Are you seeing MRS BPO LLC on your credit report? Are you wondering who they are and how they got there?

It makes sense. Finding a mysterious debt on your credit report can feel like finding a stranger living in your basement. You didn’t invite them to move in, and you have no idea why they’re there. The only difference is, instead of sending them packing, you’re being told you owe them money.

In the debt collection industry, it’s all about knowledge. The debt collectors know their business. But most people don’t know anything about the process. The rest of this article will change that. Let’s explore who MRS BPO LLC is, why they’re calling you, and how you can get them out of your life.

Who is MRS BPO LLC?

MRS BPO LLC is a third-party debt collection agency headquartered in Cherry Hill, New Jersey. They have call centers in New Jersey, Ohio, Alabama, and Mumbai, India. According to their website, MRS BPO has between 500-1,000 employees. They collect debts on behalf of companies like Spectrum, PayPal, Chase Bank, Verizon, and PSEG.

What are they accused of doing?

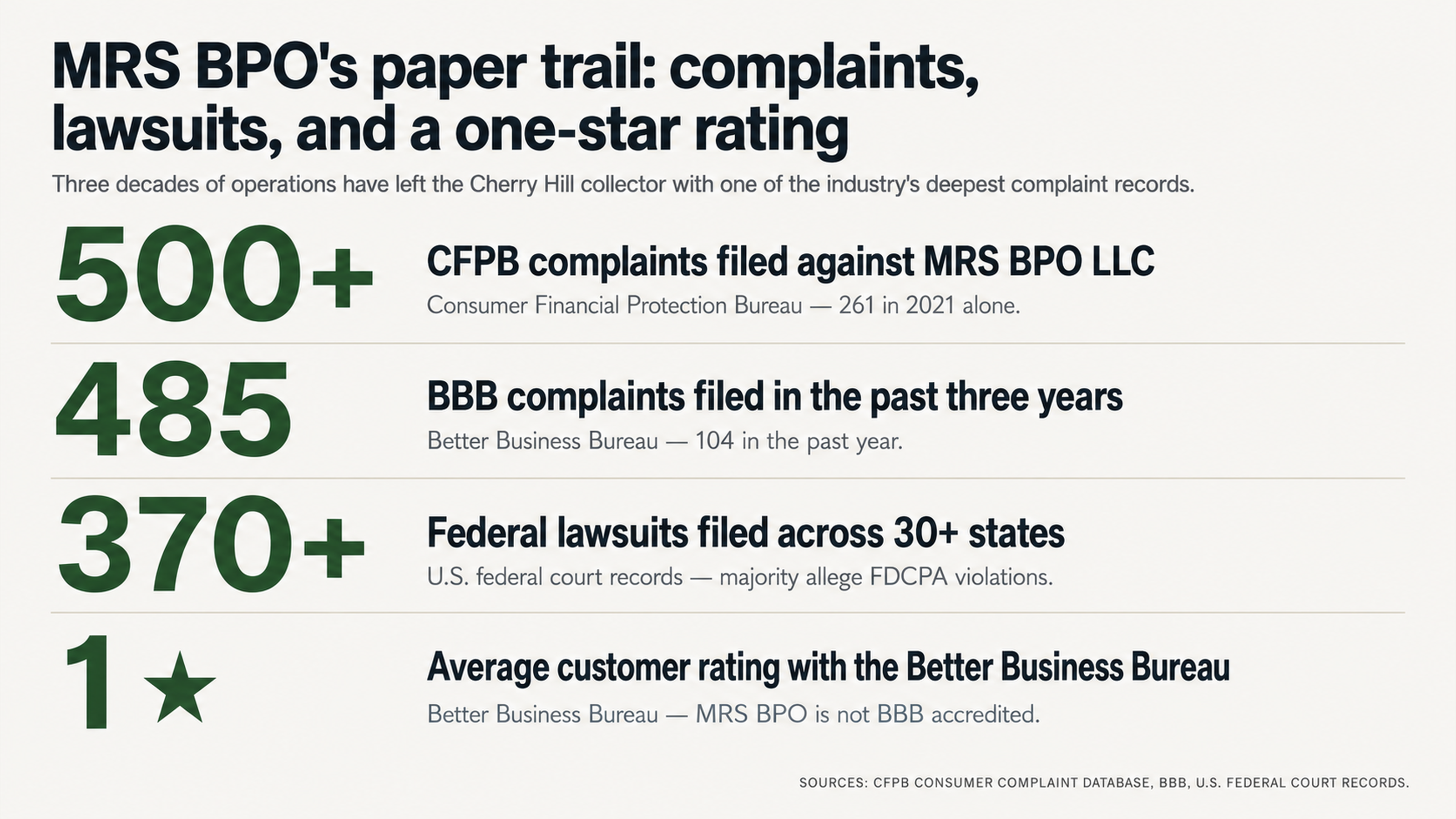

Even though they’ve been around for 34 years, MRS BPO has gained a reputation for their questionable collection practices. They’ve had over 500 complaints filed with the Consumer Financial Protection Bureau, with 261 complaints filed in 2021 alone. They also have 485 complaints registered with the Better Business Bureau in the last three years alone, including 104 complaints in the past year. Their average rating with the BBB is 1 star, and they’re not accredited by the organization.

There are even more examples of their terrible service on review sites. One customer wrote, “I have never had a Spectrum account. I have lived in the same house for 18 years and we STILL CAN NOT GET INTERNET where I live. Spectrum stops 5 miles up the road.”

Over 370 lawsuits have been filed against them in federal court across more than 30 states. The majority of the suits involved FDCPA violations. Some court decisions reveal MRS BPO’s business practices more clearly.

