Imagine logging in to check your credit report and seeing a name you don’t recognize. There’s an entry from Midland Credit Management saying you owe them money, except the debt is not one you are aware of. Your heart sinks.

This is the story of millions of people every year. Midland Credit Management is a debt buyer. That means they purchase debts from the original creditor for mere pennies on the dollar and then try to collect the full amount from you. In fact, According to the Consumer Financial Protection Bureau, Midland’s parent company paid just three cents on the dollar for the debts it purchased.

Before you jump into a panic and reach for your checkbook, realize this important fact: Paying off a collection account does not get it removed from your credit report; it merely changes status to "paid" and the negative entry still stays on your report for up to seven years. There’s a better way to deal with it. But first, you need to know who you’re dealing with.

Who is Midland Credit Management?

Midland Credit Management is the largest debt collection company in the country. Here’s their essential contact information:

A History of Regulatory Penalties

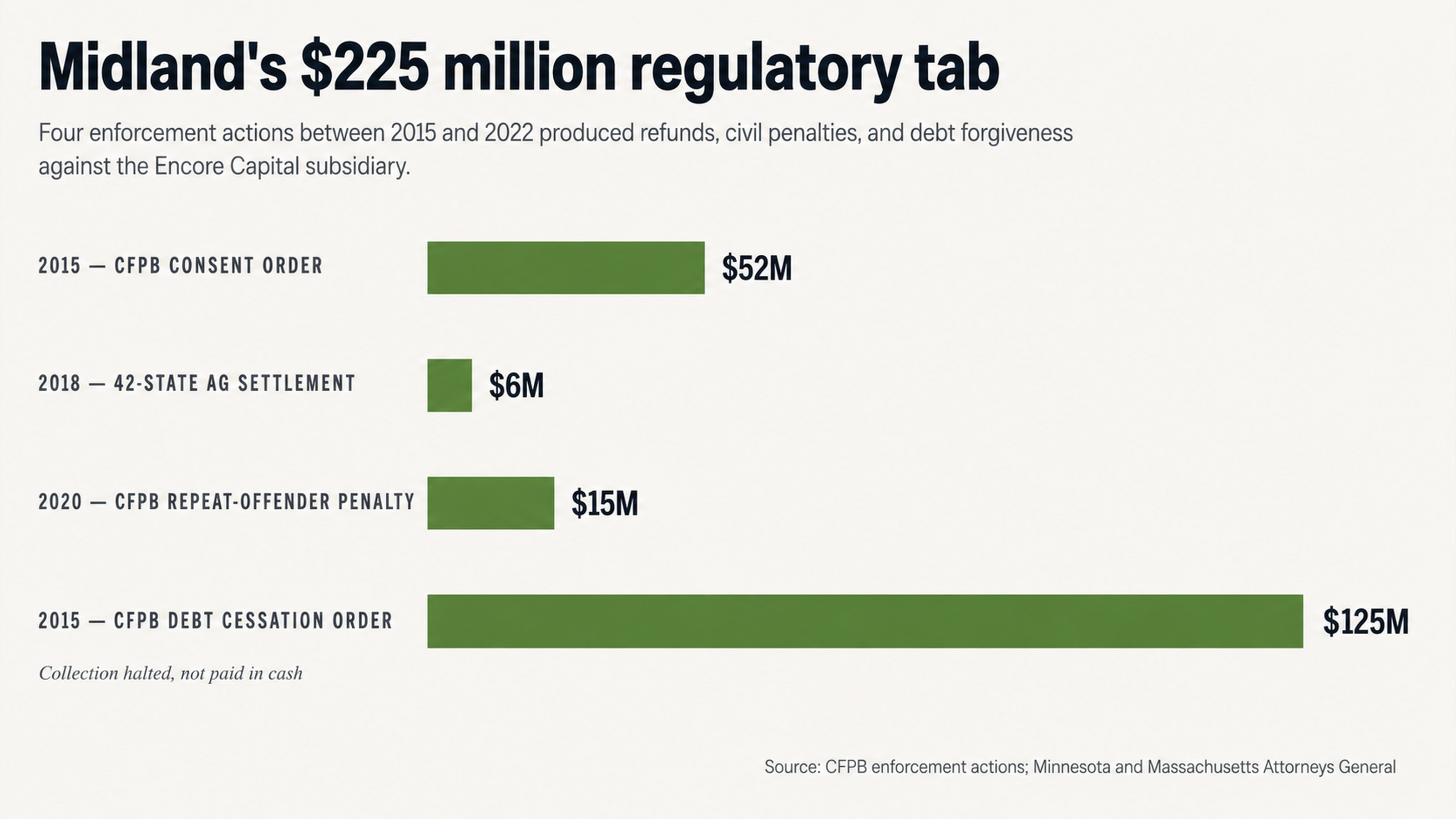

Despite its A+ rating from the Better Business Bureau, Midland Credit Management has one of the longest records of regulatory penalties in the industry. Altogether, enforcement actions have resulted in more than $225 million in penalties, settlements, and debt relief. The company has faced enforcement action from the Consumer Financial Protection Bureau, enforcement action from 42 state attorneys general, and multiple class action lawsuits.

