Seeing Cedars Business Services on your credit report can be a very unpleasant surprise. You may have never heard of them before.

The truth is, though, that you shouldn't rush to pay them or panic. Before calling them or logging into their online payment portal, you should know more about them and understand why your very next step is more important than you realize. They have a real history that you need to understand before taking any action.

Cedars Business Services, LLC, doing business as (DBA) Cedar Financial, is a third-party debt collector. This means that they purchase debts from the original creditor that are past due and then try to collect them from consumers.

License Information: They are NMLS license-holders (#959560 and #964157) and are registered with the California Secretary of State (file #200935010093). Their specialties include domestic and international debt collection, and they even handle European traffic tickets.

What Their History Reveals

It's always wise to check into the history of any business, especially when you're being asked to pay them money. Here's what we found out about Cedar Financial:

Complaints filed with the Consumer Financial Protection Bureau (CFPB): Over 100

2021 CFPB complaints: 53

2021 CFPB complaint ranking: #401 (out of all companies)

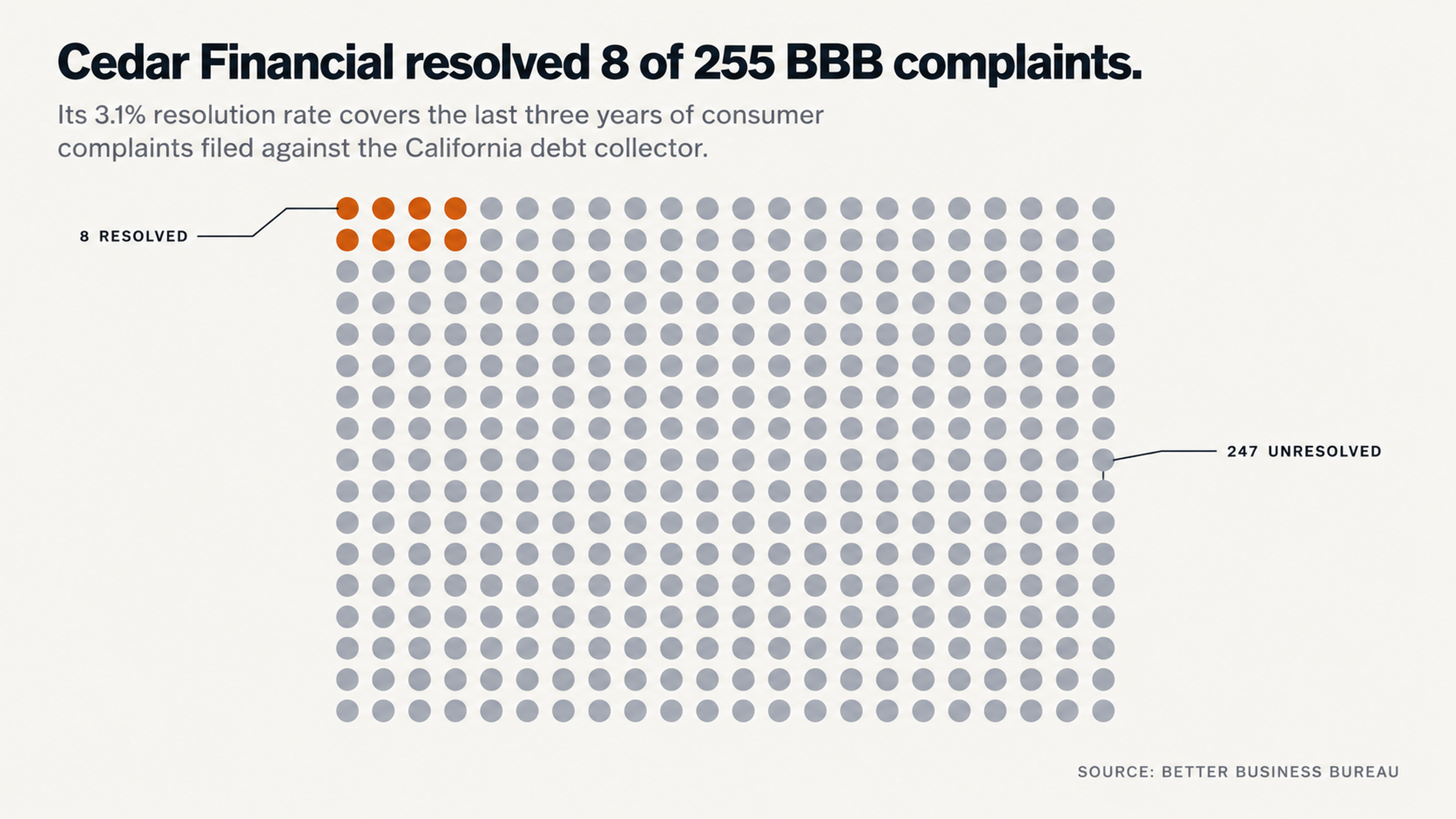

Better Business Bureau (BBB) complaints (in the last 3 years): 255

Better Business Bureau (BBB) complaints resolved: 8

Better Business Bureau (BBB) resolution rate: 3.1%

They became a BBB-accredited business in January of 2023 but still have a dismal resolution rate. While they respond to complaints, they rarely resolve them.

The $800,000 Settlement

What Happened in Chang v. Cedars Business Services

In 2016, a class-action lawsuit was brought against Cedar Financial in Los Angeles Superior Court.

The lawsuit, entitled Chang v. Cedars Business Services LLC (Case No. BC628781), claimed that the debt collection agency recorded outgoing calls to California residents without informing them that the call was being recorded at the beginning of the call. This is against California Penal Code Section 632, which mandates that parties must receive consent from all parties before recording a call.

The lawsuit also alleged that they practiced this from July 2015 to April 2018, almost three years! The court finally gave a final approval of an $800,000 settlement on August 26, 2019. It was estimated that each class member would receive a minimum of $150. Although the company did not admit liability as a part of the settlement agreement, the fact that they paid nearly $1 million is quite telling.

Why Consumers Should Care

