Receiving a collection notice from Columbia Debt Recovery can be a daunting experience, but the reality is that you are more in control than the debt collector wants you to think.

By understanding who this company is, what they do, and how they operate, you are better equipped to deal with them and protect your credit score. It has been reported that 79 percent of all credit reports have inaccuracies or major errors. This means that the debt that Columbia Debt Recovery is claiming that you owe may not be accurate, verifiable, or even collectible. Before you start stressing out or writing a check, read on to learn what you are really facing.

Who is Columbia Debt Recovery?

Columbia Debt Recovery, LLC is a debt collection agency located in Washington State that focuses on the collection of property management debt, apartment move-out charges, and utility balances. The company also uses trade names Genesis and Genesis Credit Management.

Below is the basic information you need to know about this agency:

Columbia Debt Recovery currently employs 51-200 employees and operates offices in Everett, Washington; Phoenix, Arizona; and Tijuana, Mexico. The company acquired Columbia Recovery Group, LLC in March 2017.

A History of Bad Behavior

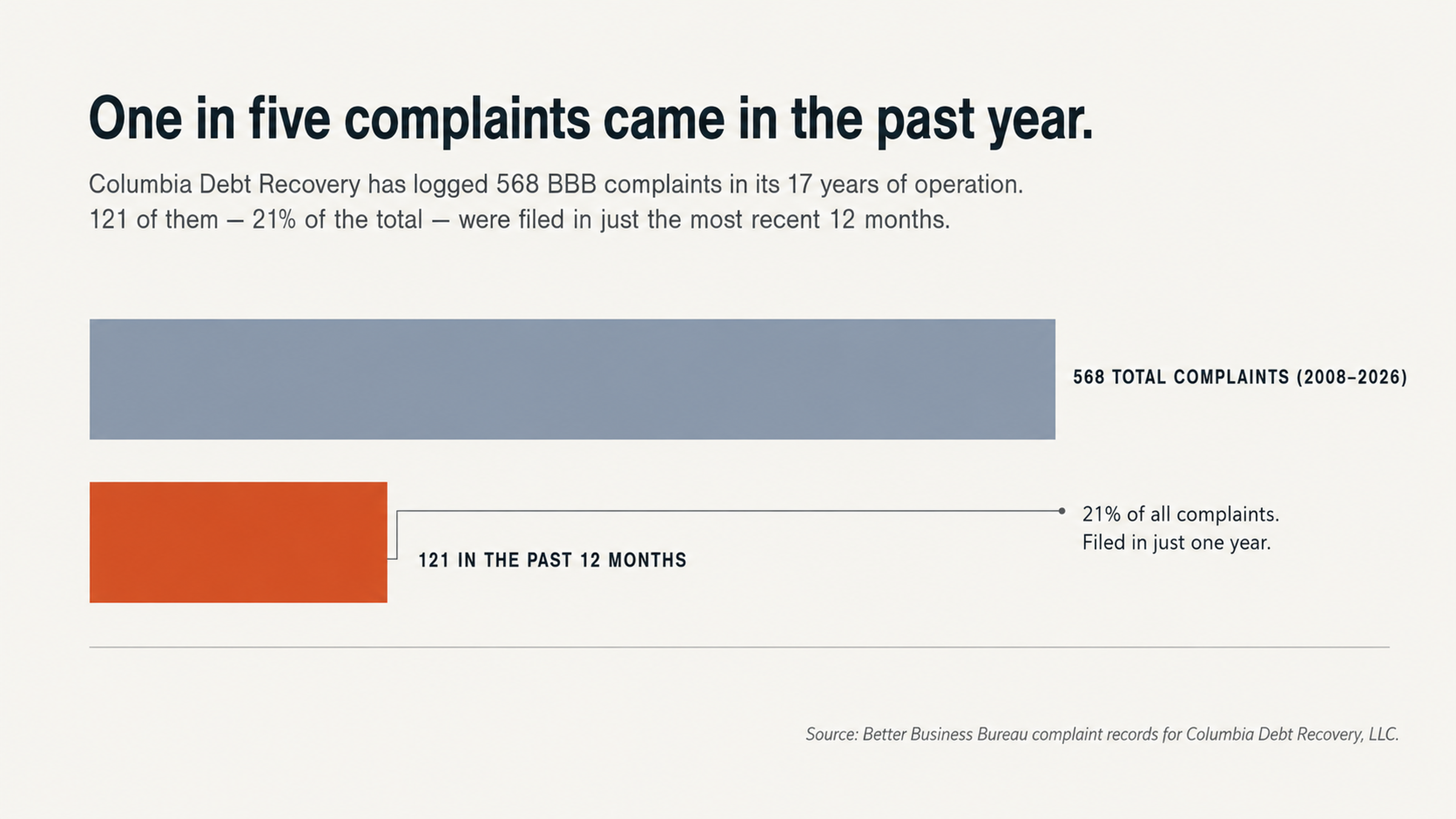

The Better Business Bureau (BBB) has recorded 568 complaints against Columbia Debt Recovery. In the last 12 months alone, 121 complaints have been filed and closed. The company has a B- rating with the BBB and has never been accredited. Their average customer review rating is one out of five stars based on 40 reviews.

Columbia Debt Recovery has also been found guilty of violating the Fair Debt Collection Practices Act (FDCPA) by a federal court. In the case of Johnson v. Columbia Debt Recovery LLC, a judge awarded summary judgment to the plaintiff after the debt collection agency made false representations regarding judgments, wage garnishments, and evictions. The plaintiffs were awarded $30,000 each in emotional distress damages, as well as statutory damages and attorney fees.

In January 2026, the company agreed to pay $200,000 to settle a class action lawsuit that alleged the agency illegally collected interest that was not permitted by either the lease agreement or state law. The settlement for the case McKay v. Columbia Debt Recovery applied to consumers who were contacted by the agency between March 2024 and August 2025 and included the removal of collection accounts from credit reports.

How Columbia Debt Recovery Works

Understanding how this agency works will help you better understand their motives and behavior. Columbia Debt Recovery works as both a contingency collector (on behalf of property management companies) and a debt buyer (purchasing delinquent accounts). Debt buyers pay mere pennies on the dollar for the debt, sometimes as little as 2-5 cents per dollar of face value.

The Debt Buying Business

Bad debt is a commodity in the debt collection business. It is bought and sold like a commodity rather than being treated like a moral obligation that must be paid. When a debt buyer purchases a portfolio of bad debt, they are making an investment. They fully expect and understand that only a small percentage of consumers will actually pay the debt.

