Here’s an example of a collections agency whose reputation may be worse than the damage they’re doing to your credit report right now.

That’s right. We said it.

The existence of that account on your report is doing damage every month it stays there. And while you may be tempted to call them up and try to resolve the debt, that’s probably the worst move you could make.

Don’t make the same mistakes that GLA wants you to make. Instead, let us show you how to approach this situation in a way that puts you in control, preserves your rights, and might even get that account deleted from your credit report entirely.

Who is GLA Collections?

GLA Collection Company, Inc. is a debt collection agency based in Louisville, Kentucky that was incorporated on August 1, 1974. The company primarily collects medical debt and also operates under the names GLA Collections, GLA Collect, and Medical Insurance Billing Systems (MIBS).

Here is a brief overview of this company:

Michael Lynch serves as the President and CEO, while Patrick Lynch works as Vice President.

What does the record show about this agency?

Despite having an A+ rating from the Better Business Bureau, GLA Collection Company has an extremely concerning history of behavior that you should be aware of.

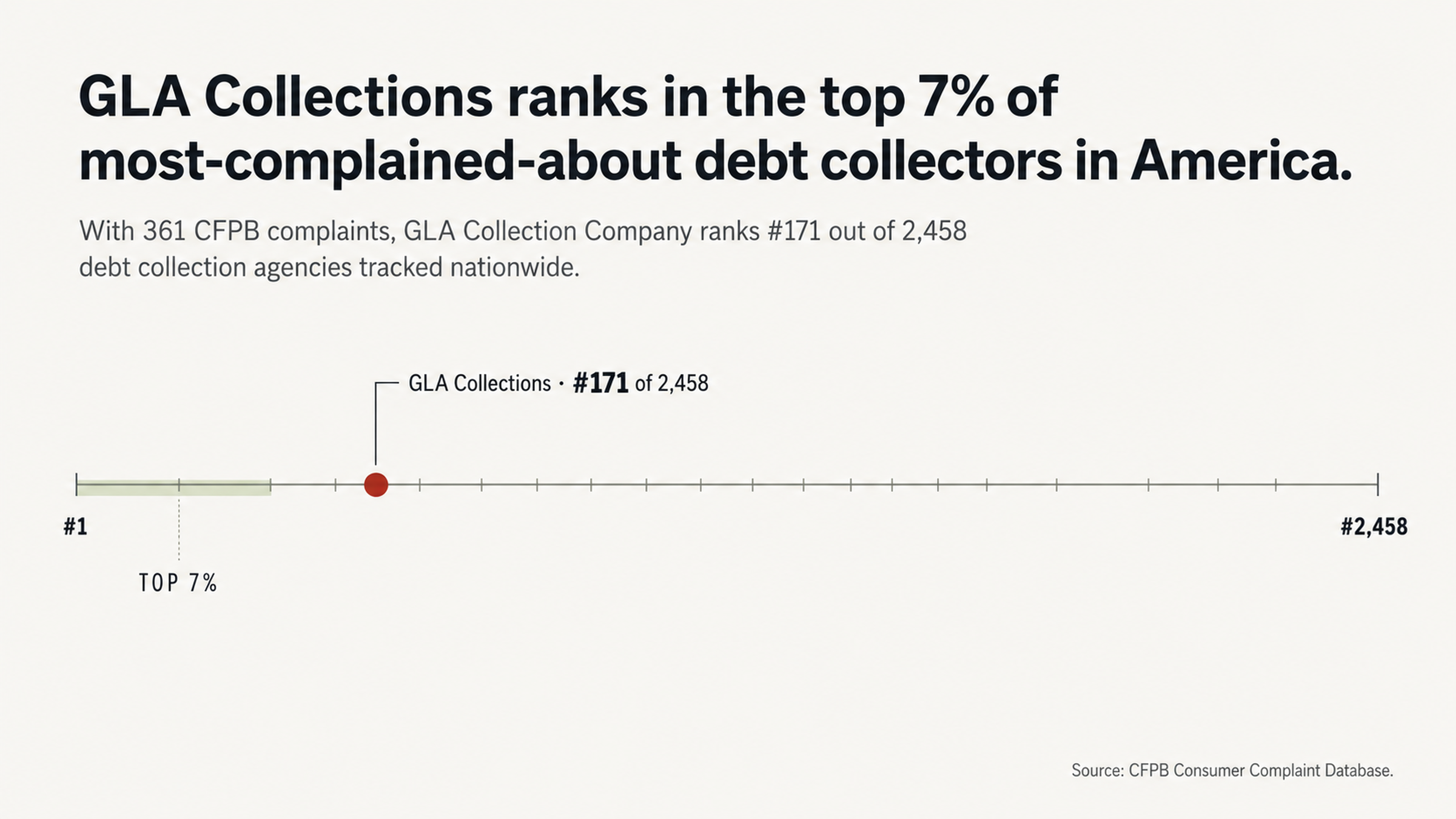

The Consumer Financial Protection Bureau (CFPB) has received more than 361 complaints about this agency, which places it at number 171 out of 2,458 total debt collection companies nationwide.

