It can be quite daunting to discover a new collection account on your credit report that you’ve never heard of.

But if that collection account happens to belong to Lockhart Morris and Montgomery, you’re dealing with a debt collector that has a history of consumer complaints and a documented history of compliance issues. And that is good news for you if you’re considering a dispute. After all, studies by U.S. PIRGs have found that 79 percent of credit reports contain errors or other major mistakes.

So if Lockhart Morris and Montgomery is reporting an account on your credit report, there is a pretty good chance that the information they’re reporting is incorrect in some way. And that could provide the ammunition you need to successfully dispute the account.

Who is Lockhart Morris and Montgomery?

Lockhart, Morris and Montgomery, Inc. is a Texas-based third-party debt collector and debt buyer. The company was founded on June 21, 2004, and has over two decades in the collections industry. It also goes by the names LMM and LMM Inc.

Lockhart Morris and Montgomery is licensed to collect debt in California, Nevada, North Carolina, Tennessee, Colorado, Massachusetts, Minnesota, New York, and New Mexico. LMM’s divisions include Vocational Recovery Solutions (educational debt) and Apex Division (security and alarm debt).

A Closer Look at Lockhart Morris and Montgomery

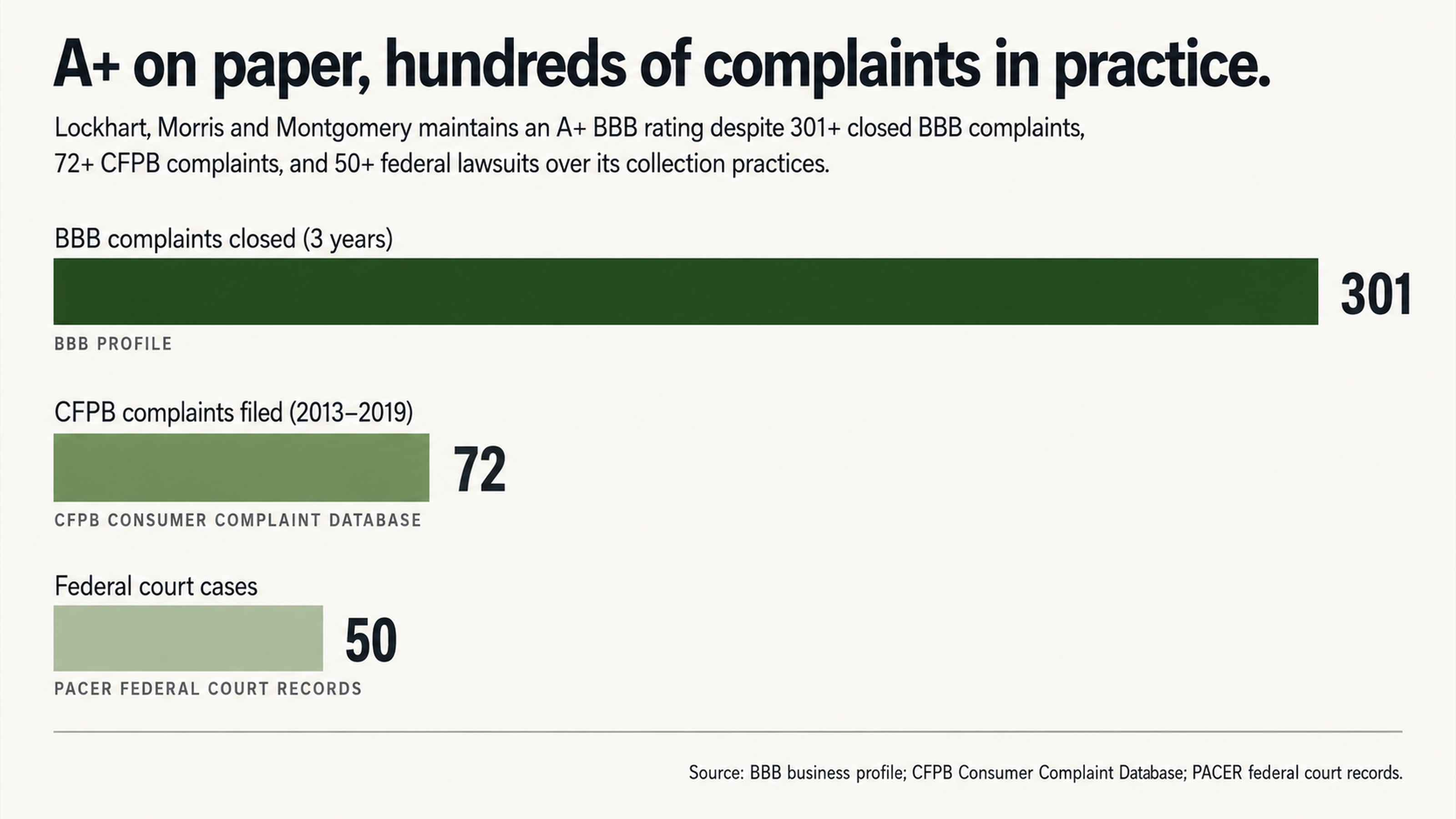

Despite its A+ rating from the Better Business Bureau (BBB) since Dec. 12, 2012, Lockhart Morris and Montgomery has had more than 301 complaints closed in the last three years, according to its BBB profile. And its customer review rating is a far-less impressive 2.59 out of five stars based on 29 reviews.

In addition, the Consumer Financial Protection Bureau’s (CFPB) complaint database shows more than 72 complaints filed against Lockhart Morris and Montgomery between Nov. 5, 2013, and Dec. 4, 2019. And the company has been involved in more than 50 federal court cases related to its collection practices.

Where Lockhart Morris and Montgomery Falls Short on Compliance

A History of Consumer Complaints

Lockhart Morris and Montgomery’s history of consumer complaints is alarming. In April 2025, a consumer named Diana H filed a complaint with the BBB against Lockhart Morris and Montgomery. She said the company resurrected an old medical debt that had previously been removed from her credit report. “This company has no documentation that I owe this debt, nor have I been contacted by them about this debt,” she wrote. “I have contacted a lawyer about this issue.”

