Linebarger Goggan Blair & Sampson LLP is a large government debt collection law firm that has been in business since 1976. They specialize in collecting unpaid tolls, property taxes, court fines, parking tickets, and other government debts owed by Americans.

Linebarger has offices in 21 states and manages over $10 billion in delinquent accounts, making it much bigger than your typical debt collection agency.

Here is their basic contact information:

If you received a collection letter from Linebarger or noticed this law firm is listed on your credit report, you're not alone. They collect roughly $1 billion per year from millions of consumers across the United States.

Disturbing History You Need to Know About

Before I show you how to deal with Linebarger, it's essential you understand their history, which includes some very troubling facts.

In 2002, partner Juan Pena was indicted for allegedly bribing two San Antonio City Council members in an attempt to secure a $35 million tax collection contract. He eventually plead guilty to bribery conspiracy and bank fraud, for which he was sentenced to 30 months in federal prison and ordered to pay a $1 million fine.

In addition to criminal activity, Linebarger has also paid out over $19.8 million in class action settlements. For example, in 2016, they agreed to a California settlement of $3.4 million. This particular settlement covered 82,906 consumers, as the firm had been sending collection letters into California despite not employing California-licensed attorneys. In 2019, another California class action settlement reached $9 million, this time covering approximately 151,000 class members who paid debts between September 2013 and April 2019.