In September 2015, a CFPB consent order required the company to provide up to $42 million in consumer refunds, pay a $10 million civil penalty, and stop collecting on $125 million in debts. But in 2020, the CFPB sued the company again for violating the consent order. The result? An additional $15 million civil penalty.

In 2018, a settlement with 42 state attorneys general added another $6 million in penalties.

Consumers’ reviews tell a similar story. The company has had more than 1,000 complaints filed with the BBB in just three years. At Trustpilot, 93% of reviews are one-star. These numbers indicate that despite the oversight, the practices continue.

Why You Should Dispute Before You Pay

The Reality of Error Rates

Credit reports are not nearly as accurate as you might think. In fact, a study by U.S. PIRG found that 79% of credit reports contain some mistake or serious error. This could be something as simple as a misspelled name or as egregious as a stranger’s account showing up on your report.

But when it comes to Midland, the issue is even worse. CFPB consent order findings said that the purchase agreements between the original creditors and Midland’s parent company include language that says account documentation will be provided “if available.” In some cases, the agreement actually says, “No documentation is available.”

The original creditors do not verify that the amount is correct or that the debt is legally enforceable before they sell.

This means that Midland routinely tries to collect from consumers on debts for which the company does not have the original contract, statements, or any proof of obligation. If there is one collection account on your report with an error, that’s a red flag that you should go through your report with a fine-tooth comb to find other potential problems. The lack of verification that plagues one account likely plagues others, too.

Systemic Documentation Issues

Court records show that there were systemic problems with the way Midland handled legal documentation. Employees testified in regulatory cases that they signed between 200 and 400 computer-generated affidavits every day. They never read them. They never verified their accuracy. And they had no personal knowledge of the accounts in question.

Despite this, the affidavits claimed that the signers had personal knowledge of debt information. When a legal specialist testified, she could not even define some basic legal terms or explain the assignments of debt she was testifying about. Employees signed documents before any supporting materials were attached.

In 2009 alone, the Minnesota Attorney General found that the company filed 245,000 lawsuits across the country. As part of a settlement with the New York Attorney General, the company had to vacate more than 4,500 judgments that were improperly obtained. Those judgments were worth nearly $18 million.

These numbers suggest that when consumers challenge debts, the collection company often cannot produce the proper documentation.

Understanding Debt Collection Tactics

Urgency and Intimidation

Debt collection agencies have an information advantage. They know that most people are embarrassed about debt. They know that consumers are not aware of their rights. And they know that consumers want the situation to go away as quickly and quietly as possible.

Every phone call, every letter, and every voicemail is designed to play on those feelings.

The Massachusetts Attorney General cited illegal calling practices in a 2022 settlement. The company made up to 15 calls in a seven-day period to individual consumers. That exceeds the two-call limit under Massachusetts regulations. The settlement also said the company targeted consumers with income from Social Security and pensions, despite the fact that income from those sources cannot be garnished.

The AG said the company falsely represented that these consumers “were obligated to pay debts when, in fact, the consumers’ income was exempt from garnishment.”

This calling creates a sense of urgency. It’s meant to scare you into action. Every question a debt collector asks is designed to give them more ammunition against you. If you confirm your address, your employer, or your bank, you are giving them information they can use against you.

Don’t feel like you’re being rude or uncooperative by not answering questions. You’re being strategic.

Third-Party Contacts

One tactic that consumers find particularly offensive is when debt collectors call their family members under the guise of something else to alarm them.

“I had Midland Credit call my granddaughter to ask if I was her emergency contact,” one consumer reported. “She immediately went into panic mode thinking something had happened to me. Then she realized it was a collections call for me.”

These calls are embarrassing. They’re designed to create social pressure for you to pay your debt. But they also illustrate why you should not volunteer information. And why you should not let your family volunteer information either. Every time you answer a question, you’re providing the debt collector with another tool to use against you.

The Dispute Process

How Disputes Work

The Fair Credit Reporting Act guarantees you the right to dispute any information on your credit report that is inaccurate, incomplete, or unverifiable. When you initiate a dispute, the credit reporting bureau has 30 days to investigate. It will contact the entity that reported the information to your report and ask it to verify the debt.

Here’s where Midland’s documentation issues can become your gain. If the collection agency cannot verify the debt and provide proper documentation within the allotted time, the credit bureau must delete the item from your report.

