MSCB Inc. is a debt collection agency based in Tennessee that was founded in 1977. They collect medical debts from consumers all over the country for healthcare providers.

If you see them on your credit report, you are likely dealing with a company that has had several complaints filed against them. Here are the details on MSCB Inc.:

What’s Important to Know

If you have noticed MSCB Inc. on your credit report, there’s a good chance you have come across some less-than-stellar information about the company’s practices. Before you panic, however, it’s essential to understand your options.

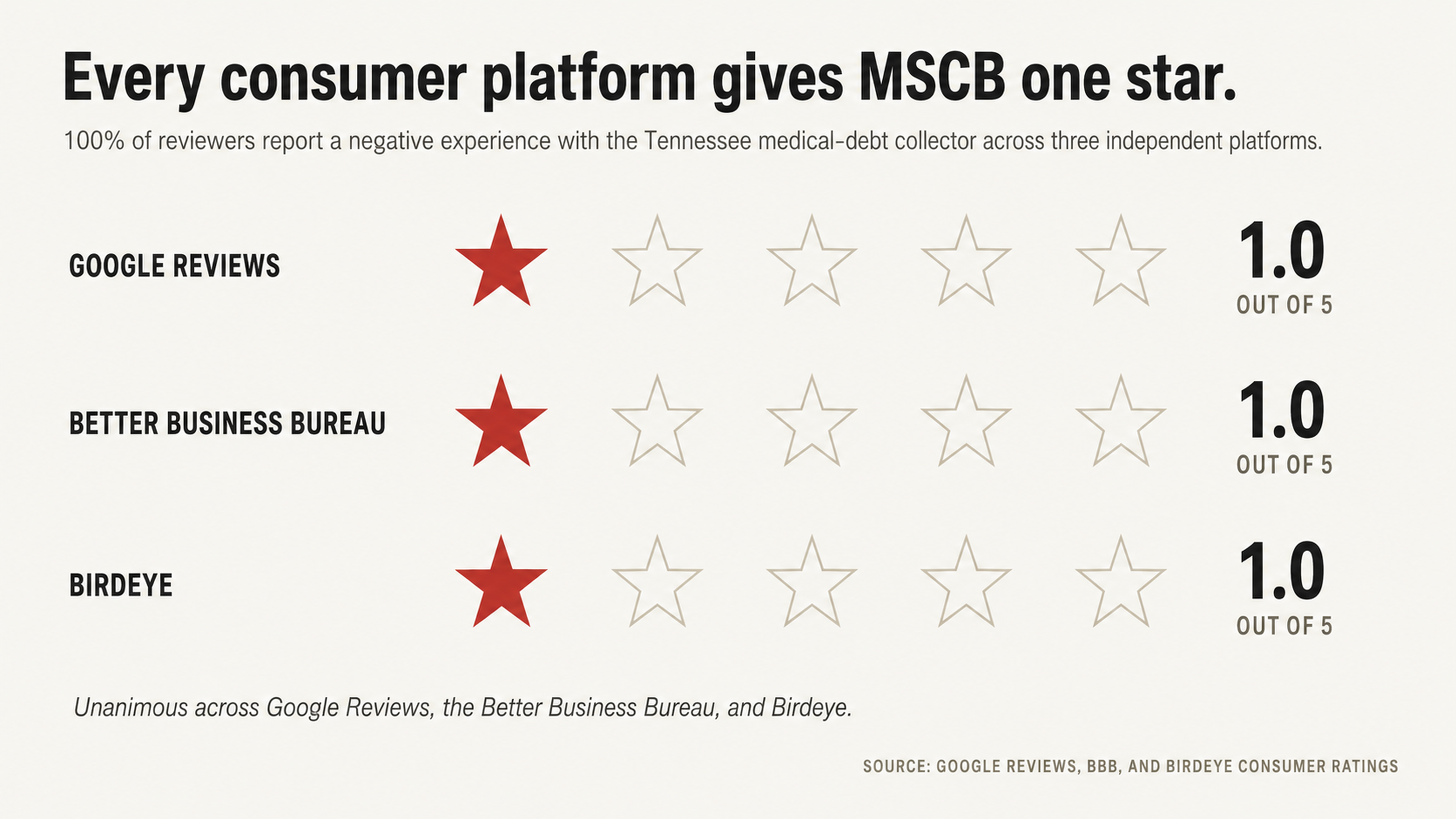

MSCB Inc. has a nearly perfect 1-star rating across Google Reviews, BBB customer reviews, and Birdeye. In fact, 100% of consumers report a negative experience with the company. There have also been 26 complaints registered with the Consumer Financial Protection Bureau (CFPB) against MSCB Inc. and at least four FDCPA lawsuits filed. (Ide v. MSCB Inc., Case No. 4: 17-cv-00823, settled in August 2018).

