If you're finding a collection account on your credit report that you don't recognize, it can be alarming. Especially if the collection agency is completely unknown to you.

DCM Services, LLC is a debt collection agency that is a little different. They specialize in the rather sensitive area of debt collection: collecting debts from the estates of the deceased.

If DCM Services is on your credit report, it's essential that you know who they are and what they do.

Here is the basic information on DCM Services:

Years in Business: 19 (Incorporated August 2006, successor to Balogh Becker, Ltd. founded 1998-1999)

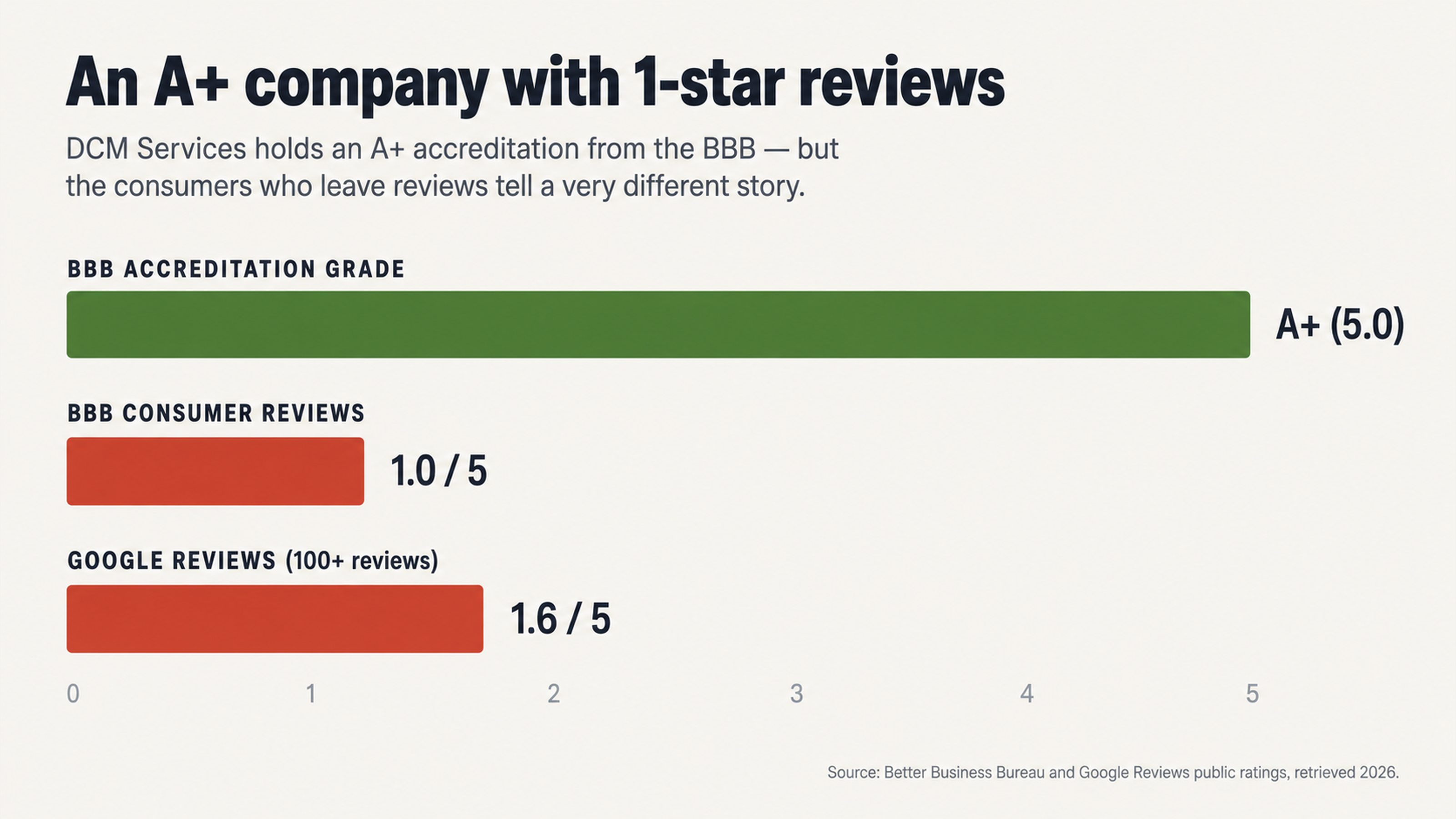

BBB Rating: A+ (Accredited since December 2007)

Despite A+ Rating, DCM Services has a Checkered History

Though DCM Services has an A+ rating with the Better Business Bureau, the reality told by consumer reviews is different. The average rating for DCM Services on the BBB website is only 1-star out of 5. On Google Reviews, DCM Services averages 1.6 out of 5 stars, with over 100 reviews. This huge disparity between the overall rating and individual reviews says a lot about how credit reporting and collection agencies are rated.

