You may be tempted to contact Central Portfolio Control to settle the account. You may think you should file a complaint. You might want to explain the situation to them. Whatever you do, don’t do that without reading this first.

Collection agencies are counting on you panicking and reaching out directly to them. You should never contact them directly. You should never pay a collection agency before consulting with a credit repair expert. According to a landmark U.S. PIRG study, approximately 79 percent of credit reports contain errors or serious mistakes.

Here’s the truth that the debt collection industry doesn’t want you to know: You are not responsible for verifying their debt. The burden of proof is on the debt collector. Central Portfolio Control has to prove that you owe the debt, that they have a right to collect on it, and that the amount is correct. Until they do that, you don’t owe them anything.

Our entire process is designed to give you the information you need to exercise your rights under federal law, and we’ll do it while forcing the debt collector to follow the law as well.

Now, let’s take a closer look at Central Portfolio Control to see how they operate.

Is Central Portfolio Control a Legitimate Company or a Scam?

Central Portfolio Control has been in business for nearly 30 years. While they are a legitimate company, they have had a few run-ins with state and federal regulators.

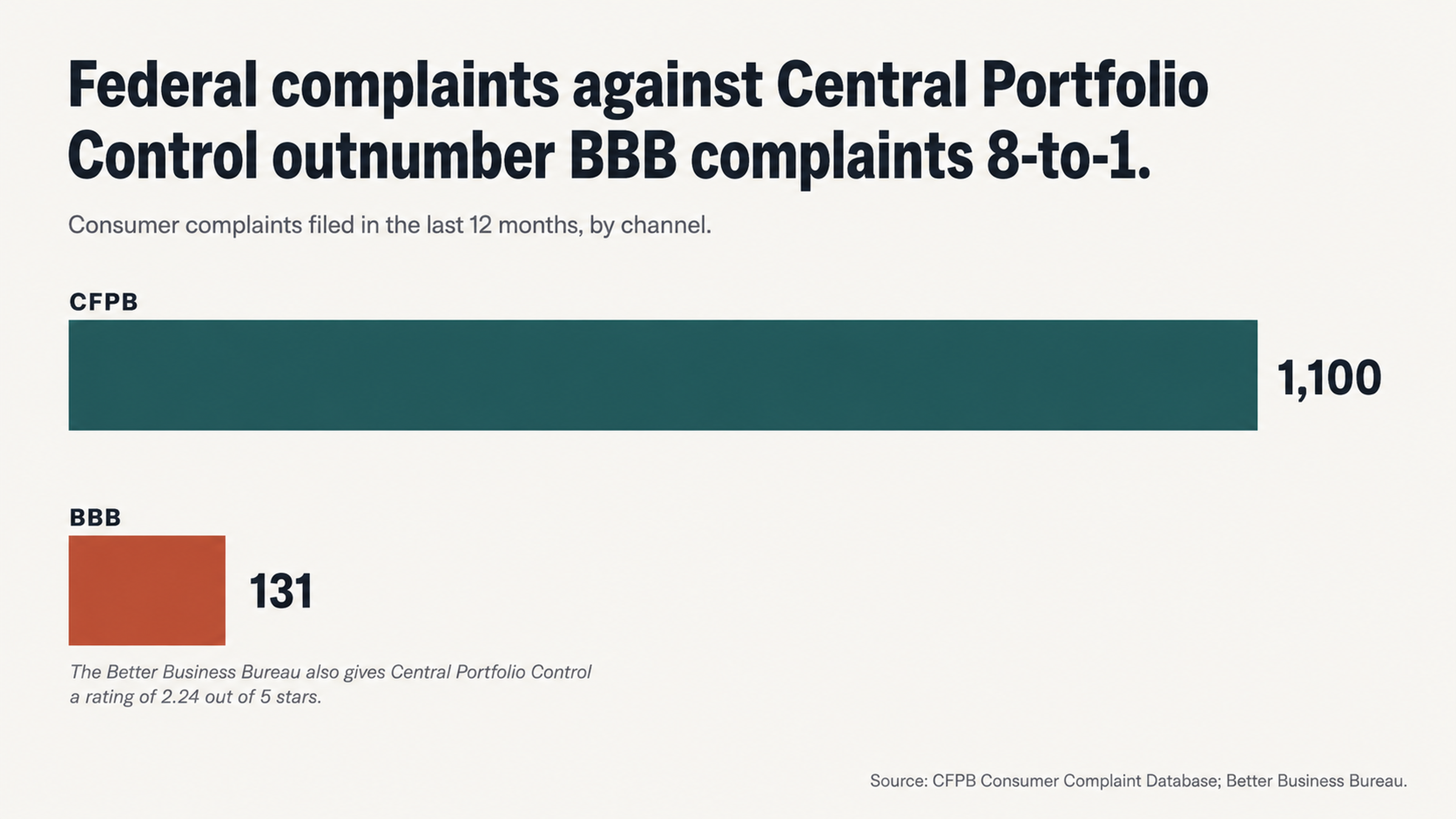

The Consumer Financial Protection Bureau has received over 1,100 complaints about Central Portfolio Control in the last year alone. The Better Business Bureau has received 302 complaints in the last 3 years, with 131 complaints in the last year.

