPA. If a debt collector does any of the following things, you should be aware of your rights and understand that you may have grounds for a lawsuit:

Asks for immediate payment without validating the debt.

Threatens to sue you or have you arrested when they have no intention of doing so (and do not have the legal authority to do so).

Refuses to give you any information about the debt, such as the original creditor and the amount that you owe.

Uses abusive or profane language.

Continues to call you after you have made a written request for them to stop.

One customer review on the BBB website says: “I do not feel as though collectors are polite or professional. The agent was arrogant and rude; it must be acceptable at CCS to exhibit bullying type behavior.”

Another customer says: “I paid a debt off for this company and never received a letter confirming that my balance was at zero. I have been on hold for nearly 2 hours just trying to talk to somebody to ask them to email a letter stating that I have paid my debt.”

Scams Claiming to be CCSPayment

There are active scams where the scammer claims to be collecting a debt on behalf of CCSPayment. Please note that this is not actually CCSPayment calling, but rather somebody claiming to represent them in an attempt to get you to pay an illegitimate debt.

Cybersecurity companies such as NordVPN, Norton, and ExpressVPN have issued warnings about these kinds of fake CCSPayment communications. Before you communicate with anybody about a debt, you should always verify its legitimacy using contact information you found independently. You should not trust any contact information that they provide you either on a phone call or in an email. Always, always, always verify the information independently.

Disputing the Debt Before Negotiating

Disputing a debt means you do not believe you owe it and want the collection agency to perform an investigation to verify its legitimacy. You should always dispute a debt before negotiating a settlement or payment. Prior to negotiations you should: Obtain a copy of your credit report from each of the three credit bureaus. Compare the disputed account against your personal records. Highlight any discrepancies between amounts, dates, or account information.

Accounts can be removed from your credit report if: Information is not accurate. Information contains errors. Information appears fraudulent. Information cannot be verified within the allotted amount of time. These are not edge cases. Given the frequency of errors on credit reports, this happens all of the time.

A professional credit repair expert will understand how to perform these investigations, what information to request, how to properly phrase a dispute letter, and how to follow up if the creditor does not respond appropriately.

Why Professional Help is Usually Necessary

The debt collection industry is staffed with professionals whose job it is to do this all day. They understand the law. They understand your rights. They understand the urgency and fear with which they are attempting to get you to make a decision. If you attempt to represent yourself in a dispute against a debt collection agency, you are at a disadvantage. You do not have the expertise or resources that they do.

The business model for collection agencies relies on people representing themselves. It relies on people being unfamiliar with the law, their rights, and the tactics that collection agencies use.

Credit repair professionals know that debt collectors use urgency and fear to get you to make a decision without all of the facts. They understand how to slow the process down and ensure everything is done correctly. They know how to ask for records and analyze them for problems. They know how to identify the most likely points of failure for a given debt collection account.

There have been almost 4,000 complaints filed against The CCS Companies in the last three years alone. They are a company that has lost a class action lawsuit and been forced to pay a settlement. They have a customer satisfaction rating of 1.02 out of 5 stars.

It seems clear that this is a company that has no problem operating in a gray area when it comes to your rights as a consumer. If you have a debt that they’re attempting to collect you should understand that this is a company that does not have your best interests at heart. You should take that for what it’s worth.

If you’re attempting to represent yourself in a negotiation with CCSPayment, there are a variety of ways you could put your feet wrong. You could say the wrong thing on a phone call. You could miss a deadline. You could file the wrong paperwork. In many cases this can severely damage your negotiating position. You may end up paying more than you owe, or agreeing to terms that are not favorable to you.

Professionals who handle these negotiations understand what to say, when to say it, and how to say it. They understand what deadlines to meet, and which ones to blow off. They understand what paperwork to file, when to file it, and how to file it.

Professionals who do this for a living understand how to properly navigate the system in a way that gets you the best results for your situation. This is not a guarantee, and there are no promises here. But at the very least the person on the other end of the phone is somebody who actually knows what they’re doing, and is on your side.

Conclusion

If you have a CCSPayment entry on your credit report this is not just a collection account. This is an opportunity for you to flex your consumer muscles and fight back against a company that has almost 4,000 registered complaints against it. This is a company that has already lost one class action lawsuit, and been forced to pay a settlement. This is a company with a customer satisfaction rating of 1.02 out of 5 stars.

When they contact you to ask for money, do not panic. Do not rush to the phone and call them. Do not rush to your checkbook and send them a check.

Instead, you should understand that you have the power in this situation. Information asymmetry is a powerful thing, and it works both ways. They’re relying on you not understanding your rights as a consumer. Once you understand those rights, the balance of power shifts dramatically in your favor.

Take Action Now

Are you dealing with a collection account from CCSPayment? At FightCollections.com, we specialize in fighting collection accounts from CCSPayment and helping consumers just like you to take back control of their finances. Our team of experts uses a dispute-first approach that has already helped thousands of people across the country remove errors, inaccuracies, and unverifiable accounts from their credit reports.

Don’t let CCSPayment push you around and dictate your financial future. Contact us today for a free consultation, and let us show you how our proven system can work for you. Your credit report is a reflection of your financial story — make sure it’s an accurate one.