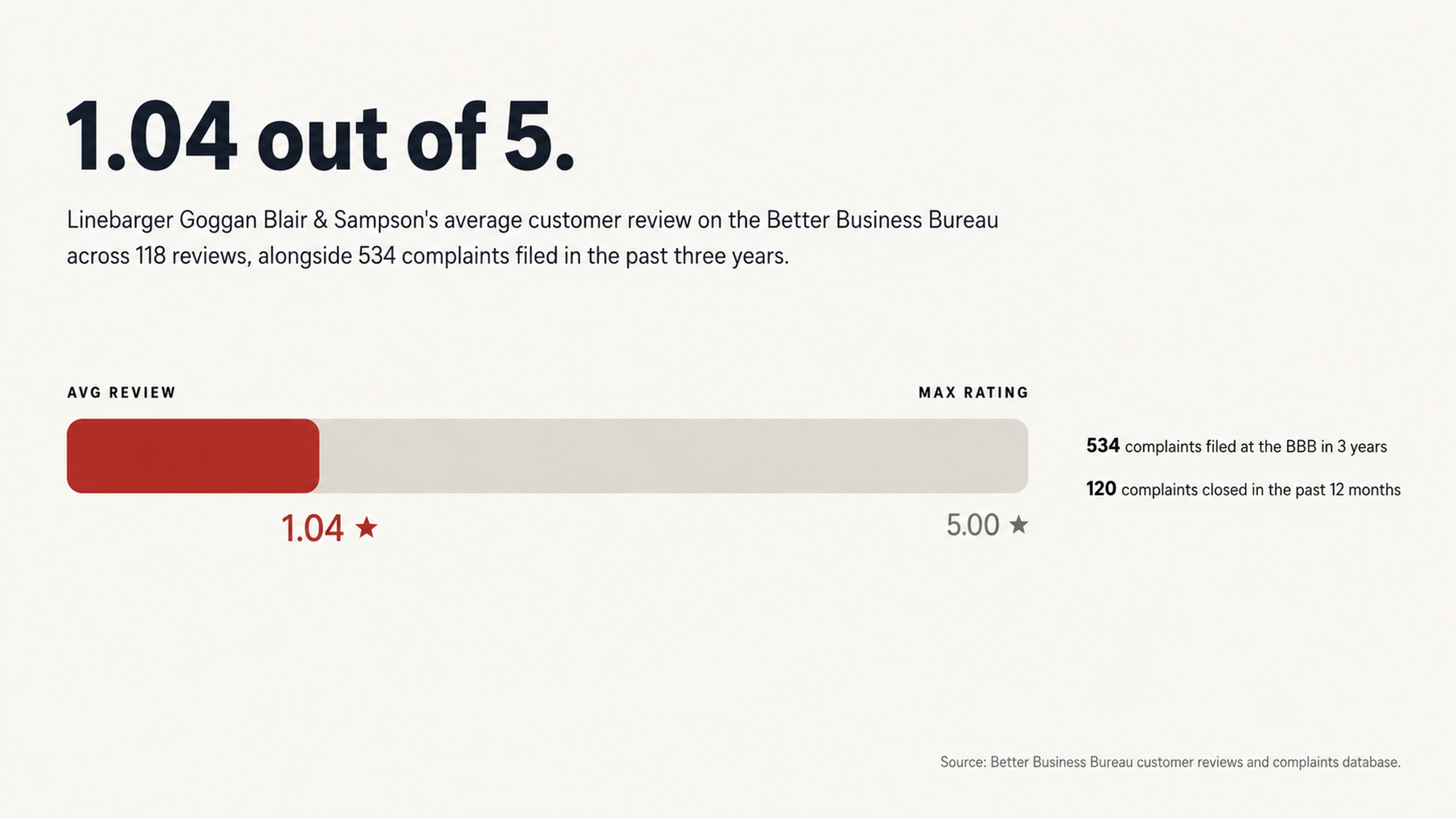

On the customer satisfaction front, the company has a Better Business Bureau (BBB) accredited rating, but its average customer review rating is a terrible 1.04 out of 5 stars, based on 118 reviews. The BBB has received 534 complaints about Linebarger in the past three years, with 120 complaints closed in the past 12 months.

Why You Should Never Pay First

Now that you know a bit about Linebarger's troubling history, let's cover the documentation gap that exists with government debt collection, which is important for you to understand because it creates an enormous opportunity for you.

Unlike typical debt collection agencies that attempt to collect credit card debt or medical debt, Linebarger collects debt on behalf of a government entity. This is an important distinction because it affects the legal protections you have and the type of documentation the collection agency is required to maintain.

Whenever debt is transferred from one agency to another, the associated documentation often becomes degraded or incomplete. For instance, a parking ticket from five years ago may have been transferred through multiple collection systems before it was handed over to Linebarger. Each time the debt was transferred, the risk of errors and lost documentation grew.

A CNN Money investigation revealed how the debt collection process often turns small debts into staggering burdens. One driver's unpaid tolls of $1.25 blossomed into a $287 debt, while another consumer's $100 speeding ticket grew into a $2,200 debt once penalties, court costs, jail fees, and collection fees were tacked on.

The Importance of Verifying the Debt

All collection accounts are required to be verifiable. This isn't just a recommendation; it's a requirement. Any time you dispute a collection account, the debt collector must provide documentation that proves the debt is valid, it belongs to you, and the amount is accurate.

According to a study conducted by U.S. PIRGs, 79% of credit reports contain errors or other serious mistakes. This means the odds are in your favor if you take the time to carefully review collection accounts instead of simply paying them without question.

Many of the consumer reviews I've read mention verification issues. Here's what one BBB reviewer had to say: "I received a collection letter for a red light violation that I did not commit. This law firm looks for individuals with the same name and sends out letters hoping that they will freak out and pay it. What a scam! It was for a car not even similar to mine and 90 miles away." Wrong-person collections like this are just one type of verification problem.

What Happens When You Dispute a Collection Account

If you dispute a collection account, the debt collector must verify the account by providing documentation that proves the debt is valid and belongs to you. If they can't verify the debt within a reasonable amount of time, the account must be removed from your credit report.

Once you've disputed a collection account and had it removed from your credit report, the collector typically doesn't have the ability — or the incentive — to have the account re-reported. The removal is usually permanent. This is a much different outcome than simply paying the collection account, which would leave the negative account on your credit report for years to come.

Keep in mind, disputing a collection account isn't about deciding whether you actually owe money or not. It's about the collector's ability to verify the debt with the proper documentation. Given the frequency with which documentation becomes lost or degraded as it's transferred from one agency to the next, this is an important distinction.

Why You Should Say Nothing

It's generally not a good idea to call a collection agency like Linebarger. In fact, it should be the last thing you do. Collection agencies are professional operations that employ representatives who are trained to get you to pay them money. Every time you speak with a debt collector on the phone, you have the potential of saying something that will hurt your case or waive rights you didn't realize you had. The balance of power is always in the debt collector's favor.

Here's what one BBB reviewer had to say about her experience with Linebarger: "Literal frauds and scammers who sent me a payment demand for a traffic infraction in a state where I have never ever been. I demanded that they delete the payment demand, which they did; however, two years later, they sent the identical demand." Engaging with debt collectors directly rarely results in the outcome consumers hope for.

Another reason you shouldn't interact with a debt collector is because they use fear as a tactic. Their letters often threaten arrest, wage garnishment, license revocation, and even property liens. According to a CNN Money investigation, Linebarger's letters threaten actions that a typical debt collection agency can't because the firm is a government-backed collector. Understanding this should help you refrain from reacting out of fear.

The Credit Repair Advantage

If you are dealing with a Linebarger collection account, you are not alone. Credit repair companies face them every day. They know what steps the collection agency has to take. They know what documentation it has to have. They know the technicalities of disputing an error. This gives you an advantage.

If you try to take this on yourself, you have to learn this system, and navigate it while facing an adversary that does it all day, every day. That’s a steep learning curve, and mistakes will cost you. The collection company knows this and will count on you making mistakes.

