Are you surprised to see a strange collection on your credit report? Is the collector a 60-year-old agency with 300 BBB complaints over three years? If it's Credit Management Company, you are dealing with one of the most prolific debt collectors in the country.

Before you jump to conclusions or your wallet, take a moment to remember that you hold all the power.

This is the first thing to know when a debt collection agency contacts you or appears on your credit report. While a new collection notice can be scary and you may feel the urge to act quickly to take care of the problem, that is the best way to make costly mistakes. The debt collection industry depends on an emotional response from consumers. With such low profit margins per account, agencies like CMC need volume, urgency and fear to stay in business. When you understand their business model, their leverage disappears.

What to Know About Credit Management Company

Before you respond to any collection, you should do your research. If you search for the company name, you will get mixed reviews and you may see different addresses for Credit Management Company. So, what do you need to know?

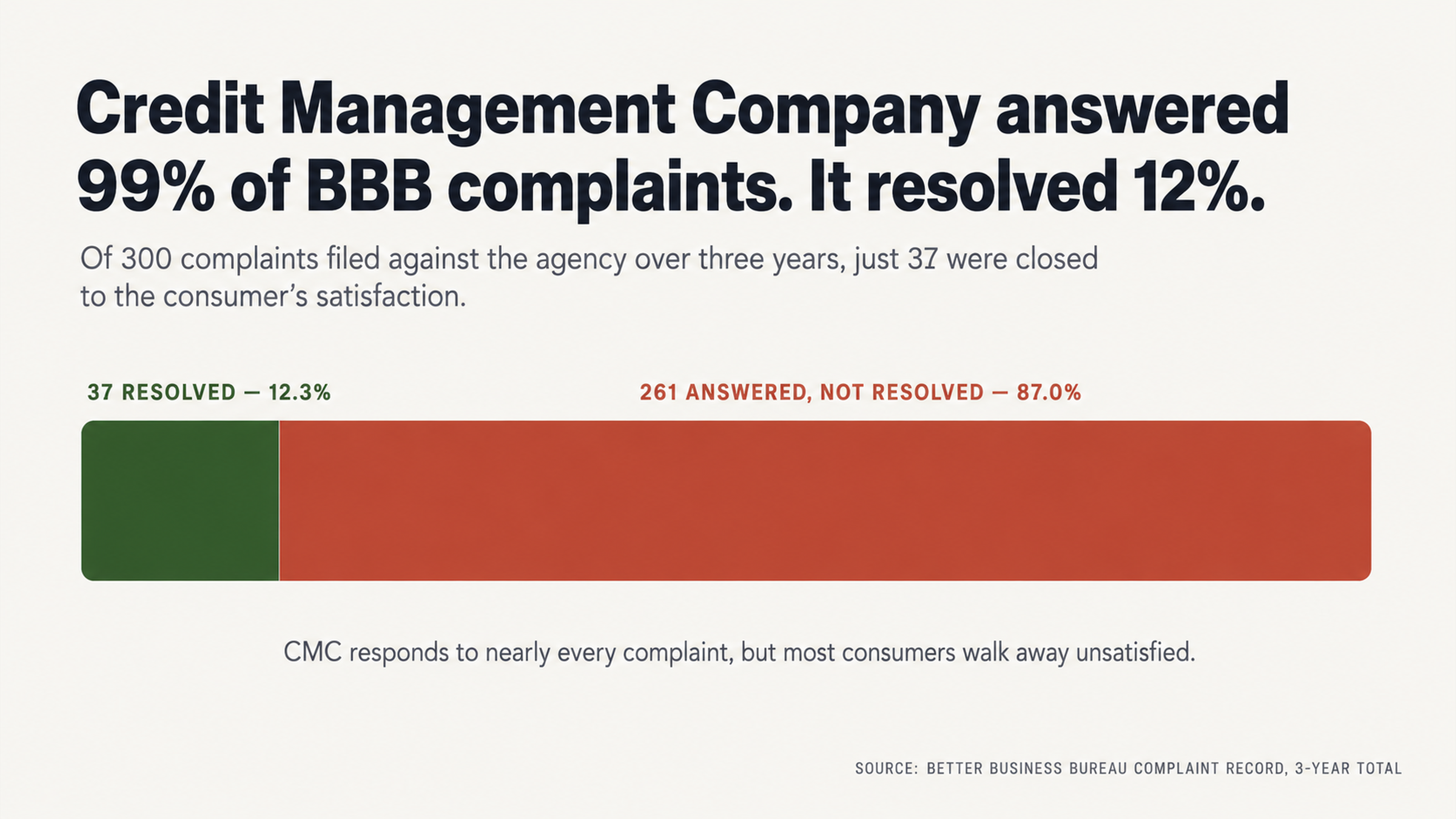

CMC maintains a B+ rating from the Better Business Bureau, rather than the highest A+ rating, specifically because of its complaint volume. Over the last three years, 300 customers registered complaints with the BBB. Of these, 118 came in the last year alone. While CMC responds to 99.3% of its BBB complaints, only 37 were reported closed and resolved to the consumer's satisfaction. That leaves 261 complaints marked answered but not resolved.

