Are you tired of National Credit Systems ruining your credit report? If so, you’re not alone.

The Atlanta-based debt collector has a long history of harassing consumers over apartment-related debts, and it’s imperative that you understand their most common mistakes before you decide how to approach the situation.

Debt collectors like National Credit Systems want you to feel as overwhelmed and misinformed as possible. But once you have a basic understanding of their regulatory infractions, common complaints, and known errors, you can find the leverage you need to dispute their claims successfully.

In this article, we’ll cover the essential information you need to know about National Credit Systems before we dive into the ways they commonly goof up.

Who is National Credit Systems?

National Credit Systems, Inc. is a debt collection agency that specializes in the multi-family housing industry. Before you respond to their letters or make a payment, make sure you understand who you’re dealing with. Here is their contact information:

The company represents over 15,000 apartment communities across the country and tries to collect on various debts, including unpaid rent, property damage (in excess of a security deposit), early lease termination fees, and move-out fees.

Although National Credit Systems only collects apartment debt, that doesn’t mean they’re exempt from the same rules and regulations as any other consumer debt collection agency.

National Credit Systems’ history of regulatory infractions, consumer complaints, and known mistakes

In addition to the complaints registered with the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC), the Better Business Bureau lists nearly 3,000 complaints filed against National Credit Systems in the past three years. The company currently holds an F rating with the BBB and is not accredited.

Many of the complaints surround the company’s failure to communicate effectively with consumers and failure to verify debts upon request.

The company has faced over 570 federal court cases, primarily involving allegations of Fair Debt Collection Practices Act (FDCPA) and Fair Credit Reporting Act (FCRA) violations. In a recent case, the jury awarded one consumer $500,000 in emotional distress damages after determining that NCS did not conduct a reasonable investigation when a consumer disputed a debt. Although the company is appealing the verdict, this case sets a dangerous precedent for future FDCPA and FCRA lawsuits against National Credit Systems.

These statistics aren’t just numbers — they represent very real mistakes that you can use in your favor if you know how to recognize them.

How to recognize the common ways that National Credit Systems messes up

October 2022 CFPB Civil Investigative Demand issued

In October 2022, the CFPB served National Credit Systems with a Civil Investigative Demand (CID) to investigate their business practices and determine whether they are complying with federal consumer protection laws. Specifically, the CFPB wants to know whether National Credit Systems is:

Furnishing information to CRAs that they know or should know is inaccurate, and

Failing to review and respond to direct dispute notices as required by law.

When National Credit Systems failed to comply with the CID, the CFPB filed a Petition to Enforce with the federal court in February 2023. This is not a routine practice for the CFPB, so it’s safe to say they’re taking the actions of National Credit Systems very seriously.

As a consumer who is currently dealing with National Credit Systems, this is excellent news. It means that the behaviors you’re experiencing might already be on the radar of the CFPB, and they may determine that these actions violate your federal rights as a consumer.

National Credit Systems’ credit reporting mistakes

Under the Fair Credit Reporting Act (FCRA) and Regulation V, debt collectors have a responsibility to develop and implement reasonable procedures to ensure the accuracy of the information they are reporting. They must also conduct a reasonable investigation when a consumer disputes the information directly with the CRA or the debt collector.

When debt collectors fail to meet these expectations, you may have grounds to dispute the information with the credit reporting agencies.

According to several complaints filed with the CFPB, National Credit Systems is placing accounts on consumers’ credit reports before the dispute period has expired. They’re also re-aging debts to make them appear newer than they actually are.

In one lawsuit against the company, the consumer claimed that National Credit Systems reported a 15-year-old debt as being less than seven years old. They also incorrectly notated the balance as $790,977 for an apartment lease.

While these might seem like honest mistakes, they can make a big difference if you’re trying to repair your credit report. If a debt collector cannot verify the information they’re reporting or fails to conduct a reasonable investigation, you may be able to have the information removed from your report. It’s not a matter of whether or not these things are happening, but rather, do you know how to identify and dispute them?

Failure to validate debts

The Fair Debt Collection Practices Act (FDCPA) says that you have the right to request validation of a debt within 30 days of initial contact. Once you make this request, the debt collector must stop all collection activities until they provide the validation you requested.

This is where many debt collectors, including National Credit Systems, tend to fall short.

In a complaint filed with the BBB, one consumer wrote: “National Credit Systems has reported to the credit companies that myself and my husband owe over $4,000 in rental related charges and won’t respond to my request for them to provide validation or verification that I owe the amount they are charging.”

We see this same trend over and over again in reviews across the internet — this is not an isolated incident.

If a debt collector cannot provide the documentation you need to prove that the debt is valid, that it belongs to you, and that the amount is accurate, you have the leverage you need to negotiate a settlement or request removal of the negative mark.