Given the volume of accounts these collection agencies handle and the fact that they do not have the documentation to back most debts, many consumers have success simply because the verification cannot be done.

Individual lawsuits illustrate this point, too. In the case Brim v. Midland Credit Management, a federal jury awarded $723,180 — including $623,180 in punitive damages — after it found that the company failed to adequately investigate a consumer’s dispute.

The company’s argument was that it was only required to verify the debt using its own electronic records. It said it was not required to investigate whether the underlying information was actually accurate.

Why Consumer-Initiated Disputes Fail

While it is technically possible to dispute items on your credit report yourself, it is a process that requires specialized knowledge of the legal technicalities, the right documentation, and the right timing.

Credit repair is not a sprint. It’s a marathon. The seven-year period that most collections can stay on your report — and the 30-day window for investigation — means that patience and persistence are likely to get you a lot further than a frantic effort to fix everything right now.

Collectors are repeat players in the credit repair process. They understand the system. They know the loopholes and the shortcuts. Most consumers will dispute an item once, get a form letter in response, and throw in the towel. Professionals understand that the initial dispute is often just the first step in a process that may require escalation and sometimes even legal action.

And the information asymmetry that works in the debt collector’s favor in almost every interaction also works in the collector’s favor when it comes to the dispute process itself. Understanding which arguments to make, which documentation to request, and which regulatory agency to turn to requires expertise that the average consumer simply doesn’t have.

What It Takes to Get a Successful Removal

Grounds for Removal

A collection can be removed from your credit report if the information is incorrect, a mistake, fraudulent, or if it cannot be verified within a reasonable amount of time. Given Midland’s documented history of collecting debts without the proper documentation, many of the accounts the company reports are vulnerable for removal.

Common problems include incorrect account balances, the wrong date of first delinquency, accounts that belong to someone else entirely, debts for which the statute of limitations has run out, and accounts where the collector cannot produce a copy of a signed agreement or a complete payment history.

The CFPB found that Midland placed more than 100,000 accounts with law firms that employed a total of just 16 attorneys — a caseload that made it impossible to conduct any sort of meaningful review of each individual case.

When consumers contested lawsuits and the company could not find documentation, the internal policy was to attempt to settle before dismissing the case rather than taking the consumer to court.

That illustrates an essential point: When you challenge a debt collector, the company will often back down rather than produce documentation it does not have.

The Value of Professional Help

Credit repair requires professionals understand the technical and legal requirements that debt collectors must meet when they respond to a dispute. They can spot when a verification response is not legally adequate — even when it might look that way to the naked eye. They can tell when the statute of limitations has expired and when a collector is trying to re-age a debt to keep collecting.

And they understand when a debt collector is violating your rights.

When you work with a professional, you also create a paper trail of your efforts to repair your credit. If a debt collector continues to report a debt after failing to verify it — or uses illegal tactics to try to collect it — having a professional record of your interactions with the company may provide essential evidence if you decide to pursue legal action.

Jury verdicts like the $723,000 award in Brim v. Midland Credit Management demonstrate that the courts take these violations seriously.

The cost of hiring professional help is typically a fraction of the long-term financial consequences of a damaged credit score. Higher interest rates on your mortgage, your car loan, and your credit cards can cost you tens of thousands of dollars over the life of the loan.

So can higher insurance premiums. A negative credit report can even affect rental applications and employment decisions.

Next Steps

What to Do First

If you see Midland Credit Management on your credit report, do not call the company. Do not pay it. Do not confirm your identity, your address, or any details about the alleged debt. Do not assume you owe the debt just because some company says you do. This is a company that has paid more than $225 million in regulatory penalties for illegal collection practices.

Instead, order copies of your complete credit reports from all three bureaus. Go through them carefully. Look for any other accounts you do not recognize or any other information that is not accurate.

If one collection account on your report has a problem, there may be others.

Document everything. Keep any letters you get in the mail. Note the dates and times of any phone calls. Having a record of what’s happening can be essential if you need to show a pattern of harassment or pursue legal action.

Getting Professional Help

At CollectionsRelief.com, we specialize in removing erroneous collection accounts from credit reports and holding debt collectors accountable for their illegal practices.

Our team understands the specific tactics debt buying agencies like Midland use. We understand the legal technicalities they must meet. And we know how to force debt collectors to follow the law.

We’ll review your credit reports for you to identify any accounts that may be eligible for removal. We will handle the dispute process on your behalf. We’ll understand which arguments to make and which documentation to request. And we’ll understand when to escalate and how.

Debt collectors are repeat players in this game. They do this all day, every day. You shouldn’t have to go up against them alone. And you shouldn’t let a debt collector with a documented history of violations mess up your credit report without a fight.

Contact us today for a free consultation. Let us review your situation and talk to you about your options.