If you dig into the federal court data, you will see that CMC faces at least 25 federal lawsuits over the past several years for alleged violations of the Fair Debt Collection Practices Act. Settlements documented on the site include a $4,200 Telephone Consumer Protection Act (TCPA) settlement for a consumer who alleged CMC called him 15 or more times daily with automated messages and a $3,000 FDCPA settlement for a consumer who alleged that CMC sent him fake court papers claiming the agency intended to garnish his wages.

Now you know a little bit more about Credit Management Company. So, how do they work and what does that mean for you?

How Does Credit Management Company Work?

Like all debt collectors, CMC follows a pattern. Once you understand how it operates, you can use that information to your advantage. Predictability gives consumers power. If you know what is coming, you can prepare for the best results.

What Kinds of Debts Does Credit Management Company Collect?

Credit Management Company operates primarily as a third-party debt collector for the healthcare industry. In other words, CMC acts as a middleman for hospitals, doctors and other healthcare providers. In this arrangement, CMC works to collect the past-due account from you.

Many consumers note that Credit Management Company also purchases debt on the secondary market. This means the original creditor has already charged off your account as bad debt and sold it to a debt buyer, usually in bulk. In some cases, the original creditor may have already assigned the debt to another collection agency before CMC bought the portfolio.

In fact, one consumer review from January 2024 states that CMC "purchases 'zombie debts' (over 7 years old) and reports them to the credit bureaus illegally." The same reviewer claims that CMC "preys mostly on senior citizens" and "harasses them to pay to have debts removed from their credit reports."

Whether this review is factual or anecdotal, it points out the problems with debt documentation when it is sold. Anytime debt changes hands, there is a risk that paperwork, including account records, agreements and payment histories, may get lost. This is your opportunity to dispute the debt. Collection agencies cannot collect a debt without verifying the information. If CMC does not have complete documentation for your debt, you may have grounds for dispute.

How Does Credit Management Company Communicate?

BBB complaints paint a clear picture of what to expect from Credit Management Company.

"They call me almost daily, sometimes 2-3 times a day," one complainant wrote. "When I got fed up and told them to stop calling me, they don't listen and still call."

Another documented daily calls, 15 or more, with automated messages before she reached a settlement. Other complaints describe a pattern of refusing to verify the debt. Consumers claim they requested proof of the debt, and CMC ignored them or could not provide the documentation.

"Credit Management Company refuses to send any validation letters for the debt and transfers calls to India when requested," one January 2026 WalletHub reviewer wrote.

"They have never contacted me and the only way I discovered this supposed debt was by pulling my credit report," another added.

These patterns are important. As a consumer, the Fair Debt Collection Practices Act grants you the right to request validation of any debt within 30 days of initial contact. If the collector cannot or will not provide adequate verification, you have grounds to dispute.

Why Paying This Collection Will NOT Help You

It is tempting to simply pay a collection once you see it on your report. In some cases, paying collections can be part of an effective strategy. Before you pay Credit Management Company, understand how it could hurt you.

The Status of the Account Will Change

When you pay a collection, the status will update to paid. This sounds like a positive step, but it does not do anything to help your credit report. A paid collection remains on your report. It does not disappear once you pay the debt. The collection will still be on your report for seven years from the original delinquency date.

In some cases, paying a debt can even restart the clock. If you make a payment on a debt that is several years old, you may unintentionally restart the statute of limitations. In other states, a payment may restart the credit reporting period.

Instead of paying the debt, you may want to try removing it. If there are inaccuracies, verification issues or other problems, you can dispute the account. If it is successfully removed, it will no longer be on your report at all.

What to Expect for Your Credit Score

Consumer reviews offer real-life insight into the damage Credit Management Company can do to your credit score.

In August 2024, one WalletHub reviewer reported that her credit score dropped from 830 to over 710 when CMC reported a medical bill she claims she already paid. "Credit Management Company reported a medical bill to my credit report that I have already paid," she wrote. "I never received a letter or phone call from them. They just reported it."

Another reviewer said her score dropped 70 points in one day.

"Credit Management Company has damaged my credit rating by combining two bills, each under the $500 credit report limit, to make a claim that would damage my credit if I refuse to pay it," one reviewer claimed. "When I refused to provide a credit card over the phone for a so-called 'Manager's Special Discount' the company allegedly reported the debt in retaliation."

