Seeing CMRE Financial Services on your credit report is the last thing you want to see. The feeling of opening up your report and discovering an unfamiliar collection account is the experience of millions of Americans each year.

The embarrassment, the sense of dread, and the immediate desire to avoid dealing with it all at once are all natural reactions to a system that is rigged to leave you feeling disempowered.

But there’s something that the debt collection industry would rather you not know: You have more power than you think. The entire collection business model relies on a system of asymmetrical information. It depends on consumers who do not understand their rights to cough up and pay without questioning the transaction. But once you know who CMRE Financial Services really is and what leverage you really have, the process becomes a lot clearer.

Who is CMRE Financial Services?

CMRE Financial Services, Inc. is a Brea, California-based collection agency that is one of the largest players in the medical debt collection business. They collect for hospitals, physician groups, ambulance and emergency services, and other healthcare systems across the United States. Here are the basics:

A Closer Look at Their Track Record

CMRE Financial Services has racked up over 1,000 complaints registered with the Consumer Financial Protection Bureau, making them one of the most complained about debt collectors in the United States. A March 2016 report by the CFPB noted that the company had seen a 31 percent year-over-year increase in complaints, from an average of 13 complaints per month to 17 complaints per month. The trend has continued since the February 2020 announcement that NexPhase Capital had acquired CMRE parent company Meduit.

CMRE has run afoul of state regulators, who have taken action against the company for failing to obtain a license to operate as a collection agency in their states. The Connecticut Department of Banking issued not one but two consent orders against CMRE for operating without a license, with the second offense in 2018 resulting in a $20,000 civil penalty and $400 in back licensing fees.

