If you see Mountain Land Collections on your credit report, you aren’t alone. As a debt collection agency out of Utah, Mountain Land Collections has been around for over 30 years.

It can be daunting to find this collection agency on your report, but there is something that Mountain Land Collections doesn’t want you to know. You have more power over this agency than you think.

What Mountain Land Collections Doesn’t Want You to Know

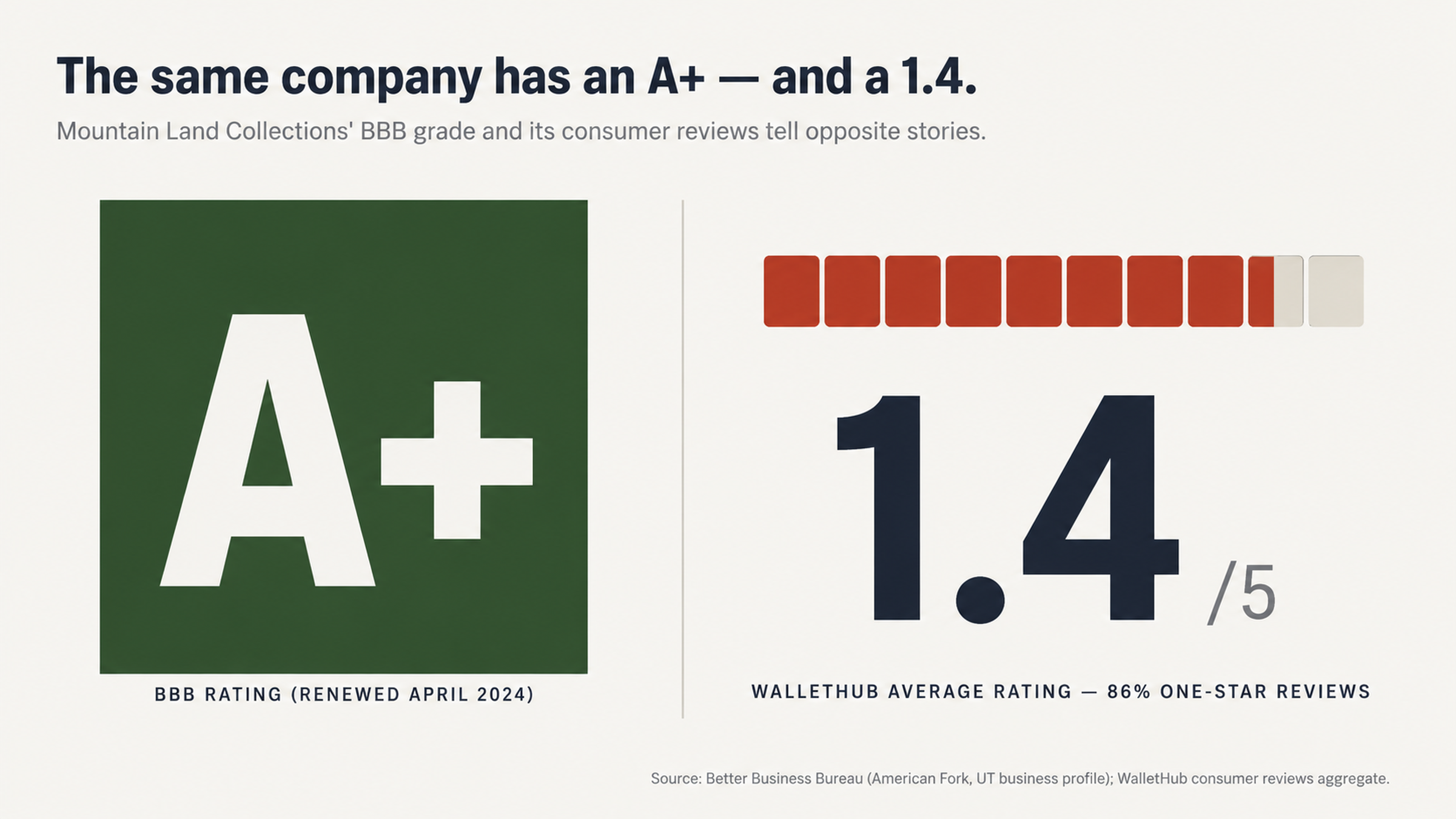

Mountain Land Collections has an A+ rating with the Better Business Bureau, which was most recently renewed in April 2024. But on WalletHub, they have an average rating of 1.4 out of 5 stars. 86 percent of all reviews of Mountain Land Collections are one-star.

