If you find an unfamiliar collection account on your credit report, your first reaction might be to panic.

If that collection account is from Jefferson Capital Systems, you might feel tempted to send a check to get rid of it as quickly as possible. Debt buyers like Jefferson Capital are counting on that reaction, but you shouldn’t act out of fear when dealing with debt collectors.

A lot of people believe that paying a collection account will help you recover more quickly from credit damage. Unfortunately, that’s not always true. Even if you pay a collection account, it will remain on your credit report. And if you pay a collection account that is not legitimate, you could end up with a bigger headache than you expected.

Before you send a payment or make a phone call to Jefferson Capital, you need to know what this company is, what they do, and why you should dispute the account before you take any other action.

What is Jefferson Capital Systems?

Jefferson Capital Systems is a debt buyer. They are not a traditional debt collection agency. Instead of working with creditors to collect debts, they buy defaulted consumer debts from the original creditors and then attempt to collect on those debts themselves.

Understanding this is important because debt buyers often can’t prove that the debts they are trying to collect are valid.

What is Jefferson Capital Systems’ reputation?

According to Portfolio Magazine, Jefferson Capital Systems is the fourth-largest debt buyer in the United States. They earn about $577 million per year. They operate in the United States, Canada, the United Kingdom, and Latin America. Despite their size and A+ rating from the BBB, their reputation with consumers is not impressive.

