Receiving a collection notice from National Credit Adjusters, LLC (NCA) can get your heart racing. The calls, the letters, the feeling that you need to do something right now.

This is what debt collectors want you to feel. It's how consumers end up doing the wrong thing when they get a collection notice.

In fact, there are several myths about dealing with collection agencies that nearly everyone believes. These myths cost consumers money, cause them to overlook opportunities to get the account removed, and result in years of damage to their credit that could have been avoided.

If you know the truth about these myths, you can protect yourself.

Who Is National Credit Adjusters, LLC (NCA)?

NCA is a debt collection agency and debt buyer based in Kansas. A debt buyer is a company that purchases debt from the original lender for pennies on the dollar. The debt buyer then attempts to collect the debt from you, often a debt that has already been sold to several debt buyers previously. Often, the documentation for the debt has become lost or destroyed along the way. This can help you in your effort to dispute the debt.

NCA is a debt buyer that has been the subject of over $6.5 million in fines, settlements, and restitution paid to consumers since 2014. The July 2018 consent order issued by the Consumer Financial Protection Bureau (CFPB) against NCA and former NCA CEO Bradley Hochstein, along with the January 2015 settlement between NCA and the New York City Department of Consumer Affairs are just two examples of NCA's history of illegal debt collection practices.

Understanding this history is essential to disputing a debt that NCA is attempting to collect from you.

The $6.5 Million Dollar Man

In July 2018, the CFPB issued a consent order against NCA and former NCA CEO Bradley Hochstein. The consent order resulted from a CFPB investigation that found NCA violated the Consumer Financial Protection Act (CFPA) and the Fair Debt Collection Practices Act (FDCPA).

According to the consent order, NCA engaged in illegal debt collection practices that included creating and supervising a network of collection companies that regularly engaged in illegal debt collection practices when collecting debts for NCA. These practices included threatening consumers with lawsuits and using process servers to deliver lawsuits when NCA did not intend to file the lawsuit. NCA representatives also threatened consumers with arrest when they had no intention or authority to have consumers arrested.

Former NCA CEO Bradley Hochstein was permanently banned from working in the debt collection industry as a result of the consent order. NCA was required to pay an $800,000 penalty to resolve the consent order allegations.

In January 2015, the New York City Department of Consumer Affairs (NYCDCA) announced a settlement with NCA. The NYCDCA found NCA had engaged in illegal debt collection practices when attempting to collect debts from New York consumers. These practices included attempting to collect payday loan debts that were void under New York law.

NCA was also found to have engaged in debt collection practices that were deceptive and an abuse. Specifically, NCA misrepresented the amount of the debts consumers owed, the character and legal status of the debts, and whether NCA had the intent or right to sue consumers who did not pay the debts. As a result of the settlement, NCA paid $1,271,838.95 in restitution to consumers and fines.

The NYCDCA deemed NCA the worst offender of the 23 debt collection agencies it fined for attempting to collect debts on illegal payday loans.

