If you have an IC System account showing up on your credit report, you’re likely going through a stressful process. You didn’t see it coming, your credit score just took a dive, and now you’re getting phone calls from people you don’t know, demanding money.

Your first instinct is probably to just pay the account and move on. That’s what the debt collector is counting on.

The truth is, debt collection agencies are under a lot of pressure to handle a high volume of accounts, without a lot of information to go on. There are some inherent flaws in the way the system works, which you can use to your advantage if you know where to look.

According to a study by U.S. PIRG, 79% of credit reports contain errors or serious mistakes. When you combine that with the chaotic way debt collection agencies operate, it makes sense to dispute instead of pay whenever possible.

What is IC System?

IC System, Inc. is a large third-party debt collection agency in the U.S.

IC System was founded on January 1, 1938, which means they have been in business for 88 years, and are currently under third-generation family ownership. The company has 1,100 employees and generates an estimated $257.8 million in revenue each year.

They collect debts for a variety of industries, including:

- Healthcare

- Retail

- Education

- Government

- Telecommunications

- Utilities

- Financial services

Problems with IC System

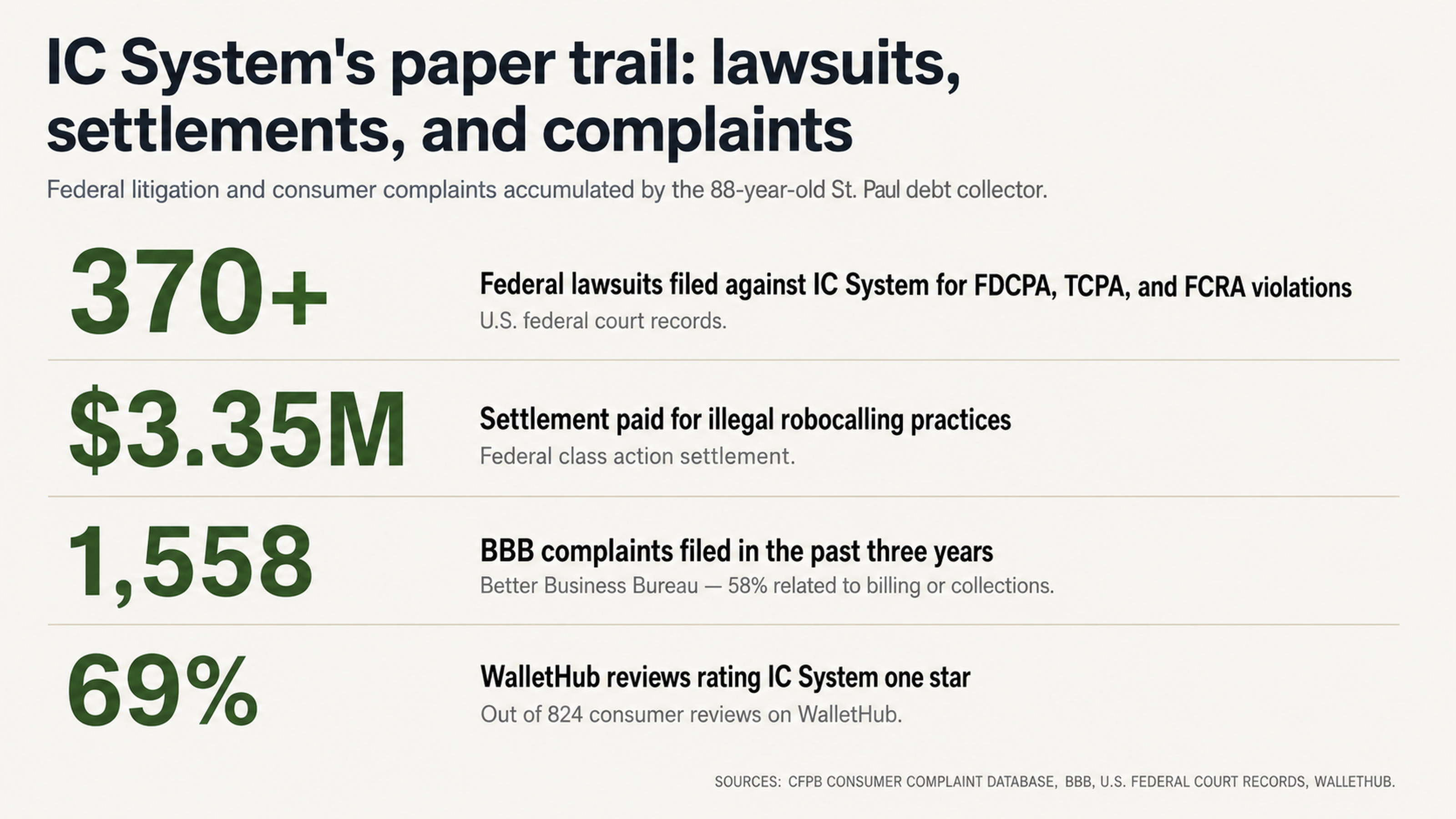

In spite of the fact that IC System won the 2021 BBB Torch Award for Ethics, the agency has been involved in more than 370 federal lawsuits for violating the Fair Debt Collection Practices Act, Telephone Consumer Protection Act, and Fair Credit Reporting Act.

They paid a settlement of $3.35 million for engaging in illegal robocalling practices, and in January 2021 the California Department of Financial Protection and Innovation opened an investigation into IC System and 11 other debt collection agencies, for potentially engaging in unlawful, unfair, deceptive, or abusive acts or practices.

On the consumer review site WalletHub, 69% of the 824 reviews are one-star reviews. The Better Business Bureau has received 1,558 complaints about the company over the past three years, with 58% of them related to billing or collections issues.

How Debt Collection Agencies Work

It’s helpful to understand how debt collection agencies work on the inside, in order to make sense of why disputing is often a good idea.

When you deal with a debt collector, you typically get phone calls and letters in the mail, demanding payment. Behind the scenes, these agencies are facing the same kinds of challenges that any high volume, low margin business faces.

High Turnover and the Volume-Based Business Model

Debt collection agencies are notorious for their high rates of employee turnover. Many collectors are paid based on the number of debts they successfully collect, which means they have an incentive to focus on speed rather than accuracy.

When a collector is handling hundreds of accounts at a time, there simply aren’t enough hours in the day to carefully verify the information for each debt. This means that collectors frequently attempt to collect debts without proper documentation to back it up.

