Credit Collection Services may have appeared on your credit report like an uninvited house guest who made a mess before you even realized they were there.

But if you've already spotted a collection account from Credit Collection Services on your report, don't panic. You have more options than you might think.

In fact, the Consumer Financial Protection Bureau has concluded that 79% of consumers who file complaints about information on their credit reports experience some type of issue. That could mean the collection account from Credit Collection Services shouldn't be there at all, or that it contains an error or two.

Knowing exactly who Credit Collection Services is and what they do can help you navigate the process of getting the account removed.

Credit Collection Services (also known as CCS) is the debt collection arm of The CCS Companies, Inc. CCS works as both a third-party debt collection agency and a debt buyer — which means they might be collecting a debt on behalf of the original lender or they may have purchased the debt from the original lender for pennies on the dollar.

Here's a brief rundown of the company's details:

What They Do

Years in business: 59 (incorporated March 20, 1969)

Alternate business names: CCS Offices; Credit Control Services Inc.; CCSPayment

Mailing address: P.O. Box 7249 Portsmouth, NH 03802

Credit Collection Services primarily focuses on collecting debts associated with insurance accounts — especially debts from GEICO, Progressive, and Allstate. However, they also collect medical debts, utility debts, and other consumer debts, and they're licensed to collect debts in all 50 states.