These numbers and cases are more than just statistics; they represent real consumers who felt compelled to file complaints or bring lawsuits against MSCB Inc. Here’s an example of one such experience:

“This company has keep [sic] call my wife claiming we owe money. They have never send [sic] a bill of proof. They have called us for about a year off and on. They were suppose [sic] to send us a proof of bill. We have never received it. They called her a liar.”

— BBB Complaint, June 2025

It’s not uncommon to find complaints about MSCB Inc. failing to provide debt validation.

Why You Are Seeing This on Your Report

Collection accounts on your credit report are there because of a very broken system. The credit reporting agencies receive information from data furnishers like MSCB Inc. and place it on your report without any real validation. In fact, a study by U.S. PIRGs found that 79% of credit reports contain errors or discrepancies. The goal of the credit reporting agencies is speed and quantity, not accuracy, and it’s up to consumers to correct errors.

When the original creditor decides a debt is uncollectible, they sell it to a collection agency for pennies on the dollar. Once they sell it, the original creditor is done. They’ve already written off the debt on their taxes and moved on. So, if you feel obligated to pay the original creditor for the services you received, that obligation is long gone.

MSCB Inc. primarily deals in medical debt. Medical billing is rife with errors, from charges for services you never received to duplicate charges to insurance payments applied incorrectly. The debt on your credit report may have originated as someone else’s clerical error that got out of control.

What’s Holding You Back

The simple fact is that collection agencies have more information and better tools at their disposal than you do. They have databases and skip tracing tools and legal resources that are not available to the typical consumer. They know how the system works because they work within it every day. You’re experiencing this situation once or twice in your life.

This disparity is why so many consumers feel intimidated when dealing with collection agencies. The agency knows exactly how much pressure to apply and how far they can go without crossing the line. They know most consumers will pay up eventually, just to make the phone calls stop, even if the debt is not valid.

The two primary weapons in any collection agency’s arsenal are urgency and fear. They will create a false sense of urgency. They will imply consequences that may not occur. They will rely on your unfamiliarity with the law. Education is a consumer’s best defense.

Why You Shouldn’t Pay First

The natural human instinct is to pay a collection agency to go away. Unfortunately, this is rarely your best option. When you pay a collection, you’re changing the status from “unpaid” to “paid,” but the derogatory mark remains on your credit report. You’ve confirmed the debt was yours. You’ve given up all your leverage. And, you still have the negative mark for up to 7 years.

Collection agencies will almost always refuse a goodwill letter asking for account deletion after paying the debt. Once they have your money, they don’t have any incentive to help you. You’ve provided them with the proof they need to verify the account if you dispute it later. You’ve armed your enemy against yourself.

The best approach is always to challenge first and only consider paying if all else fails. If the collection is not valid, it should come off your report. If the information is not accurate, you have grounds to dispute. Only after all other options have been exhausted should you consider paying.

Don’t Engage

What a collection agency considers “follow-up” is really just a psychological game to break your resistance. According to complaints against MSCB Inc., representatives from the company call twice a day and leave no messages and call consumers even after they’ve asked them to stop.

One consumer reported to the BBB that MSCB Inc. “continues to call a place of business after being told to stop” and uses “robo call with a new name each time.”

Your best recourse here is to say nothing. Every time you speak with a collection agent on the phone, you provide them with more information. They can hear the fear in your voice. They know if you’re willing to pay. You protect yourself by refusing to engage.

In fact, most direct interactions with a collection agency will end poorly for you. You can’t enforce a verbal agreement. Partial payments can restart the clock on the statute of limitations. Admissions can eliminate defenses you didn’t even know you had. If you have a legitimate reason to contact MSCB Inc., do it in writing.

The Dispute Process

Credit bureau disputes are relatively straightforward. You tell the credit reporting agency there is a problem, and they are required to investigate and respond. The credit bureau will reach out to the data furnisher (in this case, MSCB Inc.), and ask for verification. The furnisher has a short period of time to respond and must provide documentation to prove their case. If they fail to respond or can’t verify the information, the account must be deleted.