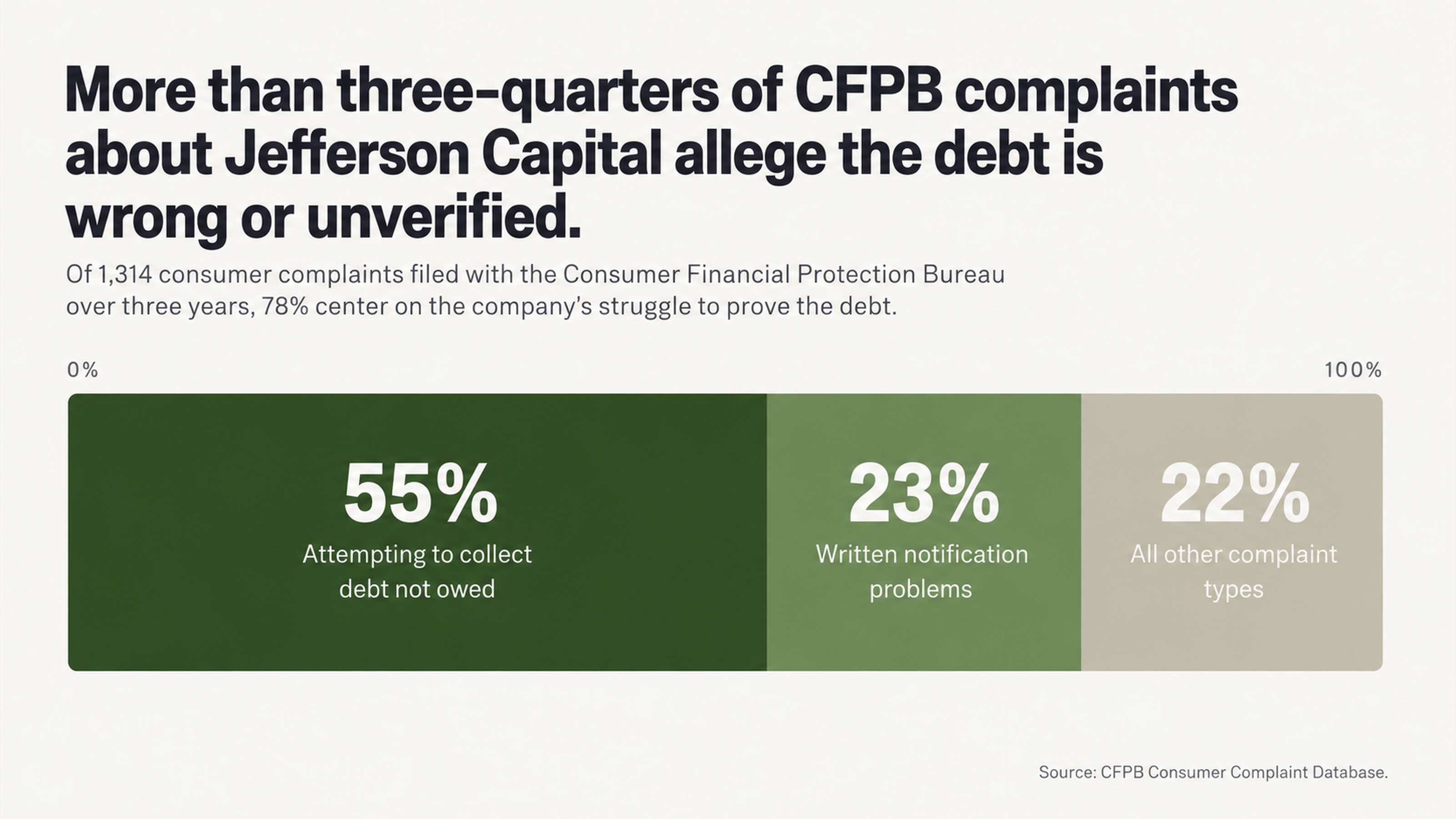

In the last three years, the Consumer Financial Protection Bureau has received 1,314 complaints about Jefferson Capital Systems. During the same period, the Better Business Bureau has received 1,094 complaints. On the BBB website, the average customer review rating is just 1.02 out of 5 stars, based on 89 reviews.

In 2008, Jefferson Capital Systems and its parent company, CompuCredit Corporation, agreed to settle charges with the Federal Trade Commission and the FDIC. The company agreed to pay at least $114 million in consumer redress, as well as a $2.4 million civil penalty, to settle allegations of abusive debt collection practices and operation of a deceptive debt-transfer credit card program.

As a result of the settlement, the company was permanently barred from calling consumers more than 20 times per day and from calling consumers before 8 a.m. or after 9 p.m.

The biggest myths about paying collection accounts

Myth #1: Paying a collection account will help your credit.

Many people believe that paying a collection account is the best way to repair their credit after a debt has gone to collections. Unfortunately, this is not always the case. When you pay a collection account, the account will show on your credit report as a paid collection account. It will still remain on your credit report for 7 years from the original delinquency date. Paying the account may not improve your credit score.

In fact, paying a collection account could create more problems for you in the future. When you pay a collection account, you may inadvertently acknowledge that the debt is valid. In some states, acknowledging the debt could restart the statute of limitations, giving the debt collector more time to sue you. Before you pay a collection account, make sure you understand the potential risks.

The truth is, you don’t have to pay a collection account to get it removed from your credit report. In fact, it’s rarely a good idea to pay a collection account without disputing it first. According to a study by U.S. PIRG, 79 percent of credit reports contain errors or serious errors. If the information that Jefferson Capital is reporting is not accurate, complete, and verifiable, you have the right to dispute it and have it removed.

Myth #2: The debt buyer has already verified that you owe the debt.

Many consumers assume that debt buyers would not attempt to collect a debt unless it was valid. Unfortunately, that’s not true. Debt buyers purchase debts in bulk, often paying just pennies on the dollar for thousands of accounts. When they buy the debts, they may not receive all of the documentation associated with each account. In some cases, the documentation may be unavailable.

As a result, debt buyers may not have the documentation they need to prove that you owe the debt. In many cases, consumers have successfully disputed debts from Jefferson Capital and had them removed from their credit reports.

