Imagine seeing an unexpected collection on your credit report. That’s bad enough, but what if the collection is on your report from Diversified Adjustment Service, one of the most sued debt collection agencies in the US?

This article is a comprehensive guide on how to dispute and remove a Diversified Adjustment Service collection from your credit report.

In a study by U.S. PIRGs, 79% of credit reports contained errors or disputes. This alone should make you skeptical of a collection account on your credit report. The information that debt collection agencies report is often flawed, and you have legal recourse.

Who is Diversified Adjustment Service?

Diversified Adjustment Service, Inc. is a third-party debt collection agency based in Minnesota. Here’s an overview of their basic information:

The company is family-owned, wholly owned and operated by its founder, Kathleen J. Zurek, who serves as the CEO of the company. DAS is licensed to collect debts in 45 states as well as Puerto Rico and primarily collects for telecommunications providers, utilities, and healthcare services.

Despite its longevity, DAS has an alarming regulatory and legal history, including:

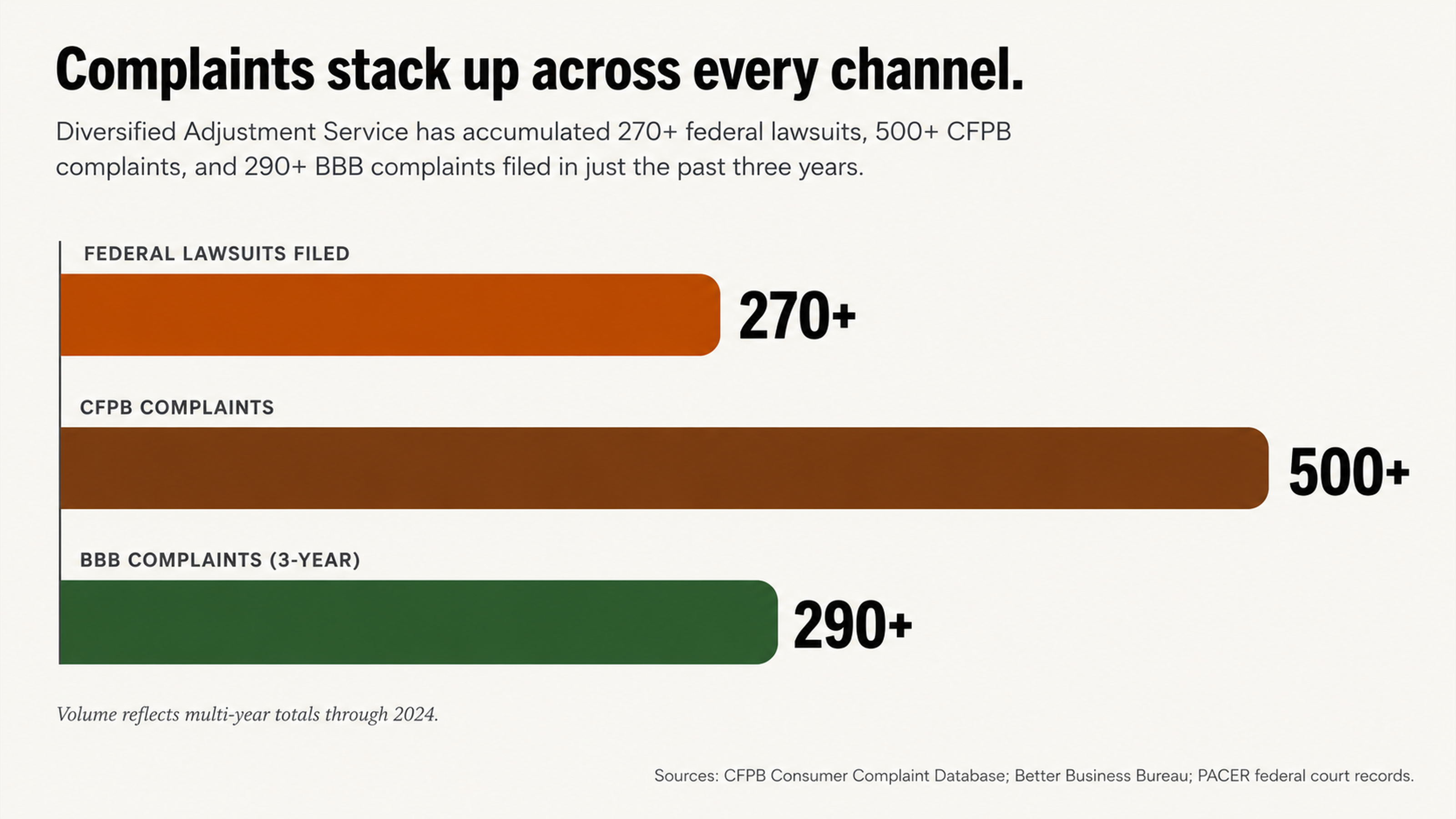

Over 270 federal lawsuits

Multiple federal court judgments finding the company liable for FDCPA violations

Over 500 complaints registered with the Consumer Financial Protection Bureau

Over 290 complaints filed with the Better Business Bureau in the last three years

An average customer review rating of 1.8-1.9 stars across various review platforms

On August 14, 2024, the Better Business Bureau published a complaint from a consumer named Sara S. that read:

“Got a recorded line to call ‘Diane’ back from diversified adjustment service. I was connected to a krista who was extremely rude. She wouldn’t listen to any of my questions and hung up on me.”

Other consumers have registered similar complaints about rude representatives.

Understanding Your Legal Rights

Federal Court Rulings

Several federal court rulings against Diversified Adjustment Service demonstrate the company’s propensity for non-compliance and underscore your legal advantage. For example:

In 2014, a federal court in Texas ruled that DAS violated the FDCPA by leaving a voicemail on a consumer’s mother’s answering machine that revealed details about the consumer’s debt to a third party. The court applied a strict liability standard. [Thompson v. Diversified Adjustment Service, Inc.]