CPC has also faced a few state-level actions. In 2013, the Minnesota Department of Commerce fined CPC $2,000 after they attempted to collect debts from payday lenders that weren’t licensed to operate in the state. In 2017, the Connecticut Department of Banking fined CPC $5,000 after they collected debts in the state without a license for almost 2 years.

According to the PACER database, there have been at least 17 federal lawsuits against Central Portfolio Control in 8 different states. Most of the lawsuits allege violations of the Fair Debt Collection Practices Act (FDCPA). Many of the lawsuits involve harassment through excessive phone calls, failure to send a validation notice, and misrepresentation of the original creditor.

The 2018 class action Norton v. Central Portfolio Control specifically accused the company of misrepresenting creditor information to consumers.

Why You Should Not Pay Central Portfolio Control

If you pay a collection agency, you are settling the debt and bringing the account to a close. That sounds like a great thing, but it’s not. When a collection account is on your credit report, it has already lowered your credit score. Paying the debt just changes the status of the account from “in collection” to “paid collection.”

The biggest problem with paying a collection agency is that it removes your leverage. Once you’ve paid the debt, you can no longer negotiate to have the account removed from your report.

Paying a debt doesn’t remove it from your credit report, and it doesn’t necessarily improve your credit score. If the account is legitimate, paying it may not even help your credit score at all. If the account isn’t legitimate, paying it can actually make it harder to dispute.

The best way to protect yourself is to understand that you don’t have to pay a debt collector to make them go away. Ignoring them, or making them go through the proper procedures, is often the best way to deal with them.

What to Expect When Dealing with Central Portfolio Control

Central Portfolio Control operates like any other debt collection agency. They purchase debts from the original creditors for pennies on the dollar, and then attempt to collect as much as they can from you.

Most collection agencies use an automated system to send collection letters and make phone calls. If they don’t get a response from you, they may escalate their efforts. They may send more letters, make more calls, and even send emails or text messages.

Central Portfolio Control may also attempt to add the debt to your credit report. This can damage your credit score and remain on your report for up to 7 years.

Like most debt collectors, Central Portfolio Control is probably more interested in getting a payment from you than they are in verifying the debt. In fact, Central Portfolio Control has a history of reporting debts to credit bureaus before they’ve even sent a validation letter to the consumer.

One consumer reported to the Better Business Bureau that, “This collection agency has violated federal law by reporting an alleged debt to the credit bureaus without first sending a validation letter. As of 10/11/25, no contact has been made between the collection agency and myself, although their collection account appeared on my credit report as of 10/9/25.”

Another consumer reported that, “They put a collection on my credit report after it was paid off 2 years ago I have proof and the woman said it will not come off till you pay it and would not let me speak with a supervisor. I am in the middle of buying a home and this just might screw up my mortgage.”

Remove Central Portfolio Control From Your Credit Report Today!

If Central Portfolio Control cannot properly document and verify a debt, they have no legal basis to collect it or report it to credit bureaus. However, if you believe that the debt is not legitimate, or if you have already paid it, the best way to deal with Central Portfolio Control is to dispute the account with the 3 major credit reporting agencies. You can do this on your own, or you can work with a credit repair agency that has experience with debt collectors like Central Portfolio Control.

Don’t let Central Portfolio Control or any other debt collector push you around. Contact us today to learn more about your rights and how you can dispute inaccurate debts on your credit report.

Are You Dealing with Central Portfolio Control? We’ve Got Your Back

In the past year alone, the Consumer Financial Protection Bureau has received over 1,100 complaints against Central Portfolio Control. CPC’s Better Business Bureau (BBB) rating is 2.24 out of 5 stars, with 302 complaints in the last three years and 131 complaints in the last year. The BBB has issued a formal alert warning the consumers about instances of misconduct. The company has been subject to two state-level enforcement actions and at least 17 federal lawsuits in eight different states, with most alleging violations of the FDCPA. But it doesn’t have to be that way.

When you contact Central Portfolio Control, you’re playing their game. You are, at best, an annoyance to be handled. At worst, you’re the opening in their next quick score. So why would you give them the satisfaction? Why would you reward their (often) illegal behavior? You shouldn’t.

Instead, contact us. Our team is dedicated to putting you back in control. We’ll help you stand up for your rights and get the outcome you deserve. And if that means you get the chance to smile smugly while some CPC collector’s eyes bug out of their head, so be it.

You don’t have to take on Central Portfolio Control alone. Let us help you get the best possible outcome.