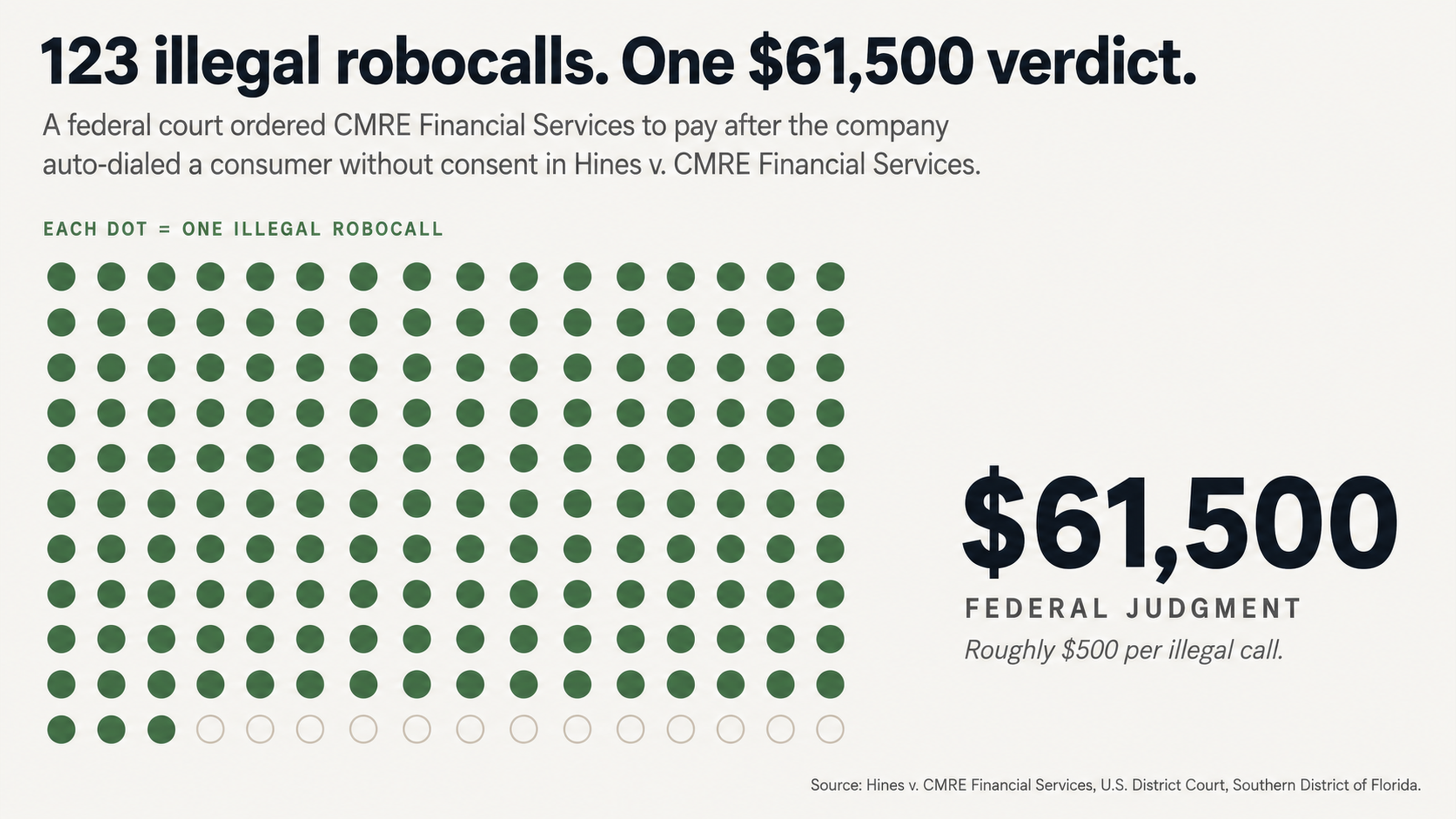

CMRE has also been penalized by federal courts, who have held the company liable for damages when it violates consumers’ rights. In the case Hines v. CMRE Financial Services, the U.S. District Court for the Southern District of Florida awarded the plaintiff $61,500 in damages after it found that CMRE had made 123 illegal robocalls in an effort to collect on a medical debt. The court found that a consent to robocalls that Hines had given to the hospital where she was treated did not extend to the third-party physician group that CMRE was representing, and that CMRE was accordingly not authorized to make the automated calls.

Why You Should Not Rush to Pay

The Payment Paradox

When a collection account shows up on your credit report, your immediate instinct is probably to pay it off as fast as you can. You may assume that once you pay the debt, the negative mark will be removed from your report and your credit score will be restored. But that’s not how it works.

When you pay a collection, it will be noted as a paid collection on your report. But the original debt will still remain for up to seven years. This means that a paid collection can continue to affect your credit score, and raise red flags for new lenders, for years after you have paid off the underlying balance. While some of the newer credit scoring models now treat paid collections more kindly, many lenders still use the older models—and either way, there’s never a good reason to pay a debt without taking the time to evaluate it carefully.

The Error Epidemic

As many as 79 percent of credit reports contain errors or other mistakes, according to a 2020 study by U.S. PIRGs. That’s not just a typographical error, but mistakes like charging the wrong person for a debt, incorrect balances, accounts that should have already been removed from your report, and debts that were already paid (perhaps through insurance or other means).

CMRE Financial Services has a history of these kinds of errors. Consumer reviews describe instances in which CMRE has tried to collect debts from the wrong person, attempted to collect on balances that were already covered by insurance, and has maintained incorrect information about accounts. In a review posted to the WalletHub website, one consumer described being hounded for 14 years over changing balances that the CMRE representative could never accurately itemize. Another reviewer posted a complaint after receiving collection letters about a debt supposedly owed by a nephew who had been deceased for almost a year; after contacting CMRE to inform it of the nephew’s death, the reviewer continued to receive threatening letters for months.

These reviews are just two illustrations of a systemic problem with verification that creates real opportunities for consumers to challenge debts.

Understanding Your Legal Leverage

The Fair Credit Reporting Act

The FCRA is a federal law that creates a number of tools that consumers can use to challenge information on their credit report. If you dispute an item, the credit reporting agency has 30 days to investigate and respond. This creates real leverage, because the clock is ticking—and in many cases, collection agencies cannot provide verification for a debt in time. And if the collector cannot respond within the 30-day window, the credit reporting agency must remove the item in question. That’s not a technicality or a loophole; it’s the law.

Most collection agencies buy debt portfolios, which typically contain thousands of accounts and very little documentation. When they are forced to verify the details of a specific debt owed by a specific consumer, it is often impossible.

The Fair Debt Collection Practices Act

The FDCPA is another federal law that offers important protections for consumers when it comes to debt collection. The law bars harassment, misrepresentation, unfair practices, and other improper communication by debt collectors. Collectors who violate the FDCPA may be subject to statutory damages; pattern-or-practice violations may support a class action claim.

CMRE Financial Services has faced at least six class action claims since February 2020, when the company was acquired by private equity firm NexPhase Capital. Many of those suits allege violations of the FDCPA, and describe practices ranging from misleading language in collection notices to making calls for which the consumer had not given consent to continued attempts to communicate with consumers after they have requested that the collector cease contact.

Each violation represents another point of leverage that consumers may use to their advantage.

Protecting Yourself from Collection Tactics

The Danger of Phone Communication

When debt collectors reach out to consumers, they do so because it puts them in a position of strength. Phone calls create no paper trail, leave lots of room for miscommunication, and allow collectors to use high-pressure psychological tactics in real time. And once you have made a statement on the phone, the collector may use it against you—perhaps by trying to use something you said as grounds for restarting the clock on an old debt, or by claiming that you have waived rights you did not even know you had.

CMRE is available to take your calls seven days a week, between the hours of 6 a.m. and 5 p.m. Pacific Time. That does not mean the company is trying to make things easy for you. Instead, it is simply trying to maximize the chances of catching you off guard, unprepared, and vulnerable to whatever the collector says.