In fact, court records show that Jefferson Capital Systems has a documentation problem. In the case of Jefferson Capital Systems LLC v. Rice, a ruling from the Missouri Court of Appeals in February 2024 upheld the denial of the company’s motion to compel arbitration. According to the court documents, Jefferson Capital failed to meet its burden to establish a complete chain of assignment of arbitration rights from the original creditor.

Debt buyers like Jefferson Capital are required to show a complete chain of assignment with admissible evidence to prove the debt is valid in their hands. Clearly, the company is struggling to meet this burden.

Data from the CFPB complaint database indicates that about 55 percent of the complaints the agency has received about Jefferson Capital are attempts to collect a debt that the consumer does not owe. Consumers say that the debt is not valid, that it belongs to someone else, or that it has already been paid.

Another 23 percent of complaints are about problems with written notification about a debt, usually because the debt collector failed to validate the debt after the consumer requested validation.

Why you should dispute first

The law requires debt collectors to validate debts

When you dispute a debt, the law requires the debt collector to validate it. In fact, under the Fair Debt Collection Practices Act, debt collectors are required to stop attempting to collect a debt until they provide the validation. Debt buyers like Jefferson Capital may struggle to validate debts because they often do not retain all of the documentation associated with the original account.

The debt collection business model relies on consumers making payments without disputing accounts. Debt collectors attempt to collect as many accounts as possible because they know that most consumers will pay without asking questions. When consumers dispute accounts, the debt collector must respond by validating the debt. In many cases, it’s just not worth their time and money to respond, so they give up.

Here’s what one verified BBB reviewer experienced: “I have no idea as to who the original debtor is. I don’t nor have I ever taken a loan from this bank Jefferson LLC says I owe. This entity needs to be brought before the court asap. Corruption last I checked was illegal. This company is clearly bullying people to make income.” This reviewer’s experience is not unique. Debt buyers often do not have the documentation to validate debts.

Information asymmetry

Debt collectors understand their business a lot better than consumers do. They know which tactics will prompt consumers to make payments. They know that consumers are afraid of damage to their credit. They are counting on consumers not understanding their rights under federal and state consumer protection laws.

This information asymmetry is why consumers who work with a professional to handle collections get better results than consumers who try to handle things on their own. A credit repair professional understands the dispute process and knows what documentation to request. The professional will also be able to tell whether the collector has met its burden under the law.

Here’s what one CFPB complaint says about the experience of dealing with Jefferson Capital: “I have asked Jefferson Capital Systems to stop contacting me via phone several times. I requested to only be contacted by mail; however they repeatedly call. They over talk me and attempt to belittle me. This is not an effective method of trying to get someone to pay a debt. This is illegal and I’m getting extremely tired of it.” Consumers who have professional representation do not have to go through this type of harassment.

Federal and state laws favor informed consumers

In recent years, Jefferson Capital Systems has faced more than a dozen class action lawsuits. The suits, filed in federal courts in New York, Wisconsin, Indiana, Georgia, and New Jersey, allege that the company has engaged in a pattern of violations of the Fair Debt Collection Practices Act.

The suits allege that Jefferson Capital engaged in a variety of misconduct including use of misleading language in collection letters, failure to identify the original creditor, attempts to collect time-barred debts without making required disclosures, and improper credit reporting of debts that had been discharged in bankruptcy proceedings.

Lawsuits against Jefferson Capital Systems point to practices that routinely cross legal lines. Each victory for consumers in these cases sets further precedent to protect your rights. If you dispute instead of paying, you have the opportunity to be among those who benefit.

Why You Should Say Nothing Now

There’s a tendency to want to talk to debt collectors, explain your situation, or negotiate on the spot when they call. Don’t do it. Anything you say can and will be used against you. It gives them the opportunity to get information out of you, to secure admissions of debt, or to obtain payment information for partial payments.

If you say nothing and insist on everything in writing and going through the proper channels, you’re removing their most powerful weapon: your emotions. You’re also removing their ability to create a false sense of urgency. After all, they can’t pressure you if you’re not on the phone with them. They can’t create urgency if you demand everything in writing and properly documented.