In DiNaples v. MRS BPO LLC, the Third Circuit Court of Appeals ruled against MRS for printing QR codes on the outside of collection envelopes. The codes displayed the debtor’s account number when scanned with a smartphone. The court noted that, “Any teenager with a smartphone app could have scanned the QR code and obtained Ms. DiNaples’ account number.”

How does MRS BPO work?

It’s helpful to understand how a debt collection agency makes its money. This will help you understand their weaknesses.

MRS BPO primarily works as a third-party debt collector. This means they don’t buy debts from the original creditor. Instead, they’re hired to collect debts on behalf of the creditor. Their fee is usually a percentage of what they recover.

The problem with this system is it incentivizes debt collection agencies to move quickly and make as many phone calls as possible. It’s not in their best interest to spend hours verifying your debt. They have to balance the cost of their time with the debt’s potential reward. If they have to spend $500 to validate a $300 debt, they’re going to lose money on the deal.

So, if you understand the economics of debt collection, you can use it to your advantage.

What tactics do they use?

Debt collection agencies are notorious for their high volume of phone calls, emails, and letters. MRS BPO is no exception. One CFPB complaint mentions 43 phone calls from the company. Another complaint mentions five or more phone calls a day from different phone numbers.

They also play on your sense of urgency and fear. One complaint mentions a representative threatening to send the police to the consumer’s workplace to arrest her if the receptionist didn’t hand over the phone. Needless to say, this is against the law.

Why Do Errors on Your Credit Report Work in Your Favor?

One of the primary reasons it’s hard to fight debt collectors is that most credit reports contain errors. According to a study done by U.S. PIRGs, 79% of credit reports contain either errors or serious errors. When debts are transferred from the original creditor to a third-party debt collector and finally to the credit reporting agencies, something inevitably gets lost in the shuffle.

Why are credit report errors so common?

The most common complaint filed with the CFPB against MRS BPO was “Attempted to collect wrong amount.” Many consumers reported being contacted for debts owed by different people, debts that had already been paid, or debts that didn’t exist at all.

One BBB reviewer described her experience with MRS BPO, “This company will wait several months and use updated information they received on you during the dispute to have the claim placed back on your report. They’d lie and say they’ve been in contact with you regarding the money owed to Spectrum when in fact you’ll never receive anything from them until they got your information from the dispute.”

In this case, the customer had lived in the same house for 18 years and never had internet service because it wasn’t available in her area. When debt collectors pursue consumers for services they couldn’t possibly have used, you know they’re not doing their due diligence.

How Does the Law Protect You?

Fortunately, federal law gives you tools to fight back against MRS BPO and other debt collectors. Under the FCRA,credit reporting agencies have 30 days to investigate any disputed items on your report. If they can’t verify the information, they have to remove it from your report. The FDCPA forces debtcollectors to verify your debt when you request it and forbids certain practices that are deceptive or unfair.

A recent court decision shows just how effective these laws can be. In Holt v. MRS BPO, L.L.C., a federal judge in the Northern District of Illinois found that MRS BPO had engaged in “a pattern of bad faith and intentional misconduct” when they withheld evidence during discovery. In another case, the company was found to have printed a QR code on the outside of a collection envelope that displayed the debtor’s account number when scanned with a smartphone.

Why Should You Avoid Paying Them?

Many consumers want to pay off debts when they see them on their reports. It’s understandable. You want the problem to go away. But paying them might not be the best course of action.

When you pay a collection agency, you're updating the status of the account from “unpaid collection” to “paid collection.” The account can still remain on your report for seven years from the date you first missed a payment. Paying them also restarts the clock on the statute of limitations for the debt. If you dispute the debt first, you force them to verify the debt.

Why Should You Hire a Professional Credit Repair Agency?

If you’re dealing with a debt collection agency on your own, it can be a David and Goliath story. The debt collection agency has experience on their side. They know the laws and how to navigate the system.

That’s where credit repair agencies come in. Not only do they have the expertise you need to navigate the system, but they’re also not emotionally invested in the outcome. They can help you make rational decisions about your debt without clouding your judgment with emotions. If you’re dealing with MRS BPO and need help resolving the issue, consider contacting a credit repair agency.

What’s the Outcome?

MRS BPO is a legitimate debt collection agency that operates in a questionable industry. With over 500 CFPB complaints, 485 BBB complaints, 370+ federal lawsuits, and a federal court decision finding bad faith conduct, it’s not surprising they have an average customer review of 1 star.

Their business practices, including the tendency to report debts without notification and then re-report after disputes using updated customer information, demonstrate a pattern designed to grind consumers down. It’s not surprising they would pursue wrong-person debts and debts discharged in bankruptcy.

One documented case involved a consumer whose debts were discharged through Chapter 7 bankruptcy in January 2011. MRS began collection calls in March 2011, despite having pulled credit records that showed the bankruptcy discharge. The consumer ultimately paid $1,300 on a legally uncollectible debt simply to stop the harassment.

In their rush to collect, it appears they don’t verify much of anything before reaching out to consumers. If you’re facing a debt from MRS BPO, this creates an opportunity for you. If they can’t verify your debt, the law says they have to remove it from your report. If they’re violating FDCPA laws, you’ve got even more leverage. Don’t react. Instead, take action to protect your credit.

At FightCollections.com, we specialize in helping consumers fight debt collection agencies. If you have MRS BPO on your report, don’t assume the debt is valid just because it’s there. Don’t give them more information about you. Don’t make an emotional decision that might hurt your financial future.

Contact us today for a free consultation. We’ll review your situation and discuss your options for removal.