This settlement isn't that long ago. It proves a pattern of willful non-compliance that impacted an entire class of California consumers for over two and a half years. When a debt collection agency just paid out nearly a million dollars for illegal practices, that says something about their corporate culture.

The Power of Authority

Humans tend to obey authority figures, especially when under stress. Debt collection agencies are aware of this and use it to their advantage. They want you to feel pressured and confused so that you'll just pay them to make it all go away. However, legally, the burden of proof is on them, not you.

The Problem With Paying

Paying collections doesn't remove them from your credit report. It simply changes the status to "paid collection." It will still remain for seven years from the delinquency date of the original debt.

Debt collectors need you to pay quickly. This is how they make their money. The longer you take to dispute the debt, the less money they make. They aren't prepared to fight for an extended time.

When you're in a state of financial distress, you're much more likely to pay a debt collection agency. They prey on this vulnerability by creating a sense of urgency and fear. They may even suggest that if you don't pay now, they'll sue you or ruin your credit further. Don't fall for their tactics.

Error Rates You Should Not Ignore

Did you know that a study done by U.S. PIRGs discovered that 79% of credit reports contain errors or discrepancies?

This isn't a typo. Almost 80% of all credit reports have some level of inaccuracy. When you pay a debt without first validating it, you're admitting that it's a legitimate debt. You're giving up your rights. You're also giving up the possibility of having it removed. You may be paying a debt that isn't yours at all.

One of the complaints filed against them with the BBB in February of 2025 states, "Cedar Business sent me an email saying I owed them money. I reviewed the case and submitted the dispute with evidence because it is a fraud. But Cedar Business never reviewed the dispute and just asked me to pay once and once again. Very annoying." Unfortunately, this isn't an isolated incident.

Their History of Federal Lawsuits

Over the past decade, there have been at least ten federal lawsuits filed against Cedar Financial for violating the Fair Debt Collection Practices Act (FDCPA) and other consumer protection laws.

The most recent case, He v. Cedars Business Services (Case 3:24-cv-07332, N.D. Cal.), is still active with a filing as recent as January of 2025. Cases have been filed in various states, including Oregon, California, New Jersey, Michigan, and New York.

When there have been that many lawsuits spanning over a decade and across the country, that points to ongoing compliance issues, not one-off mistakes.