In this case, the reviewer said her score dropped 120 points. She also claims the company "primarily targets senior citizens, harassing them for payment to remove debts from their credit reports."

Whether or not these specific allegations are true, they illustrate the potential for score damage. Your credit score is a measure of your financial fitness and trustworthiness. It is how lenders, landlords and employers judge whether you are a good risk. Protecting your credit score is an important part of your overall financial health.

The Power of Disputing Inaccurate Information

The credit reporting system has an inherent flaw that consumers can use to their advantage. Collection agencies must be able to verify the debts they report. In many cases, collectors cannot meet this standard.

Error Rates Work in Your Favor

Studies by U.S. Public Interest Research Groups show that 79% of credit reports contain errors or discrepancies. This is not a misprint. Almost four in five credit reports have errors, ranging from minor mistakes to completely incorrect accounts. The credit reporting system is more broken than most consumers understand.

In the case of Credit Management Company, BBB complaints suggest it is part of the problem. Over three years, 260 of the company's 300 BBB complaints (or 86.7%) involve billing and collections disputes. Consumers repeatedly claim that CMC attempts to collect for debts paid by insurance, for services not provided or debts owed by someone else entirely.

These are not just customer service complaints but potential grounds for removal. Federal law offers a process for challenging these errors. When you dispute information with the credit bureaus, the creditor must verify the information and respond within a reasonable amount of time. If it cannot provide documentation, the credit bureau must delete the disputed item.

Gaps in Documentation Offer Opportunity

Debt collection is a paperwork business. When original creditors sell or assign debts to collection agencies, the paperwork does not always follow. Each time debt is sold or transferred, it is easier for paperwork to disappear. By the time a company like CMC attempts to collect, it may not have the original agreement, a complete payment history or proof that you are even the right person.

Again, BBB complaints suggest a pattern. "CMC failed to verify the debt," one reviewer claimed before the company damaged his credit. Another said, "Dates and details were not reported accurately."

These documentation gaps are not an accident. The debt-buying industry operates on volume and razor-thin margins. Keeping paperwork on every single account in a portfolio of millions is costly. Many collectors do not bother and simply hope consumers will not challenge them.

Taking Control of Your Credit Report

Information is power. Once you understand your rights and the weaknesses of the collection agencies, you can approach the process without fear.

Why You Need a Professional

The debt collection industry works because of information inequality. Collectors understand the laws, loopholes and tactics to coerce consumers into paying questionable debts. Most consumers do not have this information and enter the conversation at a disadvantage.

Credit repair is consumer advocacy. It levels the playing field by pitting collectors against professionals who understand how to challenge and dispute inaccurate, unverifiable or incorrectly reported information.

The 25 federal lawsuits against Credit Management Company show that consumers can successfully challenge the agency's practices. Consumers simply need to know where to look and what to ask for.

Many consumers who try to navigate this process on their own end up making costly mistakes. Saying the wrong thing to a collector, resetting a clock or accepting a settlement that still leaves a negative mark on your credit report are common missteps. Working with a professional helps you sidestep these landmines on your way to the best outcome.

Reclaiming Financial Independence

This is not just about getting a collection removed from your report. This is about reclaiming your financial independence and refusing to be pushed around by companies that make money on your fear and confusion. Once you recognize that debt is a commodity, not a moral obligation, the rules change.

In fact, CMC's response to complaints offers a clue. The company answers with a form response stating that it "takes all complaints very seriously" and has "performed a thorough investigation." Despite this response, 87.7% of complainants report an unsatisfying experience. The company is checking a box without actually resolving the problem.

You deserve better than a form letter and an unverified debt hurting your creditworthiness. As you address this immediate issue, you can also learn how to avoid future collection problems, but first, you must deal with what is already on your report.

Conclusion

Credit Management Company may have 60 years of experience, but that does not mean the debts it reports are valid. With 300 BBB complaints over three years, a 12.3% resolution rate, 25 federal lawsuits and a 1.2-star rating, the company has a lot to answer for.

The collection on your report may be inaccurate, unverifiable or misreported. You have the legal right to demand proof and dispute anything that cannot be verified.

What's Your Next Step?

Do not let Credit Management Company coerce you into a decision that could leave the collection on your report even longer. Instead, take the smart step.

At FightCollections.com, we specialize in fighting debt collectors by disputing incorrect information on your credit report and holding collection agencies to the letter of the law. Our team understands how companies like CMC operate, where the documentation gaps are and how to challenge accounts that fail verification. We advocate for consumers who will not be intimidated into allowing unverified debts to destroy their financial futures.

Contact us today for a consultation. Let us evaluate your situation and identify the best course of action to get Credit Management Company off your credit report. You have rights. It's time to use them.