When a debt changes hands, it may be sold and resold several times. Each time it is sold or transferred, the documentation may become more and more incomplete. The original creditor may not have provided all documentation, account numbers may have changed, and balances may include fees or interest that were never properly authorized. With each transfer of ownership, the chain of ownership becomes weaker and weaker. This is an important fact to remember when dealing with debt collectors.

Communication and Verification

According to Columbia Debt Recovery’s policies and procedures documentation, the agency reports debts to the credit bureaus twice monthly. They use demand letters, phone calls, skip tracing, and legal collection services to attempt to collect from consumers. The company has been criticized for its aggressive communication.

One BBB reviewer stated, “I have never experienced anything like this in my life. It was nothing short of traumatizing and horrific. The woman was unprofessional, demeaning, condescending, rude, argumentative and behaving in a manner that was extremely threatening.”

Another consumer reported, “When I asked for an itemized bill, she [the representative] threatened to take away the measly 10% discount they were offering.”

Many consumers have complained that the company fails to provide proper debt validation when requested. One user on the MyFICO forum wrote, “They had my name and an amount, but couldn’t prove I actually owed the apartment complex they claimed to represent.”

The Dangers of Paying First

When you first discover a collection account on your credit report, your first instinct may be to pay the debt and make it go away. This can end up being a costly mistake. When you pay a collection account, you are changing the status of the account from unpaid to paid. However, this does not mean the account will be removed from your credit report. The account will remain for seven years from the date of delinquency. When you pay a collection account without first verifying the information is accurate, you may actually be turning a disputed account into one that you have acknowledged.

The Risks of Debt Settlement

When you settle a debt for less than the full balance, it may or may not have a positive effect on your credit score. The outcome depends on a number of factors, including how the debt is reported, whether the original creditor updates their records, and the credit scoring model used. There is no guarantee that settling a debt will help you.

Some agencies report settled accounts as “settled for less than full balance.” This can be viewed as a negative by future lenders. Other agencies may agree to delete the account from your credit report upon payment, but if they don’t follow through on this promise in writing, you have no recourse. The best way to approach debt settlement is to understand all your options first.

Strategic Ignorance is Bliss

Debt collectors want you to think that you need to respond right away. The longer you can wait, the more time you have to research your rights and the more likely you are to discover inaccuracies and flaws in the debt collector’s arguments.