In 2010, the Federal Trade Commission launched an investigation into DCM Services for possible violations of the Fair Debt Collection Practices Act. The investigation was to determine if DCM Services was making false representations to family members of the deceased that they were personally responsible for the debts. Though the FTC decided not to recommend enforcement, they were clear that the decision should not be construed as a determination that no violation occurred.

There have been several federal lawsuits filed against DCM Services for violations of the FDCPA. Court records show cases like Machnik v. DCM Services in 2017. The plaintiff, a widow, alleged that DCM Services unlawfully attempted to collect her late husband's medical debts from her. In 2021, another consumer credit lawsuit was filed against DCM Services. Hirschman v. DCM Services included a demand for a jury trial. It seems there may be a history here rather than a few isolated incidents.

Most recently, in March 2025, DCM Services was acquired by the private equity firms Aldaron Partners and True Wind Capital. This is just the latest change in ownership for DCM Services, which can make it difficult for consumers to determine which company is responsible for past transgressions. The previous owner, NMS Capital, purchased DCM Services from Norwest Equity Partners. Private equity groups regularly buy, sell, and trade debt collection agencies, which can make it tough for consumers to sort out who's on first.

How Do Collection Accounts Affect Your Credit?

The Psychology Behind the Credit System

The credit reporting system works on a basic premise that consumers may not recognize: it's designed to reward those who know how the system works. When you see a collection account pop up on your credit report, the negative impact is immediate. And it doesn't matter whether or not you actually owe the debt.

This information disparity is how collection agencies make their money every day. Collectors need consumers to feel intimidated and overwhelmed. They know that most consumers will pay a debt without asking too many questions, especially if they're getting official-looking letters in the mail and fielding authoritative phone calls.

Humans have a natural tendency to defer to authority. And debt collectors know how to project authority, even when they have no legal basis for their claims. The debt collection business model relies entirely on expediency. Every single day that a debt is in dispute is costing the collector money. Every time they need to respond to a verification request, it's costing them money. Once consumers understand this, the balance of power begins to shift.

Why Paying a Collection Account Often Makes Things Worse

There's something that collection agencies will never tell you: paying a collection account does not get it removed from your credit report. Instead, the status of the account simply changes from "unpaid collection" to "paid collection." But the account remains. And it will continue to damage your credit for the full seven years. Paying a collection account does nothing to improve your credit score. So reaching for your wallet should never be your first move when you get a collection notice.

The seven-year clock for credit reporting started when the original account went delinquent, not when the collector reported it. Paying the debt does nothing to reset that clock. The derogatory mark on your credit report remains right where it was. And every lender who pulls your credit report will see it. Your better move is to understand what collectors actually have to prove before they can collect or report a debt. Many times, they can't meet that burden when properly challenged.

Think about it from a purely economic standpoint. Debt collectors buy debts for pennies on the dollar and hope to collect a fraction of the face value. Their profit model depends on volume and speed. The more accounts they have to do extensive verification work on, the less money they make. The more they have to fight with consumers, the more money they lose.

Understanding the Documentation Issue with Debt Collectors

Your Right to Verification

Under the Fair Debt Collection Practices Act, consumers have the right to request verification of any debt that a collector claims they owe. That means the collector must provide proof of the debt, including the amount, the original creditor, and when the last payment was made. These aren't just "nice to haves." They're the law.

DCM Services has a history of problems with documentation. On the BBB website, a reviewer left a complaint in September 2025. The consumer received a letter from DCM Services claiming that they were deceased and asking who was responsible for their estate. The reviewer said, "I am not dead I do not appreciate this letter. I want others to know or be aware I believe this could be a new scam!" That suggests a pretty glaring problem with documentation.

Another complaint on the BBB website from August 2024 claimed that DCM Services resubmitted bills for payment that had already been made. In fact, the consumer said DCM Services had cashed three checks for the same hospital bill two weeks earlier. If collectors can't even keep track of which bills have been paid, can we trust them to accurately determine the correct balance?

The Documentation Gap

Debt collectors often buy accounts from the original creditors with very little documentation. They may purchase thousands of accounts at a time with nothing more than a spreadsheet listing names, balances, and contact information. They may never even receive the original documentation on the accounts.

That creates an opportunity for knowledgeable consumers. If a debt collector cannot provide documentation proving that you owe a specific balance to a specific original creditor, they have only two options. They can either remove the account from your credit report or continue reporting information they cannot verify. The latter opens them up to legal liability.

We know that credit reports are frequently wrong. In fact, a study by U.S. PIRGs indicated that 79% of credit reports contain errors or major inaccuracies. When you combine the inherently error-prone credit reporting system with the lack of documentation in the collection industry, the likelihood that any given collection account is both accurate and verifiable is lower than many consumers might think.