Credit Collection Services Complaints

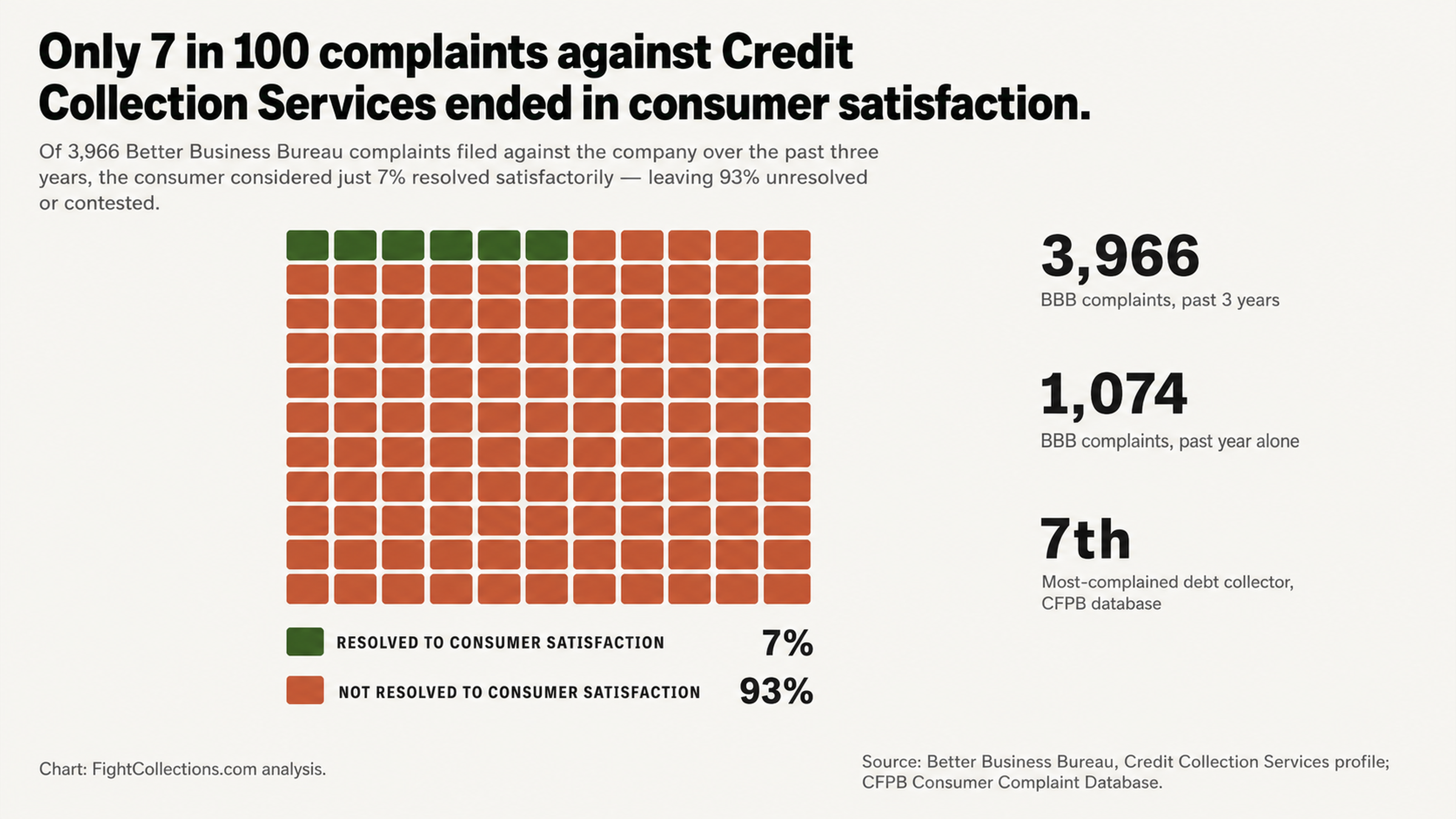

Credit Collection Services has received 3,966 complaints on its Better Business Bureau profile within the past three years, including 1,074 complaints in the past year alone. Only 7% of those complaints were closed in a way that the consumer considered satisfactory.

In May 2023, a judge ruled in the case of Zoltan v. Credit Collection Services that the company violated the Fair Debt Collection Practices Act (FDCPA) by furnishing consumer information to a third-party vendor.

On top of that, Credit Collection Services frequently earns one-star reviews from consumers. One consumer left this review on the Better Business Bureau website: "If I could leave 0 stars, then I would. But this company or whatever this is, is a scam." Another consumer who left a review on WalletHub said: "They buy debt and then harass you. They never check to see if the debt is valid. They reported on my credit for an account that I never owed a penny to."

Why You Shouldn't Pay a Collection Account from Credit Collection Services Without a Fight

If you're getting collection calls and letters from Credit Collection Services, you might feel like you need to pay what you owe as soon as possible to make the problem go away. However, this isn't always the best course of action.

When you pay a collection account, you're updating the status of the account from "unpaid collection" to "paid collection." However, the collection account will still remain on your credit report for up to seven years from the original delinquency date. That means your credit score has likely already taken a hit, and paying the collection isn't going to help your score.

On top of that, when you pay a very old debt, you might inadvertently restart the clock on the statute of limitations — which could leave you open to a potential lawsuit.

Instead of paying the debt right away, it's a good idea to send Credit Collection Services a validation letter and ask them to verify the debt. Legally, collection agencies can't harass you to pay a debt without verifying that it's your debt to pay. Often, collection agencies don't retain all the records and documentation for every single debt they buy, so they might not have everything they need to prove your debt is valid.

In some cases, a collection agency might not have any of the documentation you need to see to verify a debt. They might have only been given a spreadsheet with names, amounts, and contact information when they purchased your debt from the original creditor.

We see this happening in several complaints consumers have filed against Credit Collection Services. In December 2025, one consumer filed this complaint with the Consumer Financial Protection Bureau: "I am formally disputing the accuracy, validity, and completeness of the above-referenced account. I do not have a verified relationship with your company or the original creditor. To date, I have not received these documents. Generic responses do not meet the legal standard for debt validation."

Under the Fair Debt Collection Practices Act (FDCPA), you have the right to request this documentation from a collection agency. The Federal Trade Commission (FTC) requires debt collectors to respond to your request by providing you with validation information for your debt.

If a debt collector can't provide you the validation information you've requested, you might be able to have the credit reporting agencies remove the account from your report altogether. Simply disputing the account can be enough to have the credit reporting agency remove it if the collector can't provide documentation.

3 Steps to Remove a Collection Account from Credit Collection Services

Want to get a collection account from Credit Collection Services removed from your credit report? You can follow these steps:

Step 1: Get Your Credit Report

If you haven't already, get a copy of your credit report from each of the three major credit reporting agencies — Equifax, Experian, and TransUnion. You can access one free credit report from each agency once a year through AnnualCreditReport.com. Make sure you have access to all three reports because collection agencies might report different information to the different agencies.

In fact, reporting information to the credit reporting agencies inconsistently is one of the most common complaints consumers have registered against Credit Collection Services. Here's what one consumer had to say in a complaint filed with the Consumer Financial Protection Bureau in 2019: "The Credit Collections account tied to Progressive is being reported differently on each credit bureau. Equifax and TransUnion show the account as Open while Experian shows the account as Closed. A single collection account cannot be open on two bureaus and closed on another."