In the CFPB Consumer Complaint Database, there are over 70 complaints about this company, including allegations of attempting to collect debts not owed and misrepresenting credit information. In 2019 alone, Mountain Land Collections was the 897th most complained about financial company.

A huge discrepancy exists between their official ratings and actual consumer experience. The fact that Mountain Land Collections has an A+ rating with the Better Business Bureau despite so many negative reviews on other platforms is a testament to how the system doesn’t work for you. It works for them.

What Collection Agencies Don’t Want You to Understand About Credit Reporting

The Truth About Credit Reporting

In one of the most sweeping exposes on credit reporting, the U.S. PIRGs concluded that 79 percent of credit reports contain some type of mistake or serious error. That’s not a typo. Almost four of five credit reports have some type of error.

That means that when you see a collection account on your credit report, there is almost an 80 percent chance that something is wrong. Either the amount is incorrect, the dates are wrong, the account belongs to someone else, or (as is frequently alleged against Mountain Land Collections) the debt has already been paid.

Your legal right to request a free annual credit report from AnnualCreditReport.com isn’t just a right. It’s a tool. Requesting your credit report from each of the three major credit bureaus (Equifax, Experian, and Transunion) allows you to see exactly what’s being reported about you, identify discrepancies between credit bureaus, and find inaccuracies you can dispute.

Why Ignoring the Collection Agency is Your Best Move

Why Collection Agencies Need You to Call Them Back

There’s a reason why collection agencies make so many phone calls and send so many letters. They need you to call them back. Every minute a collection agency spends on your account costs them money. They operate on thin margins and need to resolve accounts quickly to maximize profits.

When you engage emotionally with a debt collector, they know they have you right where they want you. But if you refuse to engage directly with the collection agency and only communicate with them through formal dispute processes, you put them in the position of having to prove their case. You aren’t obligated to prove anything.

Mountain Land Collections’ Known Issues

Collecting on Debts Already Paid

Far and away the biggest complaint about Mountain Land Collections is that they attempt to collect debts that consumers have already paid. This isn’t just a suspicion. It’s a documented pattern.

In May of 2017, a consumer contacted the CFPB after Mountain Land Collections attempted to collect an $800 medical bill from an auto accident even though the other driver’s insurance company had paid all medical bills. Despite providing documentation, including a copy of the canceled check and contact information for the insurance company, Mountain Land Collections demanded payment and placed a negative mark on the consumer’s credit report.

As a result, the consumer couldn’t qualify for a mortgage until the item was removed after a complaint was filed with the Better Business Bureau.

As recently as April of 2025, consumers are still reporting the same issue. One consumer alleged that Mountain Land Collections contacted them about a three-year-old debt even though they had paid “100 percent of my hospital bills,” met their insurance deductible, and confirmed with the hospital that they owed nothing.

One consumer review put it succinctly, “They want to double dip. They will try to collect on your account a second time even after the first balance has been paid off. If you cannot produce the paperwork, they will accuse you of not paying it off the first time.”

Selectively Reporting Information to Credit Bureaus

Perhaps more insidious than attempting to collect on debts already paid is how Mountain Land Collections reports information to credit bureaus. There are several documented cases of Mountain Land Collections aggressively reporting negative information but refusing to update credit reports when consumers make payments.

One consumer reported in October of 2025 that “Every two weeks, [MLC] is reporting to the credit bureau that I owe $1.50 more in interest. This has caused my credit score to plummet. However, when I made payments, not once did [MLC] report to the credit bureau that I was making payments or that my balance was decreased.”

This type of selective credit reporting is a way of maximizing the damage to a consumer’s credit score while minimizing the benefit of attempting to pay the debt.

Your Rights and Advantages

The Seven-Year Clock is in Your Control

One of the basic facts about collection accounts is that they can only remain on your credit report for seven years from the original date of delinquency. This is a federal regulation that no collection agency can get around, no matter how many times they update a collection or sell it to another agency.

What this means is that depending on how old your debt is, you may be much closer to the end of the seven-year period than you think.

Furthermore, if you are able to successfully dispute a collection and have it removed from your credit report before the seven-year period is over, collection agencies typically do not have the ability to report it again. Once a collection is removed, it usually stays removed.

Understanding how old your debt is and how much longer it has before it is supposed to fall off your report is one of the most powerful pieces of information you can have if you are facing collection accounts on your credit report.