Credit repair companies will also provide you with a buffer. They will handle communication, keeping you from saying something to the collection company that you shouldn’t. They will know which technicalities to push and which documentation the collection company is likely missing.

Linebarger’s Weaknesses

The class-action settlements in California point to one of Linebarger’s weaknesses. The company collected from California residents for over a decade without any California-licensed attorneys on staff. In defending itself against the class-action suits, Linebarger claimed it “was not practicing law by sending a letter.” Ultimately, it had to pay $12.4 million in settlements.

This may not be a problem unique to California. If you get a collection letter from a law firm, you have every right to assume a lawyer is involved in your case. Whether that’s actually true is a different story and worth exploring in your dispute.

The Iowa case offers another example. Linebarger was accused of violating the FDCPA by threatening to revoke licenses and hold people in contempt of court. It also stood accused of not disclosing its 25% collection fees. Between 2012 and 2018, Linebarger collected $58.6 million from Iowans and was paid nearly $12 million in collection fees. Iowa ended its contract with the company in January 2021.

The Wrong Person

Another pattern that emerges in the consumer reviews is data quality. A second BBB reviewer wrote: “0 stars. A total scam - a threatening collection letter for unpaid tolls in a state I have never been to. Oh, and I do not own a car. Sloppy and shady.”

These aren’t isolated incidents. They’re a pattern. Wrong-person collections happen when a collection company tries to collect from someone because of a name match or some other identifier without verifying that it’s the right person. When you have as many accounts as Linebarger claims to have — $10 billion in delinquent government accounts — it’s easy to see how this could become a problem.

Every wrong-person collection is a total documentation failure. The collection company cannot document that you owe a debt if you do not owe it. These are exactly the kinds of reasons why you should dispute a debt before paying it. You may end up being asked to pay for something that was never your responsibility in the first place.

Start Building Your Paper Trail

What You’ll Need

You should never start the dispute process until you know exactly what is on your credit report. Start by requesting a copy from each of the three reporting bureaus and review them carefully. Make a note of what Linebarger has reported: the amount, the original creditor, the dates, and any other information.

Pull together any communication you’ve received from the company. It will detail what the company says you owe and may include language you can challenge for accuracy. Keep all of this in a folder — either a physical folder or a digital one — where you can access it throughout the process.

Also, pull together anything you have that disproves what Linebarger is claiming. If it says you incurred a toll in a city where you’ve never driven, find records that show where you were at the time. If it says you owned a car you’ve never owned, find documentation of the cars you did own. This will be ammunition you can use in your fight.

What They Have to Prove

When you dispute a collection account, the burden shifts to the collector. It must provide documentation to prove that the debt is legitimate, that you are the right person, and that the amount is accurate. It can’t just keep saying that you owe the debt. It needs records.

Given that government debts can be passed around a bit — often originating as tickets that may change hands multiple times before they land at a collection agency — this chain of documentation can be incomplete. The original parking ticket from seven years ago may have been passed around the city’s municipal offices before being assigned to a collection agency and landing at Linebarger. Not all of the records may have made all of those journeys successfully.

That’s OK. This is a legitimate way to get a collection account removed from your credit report, even if you did owe the original debt. There’s a reason that the burden of proof for verifying a debt is on the collector. If it cannot verify a debt, the debt should not remain on your report.

Now What?

Why You Should Act Now

A collection account is a negative mark on your credit report, and there are statutes of limitation that govern how long you have to pursue some potential remedies. That means the sooner you address a Linebarger collection account that has landed on your credit report, the better. The longer you wait, the longer that negative mark is affecting your credit score, and the fewer options you may have when you do decide to act.

That does not mean you should rush into anything. You should not rush to pay the debt or call the collection company directly. All of that is likely to end badly for you. Instead, you should rush to get professional help on your side and then not rush to pay the debt. That’s the way you end up with the best outcome.

Help Is Available

If you find that Linebarger Goggan Blair & Sampson LLP has placed a collection account on your credit report, you do not have to go through this process alone. At FightCollections.com, we specialize in working with consumers to dispute erroneous, inaccurate, and unverifiable collection accounts from debt collectors.

We know what kind of documentation a collection company is supposed to have. We know how to challenge it. We have watched the way government debt collection companies operate and have seen all of the patterns — the wrong-person collections, the inflated fees, the threatening letters, the failure to verify debts. We know where the weaknesses are and how to use them to your advantage.

Contact FightCollections.com today for a free consultation. Let us take a look at your situation and at what Linebarger is claiming. We’ll help you come up with a strategy for getting the account off your credit report as quickly as possible. The sooner you start that process, the sooner you can put it behind you and move on with a cleaner credit report.