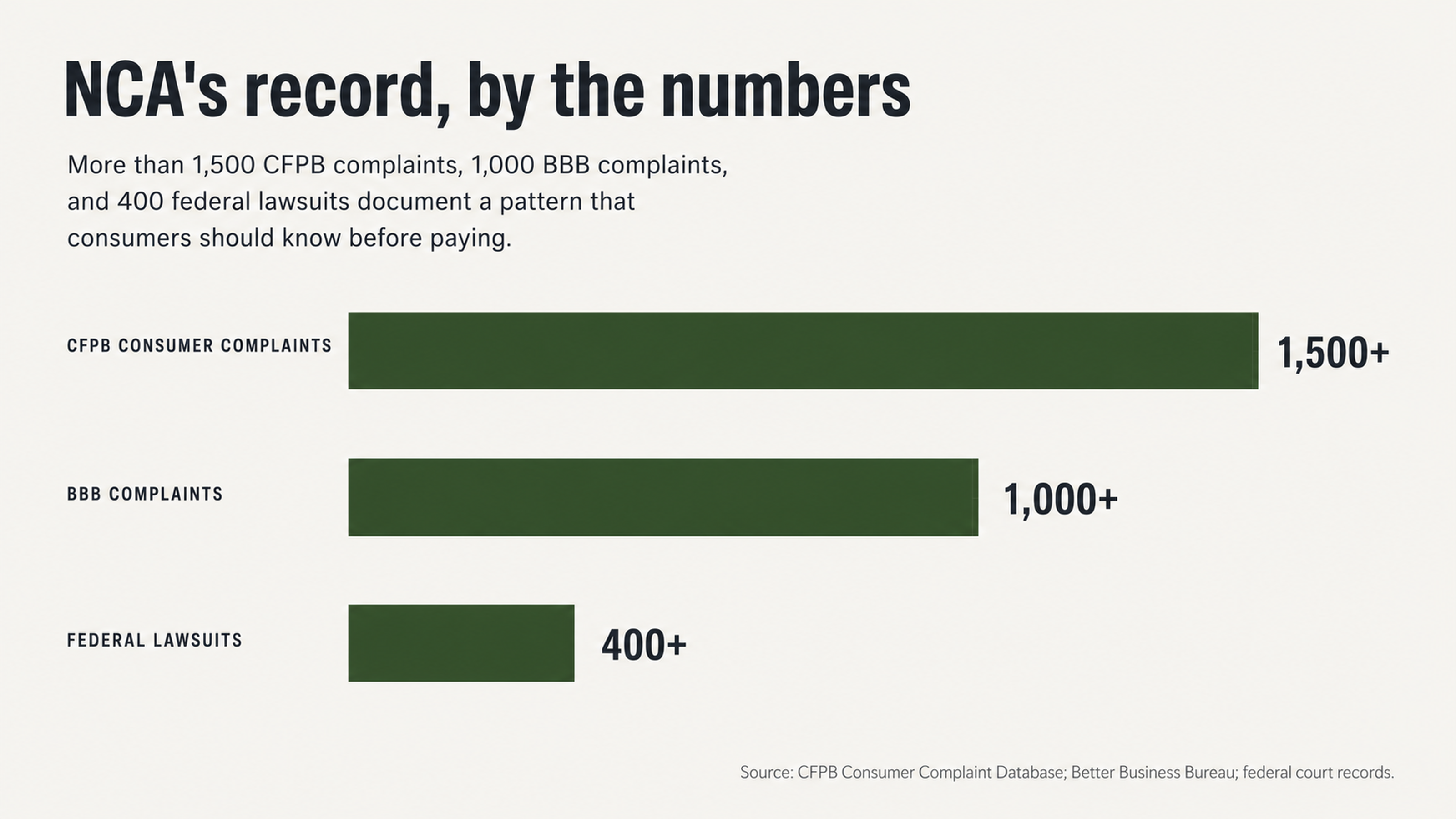

In addition to the CFPB consent order and the NYCDCA settlement, there are over 1,000 complaints about NCA on the Better Business Bureau (BBB) website and over 1,500 complaints about NCA in the CFPB consumer complaint database. NCA has been a party to over 400 federal lawsuits, most of which were filed by consumers alleging NCA violated their rights under one or more federal consumer protection statutes.

The "I'll Just Pay It" Myth

Most consumers believe that if they pay a debt collection agency the amount the agency claims they owe, the agency will update their credit report to reflect that fact and the negative mark associated with the debt collection will be removed from their credit report.

The Fair Credit Reporting Act (FCRA) requires credit reporting agencies to remove negative marks from a consumer's credit report seven years from the date of first delinquency. If you pay a debt collection agency, the agency will update your credit report to reflect the fact that you have paid the debt. However, the date of first delinquency remains the same. As a result, the credit reporting agency will not remove the debt collection from your credit report simply because you paid it. The credit reporting agency will continue to report the debt collection for seven years from the date of first delinquency.

In addition, simply paying a debt collection agency is unlikely to result in the agency removing the debt collection from your credit report. Instead, you should exercise your right to dispute the debt under the FCRA. If you dispute the debt and the credit reporting agency cannot verify the debt, it must be removed from your credit report.

Often, simply paying a debt collection agency can even harm consumers when the debt is very old. The FCRA allows debt collection agencies to sue consumers for debts for a certain period of time. In some states, if you pay a debt collection agency money on a debt, the period of time the agency has to sue you for the debt may start over. Additionally, if you pay an agency money on a debt you do not owe, you may eliminate defenses you could have raised if the agency decided to sue you.

As a result, if a debt collection agency contacts you about a debt, you should not simply pay what the agency is asking you to pay. Instead, you should investigate the debt to determine whether the agency has the right to collect money from you and whether the amount the agency is asking you to pay is correct.

What Really Impacts Your Credit Score

If you are contacted by a debt collection agency about a debt, you should not focus on simply paying the debt. Instead, you should focus on determining whether the agency is accurately reporting the debt on your credit report and whether you can get the agency to remove the debt from your credit report entirely.

The FCRA prohibits credit reporting agencies from reporting inaccurate information about consumers. If an agency is reporting a debt about you that is not accurate, you have the right to dispute that information with the credit reporting agency. The credit reporting agency must conduct an investigation to determine whether it is reporting inaccurate information about you. If the agency determines the information is not accurate, it must remove the information from your credit report.