Never speak with a debt collector on the phone. Anything you say can and may be used against you, and phone calls do not create the paper trail that written communication does. Phone calls also allow debt collectors to use high-pressure sales tactics to attempt to coerce you into paying a debt. Written communication does not permit this.

The Multiple Identity Issue

One of the biggest concerns regarding Columbia Debt Recovery is their use of multiple trade names. The agency operates under the names Columbia Debt Recovery, Genesis, and Genesis Credit Management, sometimes all at the same time. This has caused confusion among consumers who are trying to dispute debts and research the company.

Credit Report Manipulation

Some consumers have reported that the agency is manipulating their credit reports. One consumer wrote the following on the BBB website: “Columbia Debt Recovery was reporting on my file, along with Genesis Credit Management for the same debt from March 2017. Thought that was odd so I dispute both in writing. 30 days later Columbia falls off, and then Genesis updates with a January 2022 as account opened.”

The consumer continues, “So I dispute again in writing. Then Genesis disappears and Columbia reappears. It is the same company. They keep playing with this back and forth business changing dates.”

Wrong Person

When an agency like Columbia Debt Recovery pursues the wrong person for a debt, it highlights the importance of verifying the information they are using to collect the debt. Just because they say you owe it does not make it so. The burden of proof is on the debt collector, not you, and they often fail to meet that burden when challenged to do so.

A class action lawsuit was filed against Columbia Debt Recovery in 2024. The suit claimed that the agency pursued an Ohio math teacher for $260 for an apartment she never even applied to live in. The plaintiff claimed to be the victim of identity theft and that the agency was attempting to collect the debt of someone else. The lawsuit also claimed that the agency illegally obtained the consumer’s credit report.

The Importance of Disputing the Debt

The only way to get a Columbia Debt Recovery account removed from your credit report is to systematically dispute the debt and force the agency to prove that it is valid. If they cannot do so, the account must be removed. But, this will not happen if you sit back and wait. You have to make it happen.

Free Credit Reports

Using your free credit reports from each of the three credit bureaus is an essential part of disputing a debt. Not only is it your right as a consumer, but it also provides you with the reconnaissance you need to understand exactly what the debt collector is claiming. Obtain free credit reports from Equifax, Experian, and TransUnion and compare the information that Columbia Debt Recovery or Genesis has reported to each agency.

Compare the information in each credit report for: Inconsistencies in account numbers. Inconsistencies in dates. Inconsistencies in balances. Inconsistencies in the status of the account. Whether the debt is reported by more than one company. Document any information that you cannot verify with your records or that is not accurate. Each of these items is a potential point for disputing the debt.

Disputing the Debt

Under the federal Fair Credit Reporting Act (FCRA), you can dispute collection accounts on your credit report if they contain information that is: Inaccurate. Erroneous. Fraudulent. Cannot be verified within a reasonable period of time.

Columbia Debt Recovery must be able to verify that: You are the correct consumer. The amount is correct. They have the right to collect on the debt. If they cannot verify any one of these items, the account must be removed from your credit report.

In the court case Creager v. Columbia Debt Recovery, the judge ruled that simply accepting documentation from the original creditor was not enough. The agency must maintain procedures reasonably adapted to avoid violations. This means they must verify what they are reporting, not simply pass on what they have been given.

Columbia Debt Recovery Lawsuits & Violations

The Better Business Bureau has recorded 568 complaints against Columbia Debt Recovery. The agency has lost multiple federal lawsuits for violations of the FDCPA. They have paid $200,000 to settle a class action lawsuit for engaging in illegal collection practices. They have a history of aggressive tactics, documentation problems, and issues with credit reports.

This is not a debt collection agency that you want to ignore. But, it is also not an agency that you should fear. Armed with the right information and assistance, you can successfully dispute their claims and have the account removed from your credit report.

Free Consultation

A free consultation with FightCollections.com can help you understand your situation and options before you commit to any action. This risk-free case review will provide you with the information you need to make informed decisions about your credit. You will understand exactly what Columbia Debt Recovery has reported to the credit bureaus, where the weaknesses are in their documentation, and what your options are for having the account removed.

Professional credit repair gets results much more often than consumers who attempt to navigate the process on their own. The system is rigged in favor of those who understand it, and debt collection agencies are counting on you not knowing your rights.

Contact us today to let us put our expertise to work for you. We have extensive experience with successfully dealing with Columbia Debt Recovery.