Another consumer, Tyler W, called Lockhart Morris and Montgomery a “scam” in a March 2025 complaint. He said the company wouldn’t even communicate with his lawyer and was refusing to remove a “fraudulent charge” from his credit report. He added that the company’s representative was “extremely rude” when he attempted to explain his situation.

We could go on and on. But the point is that this isn’t an isolated problem. There are hundreds of complaints just like these that have been filed against Lockhart Morris and Montgomery. And if you think that the company may be violating your rights, you should reach out to a reputable consumer advocate for help.

When debt collectors are operating under a revenue crunch or an overly aggressive collection quota, it can be tempting to cut corners and ignore consumers’ rights in the process. But this type of behavior is against the law. And if Lockhart Morris and Montgomery has a history of ignoring your rights, that may be a sign that the company is operating outside of legal boundaries.

Federal Court Judgments Reveal FDCPA Violations

The fact that Lockhart Morris and Montgomery has a history of violating consumers’ rights isn’t just an accusation. It’s a fact. And the proof is in the pudding.

In Holmes v. Lockhart Morris Montgomery Inc. (Case No. 3:2010cv00040), U.S. District Court for the Northern District of Indiana entered a judgment against Lockhart Morris and Montgomery on Sept. 14, 2010. Judge Theresa L. Springmann ordered Lockhart Morris and Montgomery to pay the plaintiff a total of $3,080, which included $1,000 in statutory damages for violating the Fair Debt Collection Practices Act (FDCPA); $1,665 in attorney fees; and $415 in filing and service fees.

The judgment was the result of a default because Lockhart Morris and Montgomery failed to respond to allegations that it had engaged in illegal and harassing communication tactics.

Another case, Williams v. Lockhart Morris and Montgomery Inc., was settled in March 2021, approximately three weeks after the complaint was filed. It’s pretty clear that Lockhart Morris and Montgomery has a weakness for settling cases (and occasionally losing them). And if you have a skilled advocate in your corner, you may be able to use this knowledge to your advantage.