In 2019, a federal court ruled that a reasonable juror could find that DAS’s practice of calling a consumer 77 times over the course of 73 days—despite the consumer’s repeated requests to stop calling—evinced an intent to harass, and allowed the consumer’s lawsuit to proceed. [Ammons v. Diversified Adjustment Service, Inc.]

These court rulings indicate that the company has a demonstrable history of failing to follow proper protocol.

30-Day Investigation Period

When you initiate a dispute of an item on your credit report, the credit reporting agency has a legally allotted 30-day period to conduct an investigation. This is an important period for consumers because debt collection agencies must respond with verification of the debt within this time period or the credit reporting agency must remove the disputed information.

Often, debts are sold and resold before they reach a debt collector. The documentation can become spotty, incomplete, or altogether lost during this process. If you dispute the item through the proper channels, the debt collector won’t always be able to verify the debt in time.

How to Remove a Diversified Adjustment Service Collection

Move 1: Avoid Direct Communication

Your first move is not to contact Diversified Adjustment Service directly. Debt collection representatives are trained to get you to make a payment or admission of any kind. The goal is to get you talking so that they can use the information against you.

There’s no hurry. Debt collectors create a false sense of urgency to scare you into making an immediate payment. Once a collection appears on your report, the damage is done. Making a payment won’t improve your credit score.

Also, paying a collection changes the status from “unpaid collection” to “paid collection.” Either way, the account remains on your report for the same amount of time and affects your score just the same. Most often, if your goal is to repair your credit, it’s better not to pay without the collection being removed.

Move 2: Review Your Report

Obtain a copy of your credit report from each of the three major credit reporting bureaus (Equifax, Experian, and TransUnion). Locate the Diversified Adjustment Service collection account on your report and review the details carefully. Make sure the original creditor is correct, the date of first delinquency is accurate, and the amount is correct. Ensure the information appears consistently across all three credit reports.