Over 130 federal lawsuits have been filed against GLA, mostly alleging violations of the Fair Debt Collection Practices Act (FDCPA), the Telephone Consumer Protection Act (TCPA), and the Fair Credit Reporting Act (FCRA). Individuals who brought FDCPA lawsuits against the company received between $3,750 and $5,100 in damages.

More than 65% of all the complaints submitted to the CFPB involve credit reporting problems. In these cases, the complainants allege that GLA reported a debt that they didn’t owe, the amount was incorrect, or that the company failed to mark the debt as disputed after the consumer disputed it.

For example, one consumer filed a complaint with the BBB after repeatedly asking for debt validation since 2021, but being told that the company could no longer communicate with their client.

Why You Shouldn’t Pay First

The credit report problem

Let’s be very clear about something: the worst thing that’s happening to you right now is the damage that collections account is doing to your credit score.

When you have a collections account on your credit report, it’s not just sitting there. It’s actively pulling your credit score down, and paying it won’t make that stop.

When you pay a collection, the status of the account changes from “unpaid” to “paid collection.” While that might sound like an improvement, the truth is that the account is still on your credit report, and it will stay there for up to 7 years from the original delinquency date. Many credit scoring models treat a paid collection almost as harshly as an unpaid one.

So when GLA calls you demanding payment, they’re counting on you not to understand how credit reporting really works. Don’t play their game.

The error issue

According to a study by U.S. PIRGs, 79% of credit reports contain errors or other major problems. Let that sink in for a second: almost 4 out of every 5 credit reports has something wrong with it.

Maybe that GLA account on your report is one of those errors.

Maybe it belongs to someone else with a similar name. Maybe the balance is wrong. Maybe the original creditor already got paid by insurance. Maybe you already paid that bill yourself. Maybe it’s past the statute of limitations. There are dozens of reasons a collection could be on your report in error, inaccurately, or even fraudulently.

If you pay it, you’re assuming it’s all square. And if it’s not? You could end up paying money you didn’t owe.

Why You Should Never Call GLA Collections

Phone calls are a trap

If you speak to someone on the phone, you have no paper trail. You leave yourself open for miscommunication and manipulation. You give the collector an opportunity to extract information from you that you shouldn’t be providing.

Every phone call you have with a debt collector is a trap. Avoid them.

As one reviewer described their experience with GLA on the BBB site:

“The GLA representative who called me was very aggressive, condescending, and extremely disrespectful. She consistently interrupted me, asked the same question multiple times because she didn’t listen to my response, and was completely hostile throughout the conversation despite my remaining calm and professional.”

That behavior isn’t accidental. Collectors are trained to apply pressure, extract admissions, and get you to commit to a payment plan over the phone. Once you say it, good luck proving what was agreed to.

Remaining silent is power

Here’s something that debt collectors don’t want you to know: you don’t have to talk to them.

When you block their calls, you’re not being rude. You’re not avoiding the issue. You’re exercising your legal right to avoid harassment.

What GLA calls “follow-up” is actually a psychological game designed to break your resolve. As their website describes, they use a “Qwik Dial system,” an integrated voice recognition auto-dialer that “contacts virtually thousands of debtors on a daily basis.”

Consumers report that GLA calls them 2-3 times a day, often using automated messages rather than live representatives.

You have the right to insist that all communication be in writing. It’s time to use it.

Written communication leaves a paper trail. It prevents manipulation. It forces the collector to commit their claims to writing. And if they can’t put it in writing? It isn’t worth the paper it isn’t written on.

The Dispute-First Approach

How disputes work

Under the FCRA, you have the right to dispute any item on your credit report that you believe is inaccurate, incomplete, or unverifiable. When you initiate a dispute, the credit bureau must investigate and verify the information with the furnisher of the data—in this case, GLA.

If GLA can’t verify the debt within 30 days, the credit bureau must delete it from your report. That’s the law. And here’s the thing about GLA: their history shows a clear pattern of failure to provide documentation and inability to produce original contracts and itemized statements.

In fact, that same BBB complaint we mentioned earlier describes a consumer who has been seeking validation from GLA since 2021, only to be told that they “could no longer contact their client.”