Documentation Failures Offer an Opportunity for Dispute

Debt Validation Issues

Failing to validate a debt is a violation of the FDCPA. And consumers have repeatedly accused Lockhart Morris and Montgomery of ignoring their requests for debt validation, which includes providing an original contract.

In a complaint filed with the BBB in June 2025, a consumer named Steven B wrote, “I am not liable for this debt and LMM will not be able to provide me with an original contract regarding any debt.”

Other consumers have filed similar complaints on Ripoff Report, accusing Lockhart Morris and Montgomery of attempting to collect “junk, old, unverified debt” in an effort to get consumers to pay debts they may not owe.

If the original creditor has written off your debt as a charge-off, that means the company has already accounted for the loss for tax and accounting purposes. So when a debt buyer like Lockhart Morris and Montgomery purchases that debt, it is literally buying a piece of paper. And that piece of paper may not include everything Lockhart Morris and Montgomery needs to prove that you actually owe the debt.

Credit Report Accuracy Issues

Lockhart Morris and Montgomery has also been accused of manipulating credit reports as a means to collect a debt. Specifically, the company has been accused of attempting to re-age debts that are beyond the statute of limitations by reporting the incorrect date of delinquency. This practice is a violation of the Fair Credit Reporting Act (FCRA), which says consumers have a right to accurate credit reports.

In September 2024, a consumer named Lauren S filed a complaint with the BBB against Lockhart Morris and Montgomery. She said the company had purchased a debt that she first became delinquent on in December 2017. In July 2024, which was six years and nine months after the first date of delinquency, Lockhart Morris and Montgomery attempted to add information to her credit report that claimed she became delinquent in May 2024. As a result, her credit score dropped by more than 50 points because of the “fraudulent information” Lockhart Morris and Montgomery was reporting.

Other consumers have filed similar complaints with the CFPB, including at least one who said Lockhart Morris and Montgomery attempted to add a medical debt to their credit report that they did not owe. The consumer said they had never lived in or conducted business in the state where the debt was allegedly incurred. Despite that, Lockhart Morris and Montgomery allegedly ignored the consumer when they disputed the debt.

Understanding Your Rights When Dealing with a Debt Collector

Harassment Isn’t an Option

The FDCPA says debt collectors can’t harass consumers or threaten them with arrest. Despite that, some consumers have accused Lockhart Morris and Montgomery of engaging in those exact practices.

A consumer filed a complaint on Ripoff Report, saying Lockhart Morris and Montgomery was threatening them along with their daughter. The consumer self-identified as an “elderly disabled lady in a wheelchair.”

Another Ripoff Report complaint accused the company of harassing “deployed military members overseas and their families here in the [United States].” The consumer also accused Lockhart Morris and Montgomery of placing “false information on credit reports” and using “extortion to collect debts.”

Someone identified as “Caylee” posted on the CreditBoards forum about a collections call she received from Lockhart Morris and Montgomery. The caller claimed to be representing Chase bank and threatened to sue her for fraud related to a credit card account she stopped paying in 2004.

State and Federal Exemptions You Should Know About

Consumers have more rights than they think when it comes to dealing with debt collectors. For example, state and federal law exempt some income and assets from garnishment. In most cases, a debt collector can’t touch your Social Security benefits, disability benefits or your retirement account, regardless of what they might be threatening you with.

In addition, there is a statute of limitations on debt. And once it runs out, a debt collector can no longer sue you over the debt. Lockhart Morris and Montgomery has been accused of attempting to collect debts that are beyond the statute of limitations, which could be a violation of state consumer protection laws.

It’s always important to understand your rights as a consumer. And when you’re dealing with an aggressive debt collector like Lockhart Morris and Montgomery, it’s even more important. That’s because Lockhart Morris and Montgomery is hoping you don’t know your rights and that you won’t put up a fight.

But if you do put up a fight and force Lockhart Morris and Montgomery to follow the law, you could be surprised at how quickly the company backs down. So don’t let Lockhart Morris and Montgomery push you around. If you don’t already know your rights, it’s time to get up to speed. And if you do know your rights, it’s time to start enforcing them.