In fact, one consumer filed a complaint with the Consumer Financial Protection Bureau (CFPB) because IC System was trying to collect an $88 debt, when the original creditor had already confirmed that the debt didn’t exist. The debt collector had simply never verified the information.

In many cases, it doesn’t make economic sense for a debt collector to verify the information for a given debt. For example, if the value of the debt is only $200, but it would take several hours of work to track down the documentation, the collector won’t bother. They’ll just move on to the next account.

The Lack of Documentation

When debts are sold from the original creditor to a collection agency, the documentation doesn’t always make the trip. Once the original creditor has written off a debt and sold it to a collector, they have no financial incentive to help the collector verify the information.

This creates a built-in flaw in the debt collection process, and many consumers have filed complaints about their experiences with IC System. They commonly state that the company:

- Refused to send a validation letter

- Continued trying to collect a debt without documentation

- Failed to respond to a certified mail request within the required 30-day timeframe

In March 2025, a reviewer on the website ConsumerAffairs described their experience like this: Called IC systems to ask for validation of debt and was hung up on 3 times, yelled at one time by a very nasty man because I wouldn’t give him my full social security number over the phone without proof that the company or debt was legit.

Why Paying a Collection Account Can Make Things Worse

When you first discover that a debt collection agency like IC System is contacting you, your first impulse will probably be to pay what you owe and make the situation go away. However, this isn’t always the best course of action.

For one thing, paying a collection account doesn’t make it disappear from your credit report. Instead, the status of the account is updated to “paid,” but the negative information remains on your credit report for years to come.

The Reality of Credit Reporting

A collection account can legally remain on your credit report for seven years, dating back to the original date of delinquency. When you pay the debt, it doesn’t restart the clock or remove the debt from your credit report. You’ll still have a paid collection on your credit report, and it will affect your creditworthiness for the full seven years.

As one reviewer complained on ConsumerAffairs in October 2024: This company harassed me and sent me to collections over an invalid debt. Also, instead of talking with me to see the debt wasn’t valid, they simply and IMMEDIATELY put the false debt on my credit report. I had to pay it just to get it off my credit, as I am a kidney failure patient.

This consumer felt like they had no choice but to pay a debt they knew wasn’t valid, because they didn’t understand their rights. The debt collection agency used urgency and fear to get them to pay something they may have been able to get removed altogether.