That’s exactly the kind of verification failure that can result in a deletion through the dispute process.

Why you need professional help

The information playing field is tilted against you. Debt collectors do this for a living. They know the laws. They know the loopholes. They know what tactics are effective.

Most people facing this situation for the first time are armed with nothing but Google and a bad feeling in their stomach.

Credit repair professionals know how to spot inaccuracies that can be disputed. They know how to document them. And they know how to navigate the verification process successfully. They know the magic language that triggers legal obligations. They know when collectors are bluffing and when they’re not.

GLA very rarely sues consumers in order to collect a debt. Their entire business model is built around putting pressure on your credit report and calling you repeatedly. That means all the leverage is on your side if you know how to use it. Professional intervention can help you use it.

Understanding Your Rights Under the Law

What the FDCPA prohibits

The FDCPA forbids debt collectors from engaging in abusive, unfair, or deceptive practices when attempting to collect a debt. This includes calling at inappropriate hours, using threats or profanity, misrepresenting the amount of the debt, and continuing to contact you after you’ve requested that they stop.

Given the 130+ federal lawsuits filed against GLA, it seems safe to say this particular company has had some issues adhering to those rules over the years. Eight of those lawsuits accuse GLA specifically of violating the TCPA as a result of their robocalling practices.

If GLA has violated your FDCPA rights, you could be entitled to statutory damages of up to $1,000, plus actual damages and attorney’s fees. Knowing your rights isn’t just about playing defense. It’s also about recognizing when you have the upper hand.

Your right to debt validation

Within 30 days of initial contact, you can request debt validation in writing from the collector. At that point, they must provide verification of your debt, including the balance and the identity of the original creditor. Until they provide that verification, they cannot continue collection activities.

According to the CFPB complaint database, failure to validate debt is one of the top issues consumers report with GLA. They request original contracts and itemized statements but get no response. They’re told the company can’t contact their client.

If a debt collector can’t validate a debt, they have no business putting it on your credit report or trying to collect it. Period.

How to Get a Collections Account Removed

Grounds for removal

A collections account can be removed from your credit report if the information is incorrect, erroneous, fraudulent, or if it can’t be verified within a reasonable amount of time. This isn’t a loophole. This is the law working the way it’s supposed to in order to protect consumers from inaccurate reporting.

Common reasons for removal include: incorrect account holder (due to identity confusion or mixed files), incorrect balance or payment history, debts that were paid or settled but not marked as such, accounts beyond the 7-year reporting period, and debts that cannot be verified because the documentation no longer exists.

Given that 65% of the CFPB complaints against GLA involve credit reporting disputes, there’s at least a fair chance the account on your report contains some kind of disputable error.

The removal timeline and process

Credit bureau investigations typically take anywhere from 30–45 days. During that time, the bureau will reach out to GLA and ask it to verify the information you’re disputing. GLA must then respond with documentation to support their reporting. If they fail to respond or can’t provide adequate verification, the item must be removed.

In some cases, this process may need to be repeated, particularly if the collector responds with a generic verification rather than providing actual documentation. Persistence is key here, but so is understanding how to escalate your dispute effectively if the initial round doesn’t get results.

Professional credit repair specialists do this all day every day. They understand how to spot disputable errors, document them properly, and navigate the verification process successfully.

They understand the specific language that will trigger legal obligations, and they recognize when a collector is trying to blow them off with boilerplate responses.

Conclusion

GLA Collections has been around for over 50 years, and their history says it all: hundreds of CFPB complaints, more than 130 federal lawsuits, a clear pattern of debt validation failures, and terrible consumer reviews.

But they’re still in business. And they’ll keep reporting that account to your credit bureaus every month until you make them stop.

Don’t call them. Don’t play their game. Don’t assume they’re right just because they say so. The dispute-first approach is the right one because it works. And because the law is on your side when the collector can’t show you what they claim you owe.

Your credit score impacts your mortgage rates. Your car loans. Your insurance premiums. Sometimes even whether you get the job you want.

That GLA tradeline is costing you money every single day. The only question is whether you’re going to keep paying or do something about it.

What’s next?

FightCollections.com specializes in disputing incorrect items on consumers’ credit reports in order to help them fight debt collectors. We know the tactics companies like GLA use, and we know how to challenge them effectively within the legal framework that’s meant to protect you.

If GLA Collections is on your credit report, contact us today for a free consultation. We’ll evaluate your situation, help you identify potential inaccuracies, and lay out your options.

You don’t have to go through this alone. And you definitely shouldn’t be taking advice from the people who are trying to collect money from you.

It’s time to stop letting GLA dictate the terms. It’s time to take back your leverage and put your credit report firmly back in your own hands.