We’ve noticed that several complaints against DAS involve attempted collections on behalf of T-Mobile and Sprint. Multiple consumers have complained of being contacted about debts they never owed or for equipment charges on phones they’d returned. If you see a telecommunications debt from either of these companies on your report, scrutinize it carefully.

If you find one inaccuracy, don’t stop there. If one collection account on your credit report is problematic, it may indicate a larger issue. Go through your entire report with the same level of scrutiny. If you’re successful in removing one collection account, that’s all the more reason to comb through the rest of your report.

Why You Need a Professional

The DIY Trap

You may decide to tackle this on your own. That’s possible, but the likelihood of getting the outcome you want is low. This is what debt collectors do every day for a living. You’re an amateur in a professional’s game.

Debt collectors know that the average consumer will give up after one or two failed attempts. They also know that a consumer who writes their own dispute letter may inadvertently provide the collector with the information they need to verify the debt. The balance of knowledge is not in your favor.

In addition, at least one class-action lawsuit has been filed against DAS accusing the company of deceiving consumers by tacking hidden fees onto the amount they claim the consumer owes and misinforming consumers that they could only dispute a debt in writing even though the law clearly states that oral disputes are acceptable.

What a Professional Can Do For You

Credit repair experts understand what documentation debt collectors need to produce. They understand how to spot procedural flaws and use them to your advantage. Most importantly, they know how to keep the pressure on to achieve the results you need.

In individual lawsuits against DAS, consumer law firms have negotiated settlements in which the company has agreed to pay between $8,900-$9,500 as well as vacate the debt and remove it from the consumer’s credit report. That’s what you can accomplish with the right advocate in your corner.

What Happens When a Debt Can’t be Verified

The Burden is on the Creditor

When you dispute a debt, the burden shifts to the creditor to show that the debt is valid, that the amount is correct, and that they have the right to collect it. Often, a collection account can’t meet one or more of these three criteria.

Debts may change hands multiple times before they’re placed with a collection agency. The original contract could be lost. There may be a mistake in the account records or the balance may include unauthorized fees. Any one of these issues can become grounds for removal if you know what to look for.

Removal Without Paying

Many consumers assume they need to pay a collection account in order to get it removed from their credit report. This isn’t true. If a collection account contains an error, is fraudulent, can’t be verified, or if the collector fails to meet a deadline, the account can be deleted.

The frequency with which consumers are able to get results without having to pay or ever hear from a debt collector again suggests this is a common occurrence rather than an aberration. This is the intended function of the system.

On February 14, 2024, Alyssa L. posted this complaint to the Better Business Bureau website:

“This randomly popped up on my credit saying I owe $380 to T-mobile Which I don’t!!!!! I’m not even a T-mobile customer and haven’t been for over a YEAR.”

Stories like this are the reason that verification is required and why so many collection accounts fail the test.

Conclusion

Diversified Adjustment Service may have been around for 45 years, but that doesn’t mean it’s a reputable company. With more than 270 federal lawsuits, over 500 complaints with the CFPB, and an average customer review rating of less than 2 stars, DAS has a long history of concerning behavior that suggests a propensity for errors and other issues that you can use to your advantage.

You don’t have to live with a collection account on your credit report just because it’s there. You shouldn’t have to pay a debt you don’t owe or can’t be verified. And you don’t have to navigate this process by yourself.

What to Do Next

If you have a Diversified Adjustment Service collection on your credit report, don’t wait any longer to take action. The dispute process is governed by a specific timeline that, if you understand how to use it to your advantage, can help you get the outcome you need.

At FightCollections.com, we specialize in fighting debt collectors and removing questionable collection accounts from credit reports. Our experts understand the specific weaknesses of companies like Diversified Adjustment Service and know how to dispute them successfully while you remain free to focus on your life.

Contact FightCollections.com today for a free consultation. We’ll review your case and talk you through your options. You may be eligible to get the collection removed altogether. It’s time to take matters into your own hands and start rebuilding your credit.