Allegations Against Cedar Financial

In the case of Korik v. Cedars Business Services in 2017, the plaintiff claimed that they received numerous autodialer calls asking for someone else even after they informed the debt collector of the mistake.

In CFPB complaint narratives, there are accounts of the debt collector making false threats of lawsuits, continuing to contact consumers after receiving a cease-and-desist letter, and attempting to collect on debts that consumers claim aren't debts they owe.

One CFPB complaint says, "The debt which I do not owe has been sold to Cedars Business Services which makes claims they are going to sue me and if I do not respond collect a lawsuit. The agent on the phone speaks like an attorney but is not. I have told them this is not my debt to please stop calling yet their tactics continue to get more aggressive."

We found multiple complaints on both the CFPB and BBB websites of instances where the company called consumers for months after they received a certified cease communication letter. FDCPA 805(c) states that debt collectors must cease communication upon receipt of a written request to do so. Failure to do so is a violation of the law.

Disputing: A Smart Strategy

Why Does Disputing Work?

When you dispute a collection account, you're invoking your rights under the Fair Credit Reporting Act (FCRA). The credit reporting agencies must investigate your dispute within 30 days. If the debt collector cannot validate the debt, the account must be removed from your report.

Here's the dirty little secret that debt collectors don't want you to know: When debt is sold from agency to agency, documentation sometimes gets lost or becomes incomplete. The original creditor may not have the signed contract anymore. There may be gaps in the chain of ownership. Perhaps the balance due was miscalculated. These documentation issues provide grounds for removal.

Credit repair is a science. It isn't a matter of "luck of the draw." When credit repair experts understand where and what to look for, they can find errors and instances of failure to validate that consumers may not catch on their own.

Why You Need a Professional

The playing field is not level. Debt collectors do this for a living. They understand the laws, the loopholes, and which buttons to push. Most consumers have never dealt with the collections process before and are under duress. They don't understand their rights or their options.

When you work with a credit repair expert, you level the playing field. They understand what documentation to ask for and what questions to ask. They understand which disputes will bring about results. Approaching a debt collector as a DIY project is similar to representing yourself in court against a team of lawyers. You might prevail, but the odds are against you.

Understanding Your Rights

What Does the Law Say?

The FDCPA affords you protection against debt collectors who use abusive practices. Debt collectors may not misrepresent themselves or the debt. They may not threaten action that they do not intend to take. They may not contact you at odd hours or continue to call you after you've sent them a written cease-and-desist letter.

The FCRA mandates that only accurate and verifiable information may be reported on your credit report. If a debt collector cannot prove that you owe a debt, it should not be reported. Period. You can get collections removed if the information is in error, inaccurate, fraudulent, or cannot otherwise be verified within a reasonable amount of time.

The Power of Remaining Silent

One of the strongest tools in your toolkit is silence. You do not have a legal obligation to answer debt collectors' calls. You don't have to explain your situation or negotiate with them. Anything that you say can be construed as validating the debt or reopening the statute of limitations clock.

Don't fall for their urgency tactics. Debt collectors create arbitrary deadlines and make you feel like you need to take immediate action. In most cases, you don't. It usually makes much more sense to take your time and seek the professional help you need.

In Conclusion

Cedar Financial has over 100 complaints registered with the CFPB. They paid an $800,000 settlement because they illegally recorded consumers' phone calls. They've had at least ten federal lawsuits in the past decade for their practices. Their BBB complaint resolution rate is only 3.1%. This isn't a company that you can trust.

If you find them on your credit report, don't panic. Don't pay. And don't try to go this alone. The evidence shows that disputing and working with a professional is the only way to achieve actual removal, not just paying a collection account that will still harm your credit report for several years.

Now What?

It's time to stop giving Cedar Financial the upper hand. First, you need to know what's on your credit report and whether you can challenge it. The experts at FightCollections.com have already helped thousands of people dispute inaccurate collection accounts and restore their credit.

Contact us today for a free consultation. We'll assess your situation, locate potential errors and validation issues, and create a customized dispute strategy that will work for you. You have more power than you realize. We can show you how to wield it.

The debt collectors are hoping you'll remain fearful and in the dark. Let's prove them wrong.