Rights You Never Knew You Had

Collection agencies make a lot of threats about what will happen if you don’t pay a debt. Frequently, these threats involve wage garnishment or even having your retirement accounts seized. But in almost all cases, consumers have more protections than they realize.

For example, both federal and state laws exempt almost all types of income from garnishment proceedings. One consumer filed a complaint against Mountain Land Collections in June of 2025 after they had their wages garnished and their retirement account seized. But experiences like this are rare, particularly if consumers understand their rights and take advantage of them early in the process.

Federal laws like the Fair Debt Collection Practices Act and the Fair Credit Reporting Act, along with state-level consumer protection laws, provide a framework of rights that few consumers ever fully utilize. When consumers understand what collection agencies can and cannot do, the imbalance of power in the relationship begins to shift.

Disputing a Collection Account Before Paying

Why Paying a Collection Account Often Hurts More than Helps

Your initial reaction upon seeing a collection account on your credit report might be to pay it off as soon as possible to make it go away. But in almost every case, paying a collection account is the worst thing you can do.

When you pay a collection account, its status is updated from “unpaid collection” to "paid collection." But in either case, the collection account remains on your credit report. To most lenders, a paid collection and an unpaid collection are treated the same way.

In some cases, paying a collection account can even have the effect of restarting the statute of limitations on the debt or resetting the clock on when the debt is eligible to be removed from your report. Paying a collection account can even serve to validate the debt so that it is no longer eligible for dispute. Paying a collection account is often the single worst move you can make as a consumer.

What Happens When a Collection Agency Can’t Verify a Debt

If you dispute a debt through the proper procedure, federal law requires collection agencies and credit bureaus to investigate and verify the information they are reporting. If they cannot verify the debt within a reasonable amount of time, they must remove the item from your credit report.

This is one of the most powerful tools consumers have when facing a debt they don’t think they owe. Mountain Land Collections, like almost every other debt collection agency, frequently doesn’t have all the documentation they need to verify the accounts they are collecting.

This is particularly true of medical debt, which may change hands several times and have gaps in its documentation at each transfer point.

If you dispute a debt properly and with the right documentation, the burden is on the collection agency to prove their case. In many instances, they are unable to do so, and the debt is removed not because the consumer “won” an argument but because the collection agency failed to meet their burden of proof.

In response to consumer complaints, Mountain Land Collections has been known to dismiss disputes as “form complaints taken from the internet” and argue that because they are a third-party debt collection agency, they do not have the same documentation burden as original creditors.

Instead of engaging with the substance of a consumer’s allegations, Mountain Land Collections has a history of responding with boilerplate language, which can sometimes make it easier for consumers to have debts removed through the dispute process.

Take Control of Your Credit Report With Help From a Pro

Mountain Land Collections has been named as a defendant in at least three federal lawsuits alleging violations of the Fair Debt Collection Practices Act. They have generated over 70 complaints to the Consumer Financial Protection Bureau. Their consumer reviews document a pattern of attempting to collect debts already paid and selectively reporting information to credit bureaus to maximize damage to consumers.

But here is the most important fact. None of this means you have to live with Mountain Land Collections on your credit report. You can get a collection removed from your credit report if the information is inaccurate, erroneous, fraudulent, or if the collector can’t verify it within a reasonable amount of time.

Given the extraordinarily high error rate of credit reports and the specific patterns of abuse that consumers have reported with Mountain Land Collections, there may be grounds for removing their collections from your credit report.

But should you try to do it yourself or get professional help? Consumers who attempt to navigate the dispute process on their own can make procedural mistakes that compromise their effort. They may inadvertently validate a debt, restart a statute of limitations clock, or simply fail to document their dispute in a way that forces the issue.

Working with a professional credit repair agency that understands the dispute process, knows what the law requires of collectors, and can identify the soft spots in how a debt is being reported can make all the difference. Instead of operating from a position of information asymmetry where the collector has more knowledge than you, you can work with experienced advocates who understand how the system works.

If Mountain Land Collections is on your credit report, don’t panic and don’t pay them. Instead, gather your documents, request a copy of your free credit report from all three bureaus, and consider whether working with a professional might just be the difference maker that gets Mountain Land Collections off your credit report for good.

FightCollections.com specializes in disputing collection accounts and helping consumers understand their rights. Contact us today for a free consultation to talk about your situation and see what we can do to help.