If you have a Harris & Harris debt collection agency on your credit report, you know that this is one of the largest third-party debt collection agencies in the United States. Harris & Harris has been in business since 1968, when the company was founded in the basement of a home in Chicago.

Today, it is a national debt collection agency with more than 500 employees and is licensed to collect debt in all 50 states. Just because the company is large doesn’t mean that it is accurate, however. In fact, its size is actually part of the problem.

Here’s a quick overview of the company:

Harris & Harris primarily deals with collecting medical debt, utility bills, and government receivables. It is a third-party debt collector, which means that it is hired by original creditors to collect debt, rather than owning the debt itself. This is an important distinction because it means that Harris & Harris is not working with original documentation. Instead, it is working with information that has already been passed from one company to another.

What Do the Records Show?

Sometimes the best way to understand a company’s accuracy is to look at what the records show. According to the Consumer Financial Protection Bureau, there were 1,800 complaints about Harris & Harris in a single year. The company’s profile with the Better Business Bureau says that there have been 957 complaints filed in the past three years, including 601 complaints in the past year. Despite the large number of complaints, the company has an A+ rating with the BBB because it responds to all complaints filed against it. Despite this, the company has an average rating of just 1.08 out of 5 stars, based on 104 customer reviews.

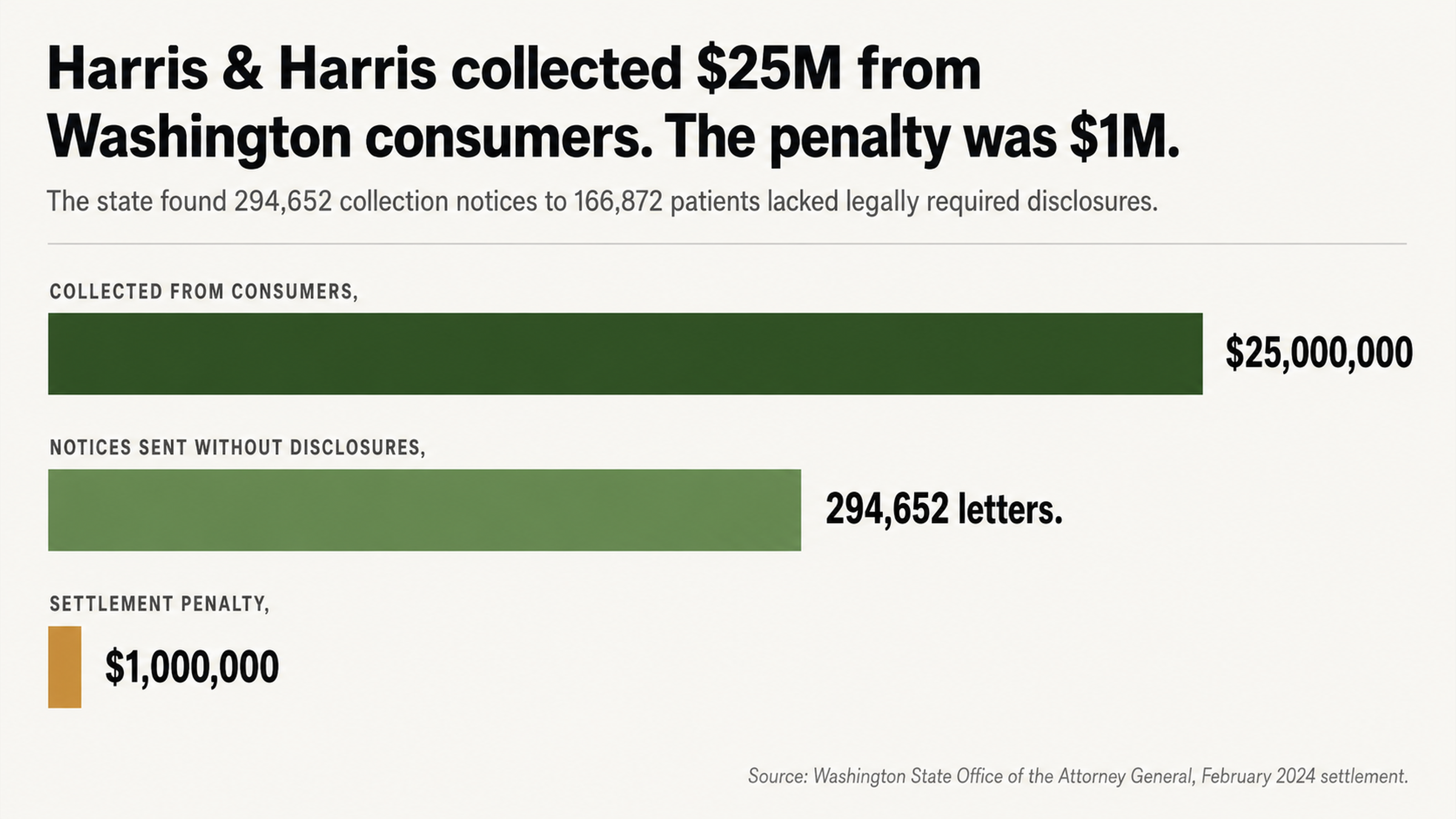

In February 2024, the Attorney General for the State of Washington announced that he was requiring Harris & Harris to pay a $1 million penalty for violating the law. According to the Attorney General, the company failed to inform nearly 167,000 patients about their rights when collecting medical debt. In all, the company sent 294,652 collection notices to Washington residents without including the information required by law, and collected almost $25 million from consumers.

This is not a minor oversight. Rather, it is a systematic problem. The Attorney General’s office also said that the company was the subject of at least 16 Fair Debt Collection Practices Act complaints in federal court in a single year, as well as several class action lawsuits. Clearly, this is a company that is processing a high volume of debt as fast as it can, and that accuracy is suffering as a result.

Understanding the Debt Collection Process

The more you understand how debt collection works, the better you’ll be able to navigate the process and protect your interests. Here’s what you need to know.

The Problem of Volume