As you review your report, make a note of any discrepancies you find. You might find that the agencies are reporting different information for the balance, date opened, date of last activity, status, or creditor, for example. Later on, you can use these discrepancies as reasons to dispute the account.

Step 2: Identify Any Disputable Errors

You can dispute (and potentially remove) a collection account if it contains any errors, isn't your debt, can't be verified, or is too old to be reported. Your goal with this step is to determine which scenario fits your situation.

One consumer registered this complaint against Credit Collection Services in 2018: "CCS Collection Agency is reporting a collection account for $1,016 allegedly owed to GEICO. I do not recognize this debt, did not authorize it and believe it is the result of identity theft. I contacted them to dispute the debt and requested that they delete the collection from all credit bureaus since it does not belong to me. They refused to remove it despite my explanation."

You might be able to dispute the account for errors like:

Debts that belong to someone with a similar name

Debts you already paid to the original creditor

Debts that are past the credit reporting time limit (older than seven years and one month from the original delinquency date)

Debts with an incorrect balance

Debts for accounts you didn't open

If you find any of these errors, you have a reason to dispute the account and ask the credit reporting agency to remove it.

Step 3: Send a Credit Report Dispute Letter

Now that you've identified the errors in your collection account, you can send a dispute letter to the appropriate credit reporting agency. Include your report and account information, a copy of your government-issued photo identification, proof of address (such as a utility statement with your name and address on it), and a clear explanation of the dispute.

You can also use this sample dispute letter as a template to help you get started writing your letter:

[Your Name] [Your Address] [City, State ZIP Code] [Date]

Credit Reporting Agency's Name Credit Reporting Agency's Address City, State ZIP Code

Re: Dispute of collection account from Credit Collection Services

Dear Credit Reporting Agency's Name,

I received a copy of my [Equifax/Experian/TransUnion] credit report and I am writing to dispute a collection account I found on my report. The disputed information is as follows:

Account information: [list the account name and number if you have it], reported by Credit Collection Services.

The specific reason for my dispute is: [list the specific reason for your dispute here and explain it clearly].

I have attached a copy of my driver's license and a utility statement to this letter for identification purposes. Please find the disputed account circled on the attached copy of my credit report.

I would appreciate it if you could provide me with an updated copy of my credit report once you have completed your investigation into this matter.

Thank you for your prompt attention to this dispute.

Sincerely,

[Your Name]

If you aren't comfortable disputing the account on your own or if you have questions about the process, you can consider working with a reputable credit repair company to help guide you through the steps to remove inaccurate information from your credit report.

Now that we have gone through the ways to identify errors in your Credit Collection Services account and how you might communicate with the collector directly, it’s time to decide how to proceed with your dispute. Do you have the time, patience, and legal knowledge to file and follow through on the disputes yourself? Or does engaging professional credit repair make more sense for your situation and lifestyle? It’s an important decision because once you initiate the dispute process with the bureaus, a clock starts ticking, and procedural missteps can jeopardize your removal chances. Understand your options and make an informed choice.

Credit Collection Services Dispute Process

Disputing with the Credit Bureaus

If you decide to dispute Credit Collection Services accounts with the credit bureaus directly, you are invoking a legal process under the Fair Credit Reporting Act (FCRA). This means the bureaus must:

Investigate your dispute within 30 days.

Contact Credit Collection Services (the furnisher) to verify the information they are reporting about you.

Remove the account if the collector cannot verify the debt.

To start this process, you must send your dispute letter to each credit bureau where the account appears, listing the specific errors you’ve found. Do not simply say, “This is not my debt.” While you can certainly dispute the debt’s legitimacy, citing specific inaccuracies in the account information as you’ve found in the steps above gives your dispute stronger legal grounds. Be sure to mention:

The different information across credit bureaus.

The incorrect date.

The wrong amount.

The mistaken identity.

When sending your dispute, use certified mail with return receipt requested to have proof that both you sent the dispute and the bureaus received it. This is important because the bureaus are penalized if they fail to respond to your dispute within the legal time frame.

What If They Respond That It’s Verified?

If the credit bureaus respond that Credit Collection Services has verified the debt, it does not necessarily mean your dispute options are over. You can request how the debt was verified. In many cases, the verification consists of the debt collector confirming the information in their own records, which is not the legal verification required under FCRA. This means you can dispute again, challenging the sufficiency of their verification.

You can also file a complaint with the Consumer Financial Protection Bureau (CFPB) and your state’s attorney general. Sometimes, the pressure from a regulatory complaint can achieve what direct disputes cannot.