Consumer reviews describe rude customer service representatives, information that changes from one call to the next, and promises that go unfulfilled once the consumer has made a payment. One reviewer who posted to the Better Business Bureau website described calling CMRE to try to get information about a debt, only to be told that she was not authorized to have the information—and then have the representative hang up on her.

That kind of contradictory behavior is par for the course in an industry that depends on keeping consumers in the dark.

The Power of Written Communication

Written communication offers consumers a measure of protection because it creates a record of what was said, who said it, and when. If a debt collector makes a promise or representation in writing, it cannot later claim it did not. And if it makes a misrepresentation in writing, you have grounds for a potential FDCPA claim.

More importantly, written debt validation letters force the collector to show that it has the legal right to collect the debt. That means CMRE must be able to show that the debt is really yours, that the balance is accurate, and that it has been legally authorized to collect the debt on behalf of the original creditor. Many debt portfolios change hands multiple times, which means that collectors may not have access to all of the documentation they need in order to answer these questions. And when they cannot validate a debt, it becomes a lot easier for consumers to successfully dispute and remove it from their credit report.

Never negotiate payment over the phone. Collectors may promise to delete a collection, accept a partial settlement, or agree to stop reporting a debt to the credit bureaus—but once you have made the payment, they may fail to follow through on those commitments. Any agreement should be put in writing before you make a payment.

The Strategic Approach to Removal

Why Disputing Comes First

The best way to approach a CMRE collection is to dispute it, rather than simply paying it off. That does not mean trying to shirk a legitimate debt. Rather, it just means making sure that you are not paying a debt that you do not actually owe, or for an amount that is not actually accurate. Given the frequency of errors in the collection business, and CMRE’s own history of verification problems, that’s not an unreasonable approach.

Disputing a debt triggers the 30-day timeline for investigation and response. The credit bureau must contact the collector and request verification, and if CMRE cannot provide it within the allotted time, the item must be removed from your report. For debts that may have been purchased from a hospital or physician’s group two or three (or ten) years ago, producing an original signed contract and a complete payment history may not be possible.

Why Professional Help Matters

Credit repair is another name for consumer advocacy. Professional credit repair specialists understand the relevant laws and know which records to request, and which pressure points to apply, in order to help consumers maximize their chances for removal. They understand the rules of the game, and the timelines involved, because they have seen it all before. They know how to craft a dispute that a credit bureau cannot ignore, in order to help consumers like you get the best possible outcome.

If you try to navigate the system on your own, you are at the mercy of a bureaucracy that is designed to be as confusing as possible. Collectors are counting on the fact that consumers will get frustrated and give up, or accept incorrect information, or make a mistake that undermines their claim. A professional advocate helps to level the playing field, by bringing some expertise and experience to a battle that might otherwise be one-sided.

The object of the game is not to help people game the system and escape debts they really owe. The object of the game is to make sure that people’s credit reports are accurate, and reflect the true state of their financial affairs. And if CMRE or any other collector cannot meet its burden of proof, removal of the debt is the proper outcome.

Conclusion

Receiving a notice that CMRE Financial Services is on your credit report is not the end of the world. In fact, it is really just the beginning. This is a company with more than 1,000 complaints registered with the CFPB, a company that has been penalized for operating without a license in multiple states, a company that just lost a $61,500 judgment in federal court for making illegal robocalls, and a company that now faces at least six different class action lawsuits. And all of that suggests that CMRE may have a real problem when it comes to verifying its debts and documenting its files.

You may be feeling embarrassed or anxious or stressed about this situation, and that’s understandable. But do not let those feelings drive you to make a decision you will regret. Sometimes, the most powerful thing you can do is to say nothing at all. So do not be afraid to take a little time to get your ducks in a row, and figure out what is really going on here. That is not stalling—that is just playing things smart.

The debt collection business depends on people who are willing to do whatever it takes to avoid conflict or controversy, without taking the time to evaluate their options and make an informed decision. When you refuse to be rushed or pressured into anything, that in itself is a kind of pushback.

Take the Next Step

You do not have to go through any of this by yourself.

At FightCollections.com, we specialize in advocating for consumers who are facing debt collectors and need help disputing inaccurate, erroneous, or unverifiable accounts from their credit report. We understand all of the tactics that companies like CMRE Financial Services use to try to get consumers to pay up, and we know how to challenge those tactics effectively.

So why not reach out to us?

We would be happy to schedule a consultation to review your situation, and talk about whether there may be some inaccuracies that we can use to your advantage. Armed with the right strategy and the right leverage, you can get CMRE Financial Services off of your back and remove this account from your credit report for good. The law offers consumers a number of important protections and powerful tools; we can help you figure out how to use them to your advantage.