Debt collection agencies such as Harris & Harris work on very thin profit margins. They collect a commission on the debts they collect, which means that the only way they can make money is to process as much volume as possible. The more phone calls, letters, and threats they make, the more money they can bring in. This business model incentivizes debt collection agencies to process as much debt as possible, as quickly as possible, in order to bring in as much money as they can.

What Happens on the Typical Collection Floor

So what actually happens on the floor of a debt collection agency? Essentially, debt collectors sit in front of computer screens that display information about the debts they need to collect. The information has already been pared down to the essentials: a person’s name, address, phone number, and the amount of money owed.

Of course, this information has already been passed from company to company at least once. It started with the original creditor, then was sold to a debt collection agency. At each transfer point, the information gets pared down a bit more. Some details may be lost or altered. This is just the way the process works.

In addition, debt collection agencies experience very high rates of employee turnover. It is a stressful job that generally offers mediocre pay and long hours. Employees often burn out after just a few years on the job. New employees get a minimal amount of training before they are handed a phone and a computer screen. They do not have the time or the training to thoroughly investigate the accounts in front of them. They are simply processing debts, trying to make as many phone calls as they can and bring in as much money as possible for their employer.

When this is the business model, there’s just not a lot of incentive to verify the accuracy of the accounts.

What Happens When the Records Fail

What happens when the records actually fail, and a debt collection agency does not have access to the information it needs to collect a debt? We can see what happened in the case of Harris & Harris and the Washington State Attorney General’s office.

Harris & Harris was hired to collect debts on behalf of Providence Health and Services, a chain of hospitals that is one of the largest health care providers in Washington State. As part of the collection process, Harris & Harris sent letters to patients who owed money. The letters were supposed to include certain information about the patient’s rights under Washington State law.

Instead, however, Harris & Harris included its own contact information rather than the contact information for the hospital. This made it difficult for patients to get in touch with the hospital if they had questions about their accounts.

Now, think about what this means in practice. Let’s say that you owe money to a hospital, but you’re not sure how much you owe. You may have disagreed with some of the charges on your bill, or you may not understand some of the costs. The hospital hires a debt collection agency to collect the debt, and the agency sends you a collection letter. But the letter does not actually tell you who to contact at the hospital to get answers about your bill. Instead, it only gives you the contact information for the debt collection agency.