Escalating Your Dispute

At this point, many consumers realize the benefits of engaging a professional credit repair service. A credit repair company has:

The knowledge to navigate the dispute process.

The experience to document your dispute thoroughly.

The skill to know how and when to escalate for best results.

The time to dedicate to your case without the distractions of work, family, and life.

Why Hiring a Credit Repair Company Increases Your Chances of Success

The Information Gap The Debt Collector Knows

Credit repair and the legal process surrounding it is their business. They know the rules. They know the loopholes. They know how to make an unsubstantiated claim look legitimate. Consumers dealing with collection accounts typically face this situation once or twice in their lifetime. The collector does it every day. This information disparity puts you at a disadvantage.

Credit Collection Services ranks as the 7th most complained about debt collection company according to the CFPB Complaint Database. Yet, as one industry report observed about the CFPB’s approach to debt collection complaints: “The CFPB has interestingly only really gone after three of these companies, letting the rest of these companies apparently manage to operate scot-free from a regulatory action perspective.”

If you cannot count on regulatory oversight to rein in problematic collection practices, you must advocate for yourself. A credit repair company evens out the information gap. They know how debt collectors operate, the common tactics they use, and how to counter them effectively. It’s their business. What might take you weeks to research and understand is their routine.

An Expert Approach to Credit Repair

At FightCollections.com, we focus on collection accounts that have errors, cannot be verified, or do not meet the legal standards for credit reporting. We understand the patterns of issues seen with debt collectors like Credit Collection Services, including their history of credit reporting errors and verification issues.

Our process includes:

Reviewing your credit report from all three bureaus to identify errors.

Preparing a customized dispute based on the errors found.

Managing the dispute and investigation process.

Following up to ensure the outcome you want.

We handle everything for you so you can get back to your life. We see credit repair as an exercise in consumer advocacy. We believe your credit report should be accurate and that you deserve the best possible credit score.

If you have questions about how we can help or would like a free consultation to discuss your specific situation, please contact us today.

Avoiding Future Issues

Keeping Credit Collection Services Off Your Report

Once you’ve successfully disputed the Credit Collection Services account and had it removed, there’s still a risk it could reappear. Sometimes debt collectors re-report a deleted collection. As one consumer noted in a review on WalletHub: “This inaccuracy had been deleted from all three credit bureaus but then this CCS Collection agency added it back on my credit reports.”

To catch any attempt to re-report your debt, monitor your credit report regularly. Look for any alerts about new accounts or changes to existing ones. The sooner you find the re-reported debt, the sooner you can dispute it again.

Keep detailed records of your original dispute and the deletion of the account. This documentation will be crucial if you need to dispute again. It shows the collector is attempting to report a debt they could not verify when you first disputed it, making your case stronger.

Preventing Future Credit Problems

The next step after cleaning up issues on your current credit report is building positive credit history moving forward. Making on-time payments, keeping credit utilization low, and letting accounts age are all strategies for improving your credit score over time.

Preventing future credit problems becomes your next focus once you’ve resolved the immediate issue of the Credit Collection Services collection. Set up payment reminders to avoid late payments. Communicate with your creditors if you are facing difficulty. Address past-due bills before they go to collections.

However, do not put fixing today’s problems on the backburner while you organize tomorrow’s prevention plan. The negative items on your credit report now are affecting your score now. Let us help you fix them.

A Summary of Removing a Credit Collection Services Account from Your Report

An account from Credit Collection Services on your credit report is an issue but not a judgment. Their history of credit reporting errors, failed verifications, and illegal practices provides a legitimate basis for your dispute. Their 7 percent BBB complaint resolution rate to the consumer’s satisfaction indicates how rarely engaging the company directly results in the outcome you want.

You have more leverage than you realize once you understand the process and your rights. Debt collectors rely on consumers reacting out of emotion rather than information. When you approach the situation from a position of knowledge—knowing your rights, identifying errors, and filing a legitimate dispute—you are taking back control. The burden of proof is not yours but theirs.

Take the First Step Today

Do not allow Credit Collection Services to damage your credit report without verifying the debt. Contact FightCollections.com today for a free consultation to evaluate your situation and determine the best strategy for your removal. Our expertise in challenging questionable collection accounts and advocating for your accurate credit report can make the difference.

Your credit report should accurately reflect your financial history. Let us help you make that a reality.

.webp)