The burden of proof is key here. When a debt collector is reporting information to the credit reporting agencies, they are also responsible for ensuring that the information is accurate. When they cannot verify the information they are reporting, the question arises as to whether the account should be on your credit report at all. By disputing the account, you are forcing the collector to either verify the account information or remove it from your report entirely.

Why the Complaints Against DCM Services all Sound the Same

Targeting the Bereaved

DCM Services makes all of its money collecting debts from the estates of deceased individuals. That's a recipe for disaster, as consumer complaints bear out. Because DCM Services regularly contacts the grieving families of deceased individuals, there's a high likelihood of contacting them before they even understand their responsibilities.

In May 2025, a consumer left a complaint on the BBB website. The reviewer said, "Watch out for these people if your loved one has passed away. They will try to collect on hospital bills that have already been paid. In fact, they started bothering us before we even got the bill. These people are monsters that prey on grieving families."

Another reviewer on the BBB website complained in August 2024. The consumer said that DCM Services called about a bill before the body was even cold. In fact, the bill in question was one that should have been paid by the VA because the consumer's father was a disabled Vietnam veteran. The consumer claimed that the representative from DCM Services actually became hostile. The family was forced to spend an entire day on the phone to get the debt dismissed.

Creating a (False) Sense of Urgency

One federal class-action lawsuit claimed that DCM Services regularly sends consumers correspondence with "time sensitive" settlement offers that are entirely false. There's a good psychological reason why debt collectors would do that.

Humans have a tendency to respond to deadlines. When someone is calling you, claiming you owe a debt and implying there will be consequences if you don't pay immediately, the human response is to react without taking time to think. That's exactly what the debt collectors want. They want you to react before you think. Pay before you verify. Don't bother to analyze their claims and make sure they're right. Just pay.

Strategic non-response can be a powerful thing when dealing with debt collectors. When you refuse to engage on their timeline, you're taking away a lot of their leverage.

The Dispute-First Strategy for Dealing with Collection Accounts

Why You Should Always Start with a Verification Request

Instead of just paying a collection account that may or may not be valid, your first step should always be to dispute the account and request verification. If there is information on your credit report that is inaccurate, erroneous, fraudulent, or cannot be verified within a reasonable amount of time, you can have it removed.

The key is understanding what, exactly, constitutes "verification." The collector cannot simply send you a printout that says you owe the balance they're claiming. They need to be able to provide documentation that proves you owe that balance to that creditor. And they have to be able to prove they have the legal right to collect it.

Given the widespread documentation problems in the debt collection industry, many accounts cannot survive a legitimate challenge. The collector's incentive is to just move on to the next account rather than engaging in a long, drawn-out battle over verification. That costs them money.

Dealing with a Collection Account from DCM Services

When DCM Services puts a collection account on your credit report, your first instinct may be to pick up the phone or start responding to their letters. Don't do that. When you engage with a debt collector on their terms, you're putting yourself at a disadvantage. They're professionals. You're not.

Instead, you may want to consider working with professionals who understand the mechanics of the credit reporting system and the documentation vulnerabilities of collection agencies. Credit repair specialists work with these companies every day. They know which documentation requests have the best chance of exposing a collector's verification failures. And they know the timelines and procedures that will put the most pressure on the collector to verify the debt or vacate it.

If you try to handle a collection account on your own, you're facing off against the collector's team of specialists while trying to interpret complex federal regulations. The information disparity rarely works in the consumer's favor here.

The Bottom Line

Don't Let DCM Services Damage Your Credit

DCM Services has racked up a lot of consumer complaints, been the subject of a federal investigation, and been a defendant in several federal lawsuits despite their A+ accreditation and rating. The disparity between their official ratings and their individual consumer reviews says a lot about how the system is working.

Just because DCM Services has placed a collection account on your credit report, that doesn't mean you have to just accept their claims and let them damage your credit. You have legal rights to verification. You have options besides just paying the debt and hoping the credit damage will eventually fade. And you have access to professionals who specialize in challenging questionable collection accounts.

The credit reporting system is designed to reward people who understand how it works. Collectors make their money off consumers who are confused and intimidated. They profit when consumers are urgent and fearful. But when consumers have knowledge, patience, and professional guidance, the system works a lot differently.

Remember, a collection account on your credit report isn't proof that you owe the debt or that the amount is accurate. It just means someone has reported that information to the credit bureaus. Whether the information is accurate and verifiable is a completely different story. And it's a story that you have the power to change.

Next Step

If you're facing a collection account from DCM Services, don't let them continue to damage your credit without a fight. At FightCollections.com, we help consumers challenge questionable collection accounts and demand the verification that collectors many times cannot provide. Our specialists understand the documentation requirements, the legal technicalities, and the timeline technicalities that determine whether a collection account can legally remain on your credit report.

Don't pay DCM Services for a debt you may or may not owe without exploring your options first. Contact FightCollections.com today for a free consultation. Let us help you understand your rights and develop a customized plan to meet your needs. The first step toward better credit is recognizing that you don't have to face the collectors alone.