Credit repair is not a sprint; it’s a marathon. Given the seven-year cycle for most negative items on your credit report and the amount of time you have for the investigation process of a dispute, it generally pays to slow down rather than speed up. Paying something quickly might make you feel better today, but systematically disputing the debt protects your rights and usually provides a better outcome in the end.

What to Do Now

Understanding the Clock

If you’re seeing Jefferson Capital Systems on your credit report, you need to understand that time is not on their side. They’ll try to make you think it is with threats and deadlines designed to override your rational thinking. In reality, you have time to figure out your next move instead of simply reacting to their call.

That being said, time is of the essence if you want to prevent the worst possible outcome. Though it’s relatively rare for debt buyers to sue given the number of accounts they own, it does happen. Reaching out immediately to get help can ensure you understand your options and how to proceed if they decide to take you to court.

The good news is that the collection can potentially be removed if the information is incorrect, erroneous, or fraudulent. It can also potentially be removed if they cannot verify it within a reasonable amount of time. Your goal in this situation is not to prove that you don’t owe the money. Their goal is to prove that you do owe it with the right documentation and an accurate credit report. If they cannot fulfill their burden, removal is possible.

Why You Need Professional Help

Attempting to handle a collection dispute on your own puts you at a distinct disadvantage. You likely do not know what documentation is specifically required under your state’s law. You may not recognize if a debt collector has violated the FDCPA. You certainly cannot match the experience of a company that’s handled thousands of similar cases.

Credit repair experts understand how to properly request debt validation. They understand how to spot inaccuracies on a credit report. They understand how to effectively use consumer protection laws to your advantage. They also understand that across the industry, debt collectors respond to 97 percent of complaints filed but only 0.2 percent of those complaints result in monetary relief when the consumer does not have representation. Having professional representation on your side changes those odds dramatically.

On WalletHub, Jefferson Capital Systems has an average rating of 1.8 out of five stars based on 700 reviews, with 74 percent of those reviews being one-star ratings. On PissedConsumer, verified reviewers rate the company at 1.0 out of five stars. These are the results consumers can expect when facing this company on their own without the right support and knowledge.

The Bottom Line

Jefferson Capital Systems is one of the largest debt buyers in the country, owned by a private equity firm and now a publicly traded entity. They have more resources and scale than any individual consumer can hope to match in a dispute. However, their history of regulatory actions against them, their current class action suits, and their routine failure to validate debts highlight weaknesses that educated consumers can use to their advantage.

The myths driving you to make a quick payment serve the debt collector, not you. Paying the debt does not remove the damage already done to your credit. The debt buyer may not have the documentation they need to prove the debt.

Finally, the courts are increasingly ruling against the practices of these debt buyers. Disputing the debt first, through the proper channels and with the right professional help, puts you in the position to capitalize on all of these facts.

Your credit report can make or break your ability to rent an apartment, secure a loan, get a job, and achieve any level of financial stability. A collection account from Jefferson Capital Systems puts all of those things in jeopardy. The real question is not if you should respond but how you should respond to protect yourself and your future.

What to Do Next

Don’t let Jefferson Capital Systems force you into making decisions about your financial future that you will regret later. Don’t assume you owe the debt simply because they’re telling you that you do. Don’t try to navigate this process on your own against a company that has 23 years of experience and hundreds of millions of dollars in resources.

FightCollections.com specializes in helping consumers dispute collection accounts and remove information from their credit reports that is inaccurate, erroneous, or unverifiable. Our experts understand the tactics debt buyers use and the legal obligations they must fulfill. We help level the playing field so you can make informed decisions about your financial future.

Reach out to FightCollections.com today for a free consultation. Let us help you understand your situation, explain your options, and get started on the path to getting Jefferson Capital Systems off of your credit report once and for all. Your financial future is too important to leave up to chance or fear.