Most credit scoring models place a significant emphasis on whether you have any debt collections on your credit report when determining your credit score. Simply paying a debt collection will not remove it from your credit report. However, if you dispute a debt collection because it is not accurate and the credit reporting agency cannot verify the debt, the agency must remove the debt entirely from your credit report.

The Accuracy Myth

Most consumers believe that if a debt collection agency is reporting a debt about them on their credit report, the debt must be legitimate and they must owe it. However, this is not true. Debt buyers like NCA purchase debts from other companies without receiving all of the documentation associated with the debt. Often, consumers will dispute a debt with a debt buyer only to find out the buyer cannot provide any documentation about the debt to verify it.

If a credit reporting agency is reporting a debt about you that you did not incur or that is not accurate, you have the right to dispute the debt with the agency. The FCRA requires credit reporting agencies to conduct an investigation into disputed debts. If the agency cannot verify a debt is accurate, it must remove the debt entirely from your credit report.

In fact, a 2012 study by the consumer advocacy group U.S. Public Interest Research Groups (U.S. PIRG) found that 79 percent of credit reports contained either errors or serious errors. As a result, there may be other information on your credit report that you should dispute with the credit reporting agency.

If you believe any of the information on your credit report is inaccurate, you should dispute it with the agency. Simply ignoring inaccurate information on your credit report can damage your credit score for years to come.

The Illegal Practices Myth

Most consumers believe that debt collection agencies can do whatever they want when attempting to collect debts. This includes making phone calls whenever the agency wants, threatening whatever the agency wants, and filing a lawsuit against the consumer whenever the agency wants. However, this is not true.

The FDCPA prohibits debt collection agencies from engaging in unfair, deceptive, and abusive debt collection practices. For example, a debt collection agency is not allowed to threaten to have you arrested if you do not pay a debt. In addition, debt collection agencies are not allowed to threaten to file a lawsuit against you unless it intends to do so.

If you believe a debt collection agency has violated your rights under the FDCPA, you should speak with a consumer protection attorney. You may have the right to sue the agency for statutory damages, actual damages, and attorney's fees.

In addition, you should file a complaint with the Federal Trade Commission (FTC) and the CFPB so the agencies are aware of the potentially illegal debt collection practices in which the debt collection agency is engaging.

The Urgent Action Myth

When a debt collection agency contacts you about a debt, it often wants you to take urgent action. This can include demanding you pay a certain amount immediately or face a lawsuit, demanding you pay a certain amount immediately or the agency will report negative information to the credit reporting agencies, or making threatening phone calls to you at work or in front of your family.

However, you should not take urgent action. In many cases, taking urgent action can actually harm you. Instead, you should make sure you understand your rights under the FDCPA and the FCRA. You should also make sure you understand the debt the agency is attempting to collect and whether you owe it.

You should not give the agency money for a debt you do not owe or a debt you cannot afford to pay. In addition, you should only communicate with debt collection agencies in writing. If you communicate with an agency over the phone, the agency may mislead you into doing something that can harm you.

If you communicate with an agency in writing, you have a paper trail of what the agency is telling you and you can take time to determine how you want to proceed without feeling pressured.

The DIY Myth

Many consumers attempt to handle debt collection issues on their own. However, this can be very difficult. You must have a good understanding of your rights under the FDCPA and the FCRA. You must also be willing and able to communicate effectively with the debt collection agency and the credit reporting agencies to attempt to resolve the issue in your favor.

If you are not sure what your rights are or how to communicate with a debt collection agency or a credit reporting agency, you may inadvertently do something that can harm you. As a result, you may want to consider hiring a consumer protection attorney or credit repair agency to assist you.

A consumer protection attorney can help you understand your rights and help you enforce them. A credit repair agency can also help you understand your rights and communicate with credit reporting agencies to attempt to remove negative information from your credit report that you believe is inaccurate.

Every debt deserves scrutiny before any action is taken. The pending Virginia class action against NCA involves over $44 million in debts that were legally void under state law. Challenging the validity of a debt is not a technicality or a loophole. It is a fundamental consumer right that exists because the system produces so many errors.

Conclusion

If you are contacted by National Credit Adjusters about a debt, you should not panic. You should not simply pay what the agency is asking you to pay. Instead, you should understand your rights under the FDCPA and the FCRA. You should make sure you understand the debt the agency is attempting to collect and whether you owe it.

You should only communicate with the agency in writing and you should take your time in determining how you want to proceed. You should also consider hiring a consumer protection attorney or credit repair agency to assist you.

FightCollections.com specializes in disputing collection accounts and fighting for consumers against debt collectors with records like NCA's. Contact us today to schedule a no cost consultation to discuss your situation.

.webp)