Note that you’re not interacting with the collection agency directly at this point. You’re not asking MSCB Inc. to do anything. You’re invoking a legal process that requires them to prove themselves. Instead of you having to defend yourself, they must defend their position.

Collection agencies don’t make money by responding to verification requests. Every hour spent on verification is an hour they can’t spend making money.

In some cases, especially with debt they’ve purchased, they may not even have the documentation they need to verify properly. The original documentation may be gone. It may have been destroyed. It may never have been transferred when they bought the debt. That’s a weakness a well-crafted dispute can exploit.

Escalating

You have several decision points in the dispute process. The first comes after your initial dispute. If the account is removed, congratulations! You’ve succeeded. If not, you need to evaluate whether their verification is valid and sufficient. Often, the verification provided is nothing more than a rubber stamp and does not adequately address the questions you’ve raised.

The second decision point comes as you consider escalation. You can always re-dispute an account with more information. You can escalate to the customer service manager at the credit reporting agency.

In some cases, you may want to file a complaint with the CFPB or FTC. The CFPB complaint process, in particular, tends to elicit a more substantive response since the company is concerned about its regulatory review.

Your final decision point may involve deciding whether you should pursue this on your own or whether you need professional assistance. A credit repair expert understands the technical nuances of the FCRA and FDCPA. They understand which arguments work and which don’t. They know what documentation to request and how to escalate effectively if the initial effort doesn’t work.

Why You May Need Professional Help

There are two reasons you may want to consider enlisting some help. The first is the complexity of the situation. Consumer protection law is highly technical and constantly changing. The FDCPA has very specific requirements about what collectors must tell you, when they must tell you, and how they must communicate. Violations you might consider minor could become the basis of a successful lawsuit. Without the proper training and education, though, you won’t recognize the infractions when you see them.

Many of the complaints filed against MSCB Inc. may rise to the level of legal violations. Several consumers have reported that representatives will not identify themselves or the company they represent. The FDCPA requires debt collectors to identify themselves and explain the purpose of their business.

Here’s one example:

“This woman would not identify the company but wanted my personal information. I told her that is against the law. She said no it’s not.”

— BBB Complaint

You need to understand the law to recognize potential violations. You need experience to use those violations to your advantage. That’s where a professional can really help.

The second reason you might want some help is efficiency. The time you spend learning enough to challenge effectively is time the collection account is ruining your credit score. Every month costs you in higher interest rates on loans, declined applications, and even employment background screening. Every month costs you money even if you don’t see it on a statement.

Credit repair professionals do this for a living. What might take you weeks of study and tentative first steps might take them a couple of hours of targeted effort. They know which disputes to file, how to word them, and how to follow up based on the response they get.

Paying for professional assistance may be a fraction of the money you’re losing as you try but fail on your own. If the stakes are your credit score and your financial future, do you really want to try this on your own?

A Final Word

What You Can Do

Seeing MSCB Inc. on your credit report is not a foregone conclusion. The company’s history of consumer complaints, federal lawsuits, and failed verifications suggests many of the accounts they report are highly disputable. Given that 79% of all credit reports contain errors, the onus should be on them to prove accuracy, not on you to prove innocence.

Here are the steps you should take. First, always dispute when possible rather than paying or engaging directly with the collection agency. Second, document everything and carefully track responses. Third, don’t be afraid to escalate when initial efforts don’t get results. Finally, don’t hesitate to get professional help when you need it.

You can get collections removed when the information is inaccurate, erroneous, fraudulent, or when they fail to verify within the designated amount of time. You don’t have to prove you didn’t owe the debt. They have to prove you did. That subtle shift in perspective can completely change the way you approach this.

Get Help Now

If you’re struggling with a collection account from MSCB Inc., contact us at info@FightCollections.com. We help consumers just like you dispute their collection accounts and restore their credit. Our professionals understand the games collection agencies play and know how to beat them at it. We work within the framework of the FCRA and FDCPA to challenge accounts that fail verification.

Don’t wait any longer. Every day you wait is one more day this account is harming your credit. Reach out to us for a consultation today to explore your options and discuss next steps.

You don’t have to live with unfair collection accounts on your credit report. Let us show you how to take back control.