If you call the debt collection agency, it will not be able to answer your questions about the bill. The agent who answers the phone only has the information that appears on his or her screen, which may or may not include details about your account.

This is exactly what happened to consumers in Washington State, according to the state’s Attorney General’s office. It is also what has happened to consumers around the country, according to reviews filed with the Better Business Bureau. “We have been receiving calls from this company demanding money that is owed to them. We have no idea who the money is owed to or how much we owe because they cannot tell us,” wrote one reviewer. “According to the Fair Debt Collection Practices Act, they must provide us with that information, but they refuse to.”

This is not an isolated problem. In fact, it is endemic to the debt collection industry as a whole.

The “Pay It First” Trap

Paying a debt collection agency may seem like the fastest way to make a problem go away, but it can actually make things worse. Here’s what you need to know.

Why You Should Not Pay First

If you see a collection account on your credit report, your first instinct may be to pay it. You want the account to go away, and you do not want it to affect your credit score. Unfortunately, however, paying the collection account is unlikely to make it disappear. Instead, it will simply be marked as “paid” on your credit report, and will remain there for up to seven years.

Generally, a paid collection is considered slightly better than an unpaid collection when it comes to your credit score. However, the negative impact of the collection has already been accounted for, so making a payment is not going to improve your score much.

In addition, paying a collection validates it and can restart the clock on the statute of limitations. This means that if you pay a collection, the debt collection agency may be able to sue you if you do not pay the full amount of the debt. In some cases, it may even re-age the debt, which means that it will remain on your credit report for a longer period of time.

If you are considering paying a debt collection agency in order to avoid having a collection account on your credit report, it is worth remembering that the original creditor has already written off your debt. When the original creditor hired a debt collection agency, it was because the debt was no longer collectable. The company has already benefited from the debt in the form of a tax write-off or other accounting benefit, so it really does not care whether you pay the debt or not. Instead, the pressure to pay comes from the debt collection agency itself, which has a vested interest in getting you to pay as much money as possible.

The Epidemic of Errors

Finally, it is worth noting that errors are incredibly common on credit reports. In fact, a 2012 study by the non-profit U.S. PIRG found that 79 percent of credit reports contain some kind of mistake or serious error. This is not just a minor problem. Rather, it is an epidemic of errors that can have serious consequences for consumers.

When you combine this with the incentives that debt collection agencies have to process as much volume as possible, as quickly as possible, you get a perfect storm of inaccuracy. It’s incredibly difficult for consumers to get the correct information, and to verify the information that debt collection agencies say is owed.

This is true even in cases where the consumer knows that it does not owe money. In cases where the consumer is unsure, or does not have access to all of the information about a debt, it can be almost impossible to navigate the situation correctly.

Before you pay a debt to Harris & Harris or any other collection agency, you should verify that the debt is valid and that you actually owe the money. If you cannot get the information you need to make this determination, it may be best to dispute the account with the credit reporting bureau and avoid paying it.

Why You Should Dispute First

Forcing Verification

When you dispute a collection account on your credit report, the credit reporting agency must investigate, and the data furnisher must verify. That’s not a choice; that’s the law. The Fair Credit Reporting Act mandates verification in response to a consumer dispute. Harris & Harris has 30 days to respond, and if they can’t produce documentation of the debt, the account must come off your report.

Here, the internal dynamics of a collection agency work in your favor. Those automated systems, the personnel churn, those condensed computer files. When Harris & Harris receives a verification request, someone has to find the underlying documentation for the debt, certify the balance is correct, and confirm you’re the actual debtor. In some cases, especially for debts that have been sold and resold or sat on their books for a while, that documentation might not be readily accessible.

Several complaints about Harris & Harris to the Better Business Bureau describe failed verification processes. One consumer reported sending the company two certified letters disputing a debt, which the company refused to accept.

Another customer described Harris & Harris attempting to collect from someone with the same name but a different address and birthdate, and continuing to pursue that person even after learning of the mix-up. These aren’t random anecdotes. They illustrate systemic issues with how the company responds to consumer disputes.