The Dispute-First Approach to Lockhart Morris and Montgomery

Why You Shouldn’t Pay a Collection Account

Many consumers think that the best way to deal with a collection account is to simply pay what they owe and move on with their lives. But this could actually do more harm than good.

For example, simply paying a collection account will not remove it from your credit report. Instead, it will just show as a paid collection, which will remain on your credit report for seven years from the original delinquency date.

In some states, paying a collection account can also restart the clock on the statute of limitations, giving a debt collector additional time to sue you for the debt. In addition, if you make a partial payment on a debt you don’t think you owe, the debt collector may consider that payment to be a tacit acknowledgement that you actually do owe the full amount.

So why on earth would you pay a debt like that? Instead of paying Lockhart Morris and Montgomery, you may be able to dispute the debt and have it removed altogether. And if Lockhart Morris and Montgomery has a history of failing to validate its debts or accurately report consumer credit information, that could be the exact ammunition you need to successfully dispute the account and have it removed from your credit report.

How a Professional Advocate Can Help

If you’re dealing with a collection account from Lockhart Morris and Montgomery or a similar debt collector, you should consider reaching out to a professional advocate for help.

Consumers who try to deal with collection accounts on their own often find themselves in over their heads. That’s because debt collection is a tricky business that’s full of nuances and loopholes that the average consumer may not understand. As a result, consumers who try to navigate the system on their own may find themselves getting the runaround from debt collectors who do this sort of thing for a living.

But when you have a professional advocate in your corner, you can level the playing field. That’s because professional advocates understand how the system works. They know all the tricks and loopholes that debt collectors use to get what they want. And they know how to use that knowledge to your advantage in a dispute.

For example, if Lockhart Morris and Montgomery has a history of failing to validate its debts or accurately report credit information, a professional advocate can use that to your advantage in a dispute. The advocate can help you craft a customized dispute letter that identifies the weaknesses in Lockhart Morris and Montgomery’s position and uses those weaknesses to your advantage.

And if Lockhart Morris and Montgomery can’t verify the debt and its accuracy within a reasonable amount of time, it may be required to remove the account from your credit report altogether. That isn’t a technicality or a loophole. Instead, it’s a consumer protection that’s built into federal law. And when you have a professional advocate helping guide you through the process, you can use that protection to your advantage and get the outcome you deserve.

Conclusion

Lockhart Morris and Montgomery has a history of violating consumer rights, which could be a problem if the company is attempting to collect a debt from you. Whether it’s accusing the company of failing to validate debts or manipulate credit reports, hundreds of consumers have filed complaints against Lockhart Morris and Montgomery. And in at least one case, a judge has ruled against the company and ordered it to pay damages for violating the FDCPA.

So what does that mean for you? If Lockhart Morris and Montgomery is on your credit report, you shouldn’t try to hide or ignore the problem. Instead, you should consider disputing the account directly. And if you’re not sure where to start, that’s OK. You don’t have to do this alone.

With help from a professional advocate, you could be surprised at how quickly you’re able to resolve the issue and move on with your life. After all, you don’t have to pay a collection account just to have it remain on your credit report. Instead, you may be able to have it completely removed without paying a dime. And that isn’t a long shot.

On the contrary, it’s a common outcome when consumers dispute a collection account from a company like Lockhart Morris and Montgomery that has a history of violating their rights.

So don’t wait any longer. It’s time to take action and start enforcing your rights as a consumer.

If Lockhart Morris and Montgomery is on your credit report, don’t make any rash decisions. Don’t call the company and don’t make a payment on the debt in hopes that it will go away. In fact, that’s likely to make the problem worse instead of better.

Instead, contact the advocates at FightCollections.com for a free consultation. We can help you identify whether you have grounds for a dispute based on Lockhart Morris and Montgomery’s history of violating consumer rights. And if so, we can help you craft a customized dispute letter to send to the credit reporting agency.

Don’t let Lockhart Morris and Montgomery push you around and violate your rights. Instead, let us help you fight back. Contact us today to connect with an advocate who can help.