The Power of Time

It’s relatively rare for a debt collector to file a lawsuit against one of their customers. For one thing, it costs money to pursue litigation, and the collector may not end up getting enough money from the lawsuit to make it worthwhile.

Between the seven-year statute of limitations and the expense of pursuing a lawsuit, in many cases it’s better to dispute the accuracy of the debt and wait it out, rather than simply paying what you owe. Every month that passes without a lawsuit being filed brings you that much closer to the debt being too old to collect.

In addition, your silence can be a powerful weapon. Debt collectors are counting on the fact that you’ll react emotionally and pay them right away. When that doesn’t happen, they have to decide whether to throw more resources at the problem, or just move on to someone else.

How to Dispute a Debt

Under federal law, when you dispute a debt, the collector is required to verify that it’s yours. This can be a powerful tool for consumers, since many debt collectors may not have access to all of the information they need to prove a debt is valid.

What the Debt Collector Must Prove

When you dispute a debt, the collector must provide verification that includes:

- The amount you owe

- The name of the original creditor

- Proof that you’re responsible for the debt

If they can’t provide that information, they’re required to stop trying to collect the debt.

The credit reporting agencies also have requirements they must meet. If they can’t verify a disputed credit reporting item within a reasonable amount of time, they’re required to delete it from your credit report altogether. If a collection account is inaccurate, erroneous, fraudulent, or simply can’t be verified, you may be able to get it permanently deleted.

The important thing to understand here is that once a debt is successfully disputed and deleted, in most cases the collector won’t have any mechanism to re-report the account. In other words, once the account is gone, it’s usually gone for good.

Why You Need Professional Help

There’s an information imbalance when you’re dealing with a debt collector. The collector understands the ins and outs of the credit reporting system, and the strengths and weaknesses of their documentation. Most consumers have never dealt with the debt collection process before, and can’t effectively advocate for themselves.

Plus, debt collectors understand how to use your natural tendency to defer to authority against you. They may make vague threats on the phone, referencing legal action or implying that they’re backed by some kind of official body. If you don’t know any better, you may pay a debt you could have disputed, just because you don’t want to cause any trouble.

If you work with a professional credit repair agency, you can get help leveling the playing field. Credit repair experts understand what the debt collector needs to prove in order to collect a debt, and how to craft an effective dispute letter. They also know when a debt collector is bluffing, and how to respond.

Common Complaints About IC System

When you look at the complaints that have been filed against IC System, you start to see some patterns emerging. Understanding these patterns can help you figure out whether you’re in a situation that might be open to a successful dispute.

Failure to Validate

The single most common type of complaint about IC System is a failure to validate. In 69% of cases, consumers say they didn’t receive enough information to verify that the debt was valid, and requests for documentation went unanswered or resulted in generic responses.

This may indicate some kind of systemic problem with documentation within the company. If the debt collector can’t prove the basic elements of a debt, that might be a debt that you can successfully dispute. Whenever a collector can’t verify a debt, that’s an opportunity for you to get it removed.

Wrong Person or Wrong Debt

Mix-ups are another common issue. Consumers complain about cases where a father was being dunned for a debt that rightfully belonged to his son, debts that had already been paid being sent to a collection agency, and debts that had been purchased from another collection agency without the proper chain of ownership.

In November 2025, a consumer filed a complaint with the BBB, saying: This company is willingly participating in fraud. Even after I proved the debt they claim I owe was fraudulent they continue to attempt to get me to pay it.

Whenever a debt collector ignores evidence that a debt is invalid and continues to try to collect it anyway, they may be exposing themselves to legal liability.

What to Do Next

IC System is a typical debt collection agency, in the sense that they handle a high volume of accounts without a lot of documentation to back them up. With their $3.35 million settlement for illegal robocalling, more than 370 federal lawsuits, and thousands of complaints from consumers, it’s clear that this is a company where mistakes can happen.

Those same operational realities also mean that there are opportunities for consumers who understand how the system works. Whenever a debt can’t be verified, it has to be removed. Whenever documentation has been lost in transit from the original creditor to the debt collector, it can’t magically reappear. And whenever a debt collector is attempting to collect the wrong amount, or from the wrong person, they’re violating federal law.

So the next time you’re trying to decide whether to pay or dispute, remember that the debt collector is counting on you to do the former. But the more you understand about the way the system works, the more power you’ll have to do the latter.

Contact us today at FightCollections.com for a free consultation. We’ll talk to you about your situation and help you understand how to move forward. You don’t have to navigate the system on your own.