The Power of Silence

Debt collectors are trained to create a sense of urgency and use your emotions against you. They want to talk to you, because talking opens an opportunity to apply pressure. Every time you answer the phone or respond to a dunning letter, you’re giving the debt collector information they can use against you. You’re confirming your contact information. You may be admitting you owe the debt. You’re certainly confirming that their strategy is working.

If you remain silent, however, and instead pursue your dispute through official channels, the debt collector loses their advantage. They can’t pressure someone who doesn’t engage with them. They can’t use your emotions against you if you’re communicating by certified mail. The dispute process becomes strictly procedural, governed by rules and timelines that favor you, the consumer.

This is another reason working with a professional credit repair agency can provide an added layer of security. There’s a third party standing between you and the debt collector, so you never have to personally experience the threatening tone, the innuendos about your character, or the arbitrary deadlines designed to frighten you into paying something. While someone else handles the paperwork, you can focus on your life.

What a Successful Dispute Looks Like

Reasons for Removal

A collection account can be removed from your credit report for several reasons. The listing might include factual errors about the debt balance, the date, or your identity as the borrower. The collector might fail to verify the debt after you’ve disputed it through the proper channels. The account could be too old to report. Or the collector might have broken a consumer protection law in a way that negates its right to report the debt at all.

Harris & Harris has a history of all these issues. Its settlement with Washington State shows the company has sent consumers incomplete and inaccurate collection notices. Consumer complaints to the BBB and elsewhere describe cases of mistaken identity and failure to verify. The company has faced several federal lawsuits alleging violations of the Fair Debt Collection Practices Act, including making false statements about the consequences of not paying a debt.

That doesn’t mean any given Harris & Harris listing on your credit report is definitely removable. But it does show that the company has a proven record of the kinds of problems that support a successful dispute. These aren’t theoretical flaws; they’re a matter of public record.

Why You Need a Pro

If you try to dispute a collection account on your own, you’ll have to research the relevant laws, craft the correct language, meet key deadlines, and respond appropriately to a debt collector’s tactics, all while dealing with the anxiety of having your credit report under a microscope. Debt collectors are counting on this process being overwhelming. They know that in most cases, consumers will either abandon the effort or simply pay the debt to make it all go away.

A professional credit repair agency disputes accounts like this every day. It knows which strategies work best against which debt collectors. It knows the timelines, the documentation requirements, and the pressure points in the system. And it provides an essential layer of insulation that keeps debt collectors from contacting you directly and running the same games on you they’d run if you were working alone.

The point here isn’t just getting one questionable entry removed from your report. The point is taking back your report and making sure it accurately reflects your financial history, rather than serving as a kind of dumping ground for whatever data a debt collector happens to submit. That takes time, expertise, and perseverance, and most people don’t have the bandwidth to develop those qualities on their own.

The Bottom Line

What’s Next?

If you have a credit report listing from Harris & Harris, that’s not the end of the world. It’s not some kind of indelible scar. It’s simply a credit report entry from a company that’s admitted regulatory infractions, drawn repeated consumer complaints, and failed to verify debts. The same business model that makes the company prone to intense collection tactics also creates the vulnerabilities that make successful disputes possible.

Don’t let artificial urgency from a debt collector force you into making decisions that will damage your long-term financial outlook. Don’t pay a debt first and hope for the best. And don’t try navigating a complex dispute process by yourself when there are experts available who handle these situations all day, every day.

Take Action

FightCollections.com specializes in working against debt collectors by challenging unverifiable, inaccurate, and disputed collection listings on consumers’ credit reports. We know the tactics companies like Harris & Harris use, and we know how to challenge them through the appropriate legal channels.

If Harris & Harris is on your credit report, contact us at FightCollections.com for a free consultation. We’ll review your situation, explain your options, and help you craft a strategy for addressing this collection account the right way. Your credit future is too valuable to entrust to a company that’s already agreed to pay more than $1 million because it failed consumers.

Don’t wait for the next debt collection call. Take charge of your credit today.