Why debt collectors hate costly verification

When debt collectors purchase debt from the original creditor, it does not always come with the complete documentation you need to verify that debt. It may require the debt collector to dig up the original lease agreement, payment records, and any documentation of damage or repair.

Obtaining this documentation is a costly and time-consuming process that requires a significant amount of money. Debt collection agencies work on small margins and need to collect as many debts as possible. When you present a well-documented dispute that’s going to require a lot of time, money, or both to verify, the debt collector may decide that your debt isn’t worth pursuing.

Instead of verifying the debt and continuing the collection process, they will simply dismiss the account. It’s not because you paid the debt — in fact, you didn’t pay anything at all. It’s because the cost of pursuing the debt was more than what they were likely to collect.

Whenever you’re negotiating with a debt collector, don’t forget that your actions have consequences. Every letter you force them to write, every phone call you cause them to make, and every court filing you inspire all cost money. If you can make their job expensive enough, they may decide it’s not worth it at all.

Consumer complaints filed against National Credit Systems

What are other consumers saying about National Credit Systems? If you look at the company’s reviews on Google, you’ll see an average rating of 1.9-2.1 stars out of five. On WalletHub, the average rating is 2.0 stars, with 70% of the reviews being only one star.

Clearly, most consumers are not impressed with the service they receive from National Credit Systems.

Here’s what one consumer had to say about their experience:

“I have been harassed for 7 months about a debt that does not exist. The group that I supposedly owed this debt to confirmed that there was no debt, but the collection representative refuses to stop calling and mailing letters to me and threatening me with legal action unless I pay him directly.”

In this situation, the consumer says that National Credit Systems is attempting to collect a debt that they do not owe. Despite their efforts to resolve the issue directly with the representative, the phone calls and letters continue.

Another consumer experienced an issue with National Credit Systems placing items on their credit report, only to remove them and place them again. They wrote:

“They keep removing something from my credit report and then adding it again. It’s something that really shouldn’t be on my credit report to begin with.”

Based on this consumer’s complaint, it appears that National Credit Systems is manipulating their credit report by repeatedly adding and removing the same item. Regardless of their motivation, this behavior is concerning and may violate the consumer’s rights under federal law.

The Harassment Question

The FDCPA outlaws harassment, misrepresentation, and unfair practices. Collectors cannot threaten action they have no intention of taking, cannot call at inappropriate hours, and cannot use profanity. These rules exist because the debt collection industry has a history of crossing these boundaries.

Here’s how one consumer describes a bad experience:

“I wasn’t able to get a word in edgewise, had to ask them to quit talking over me and remind them that I’m calling to RESOLVE an issue. I asked for an agreement in writing and they wouldn’t give me one. Then they hung up on me. I called back and heard the original woman yell ‘She’s calling back again!’”

Not only is this kind of service unacceptable. It may be a violation of federal law. When a debt collector harasses you, they open themselves up to liability.

But for purposes of resolving the account, harassment is often correlated with other compliance issues. If a collector can’t keep their behavior professional, there’s a good chance they’re falling short on documentation and verification.

Why You Shouldn’t Pay First

The Original Creditor Has Already Written You Off

When your debt gets assigned to a collection agency or sold to a debt buyer, the original creditor has made a business decision. They’ve either written off the debt as uncollectable and assigned it to a collection agency, or they’ve sold it outright. In either case, they’ve closed the book on you.

The apartment complex or property management company that originally claimed you owed them money has moved on. That fact affects the ethical argument debt collectors make.

The emotional impact of owing a debt is a powerful tool for debt collectors. But it’s worth considering rationally. If the original creditor has already written off the loss, why should you still be feeling the pressure of an uncollectable debt?

Realizing this helps consumers approach collection accounts from a more clinical perspective. The question isn’t whether or not you feel bad about owing a debt. The question is whether or not the debt is accurately reported, properly verified, and complies with the relevant laws.

Paying Because of Guilt Is What Collectors Want

Collection agencies will try to make you feel like the only ethical decision is to pay. They’ll use language designed to make you feel guilty. But remember: those feelings are what the collector is trying to manipulate. You have legal rights here, and exercising them isn’t dishonorable.

The law outlines specific procedures for disputing a debt, requesting validation, and challenging credit reporting errors. These laws exist because lawmakers recognize that the debt collection industry makes mistakes and sometimes engages in abusive practices.

When you pay a collection account, you’re updating the status of that account from “unpaid” to “paid.” But you aren’t removing the account from your report. You’ve satisfied the debt but not the credit reporting damage.

Why You Should Dispute First

Credit Reporting Errors Are Shockingly Common

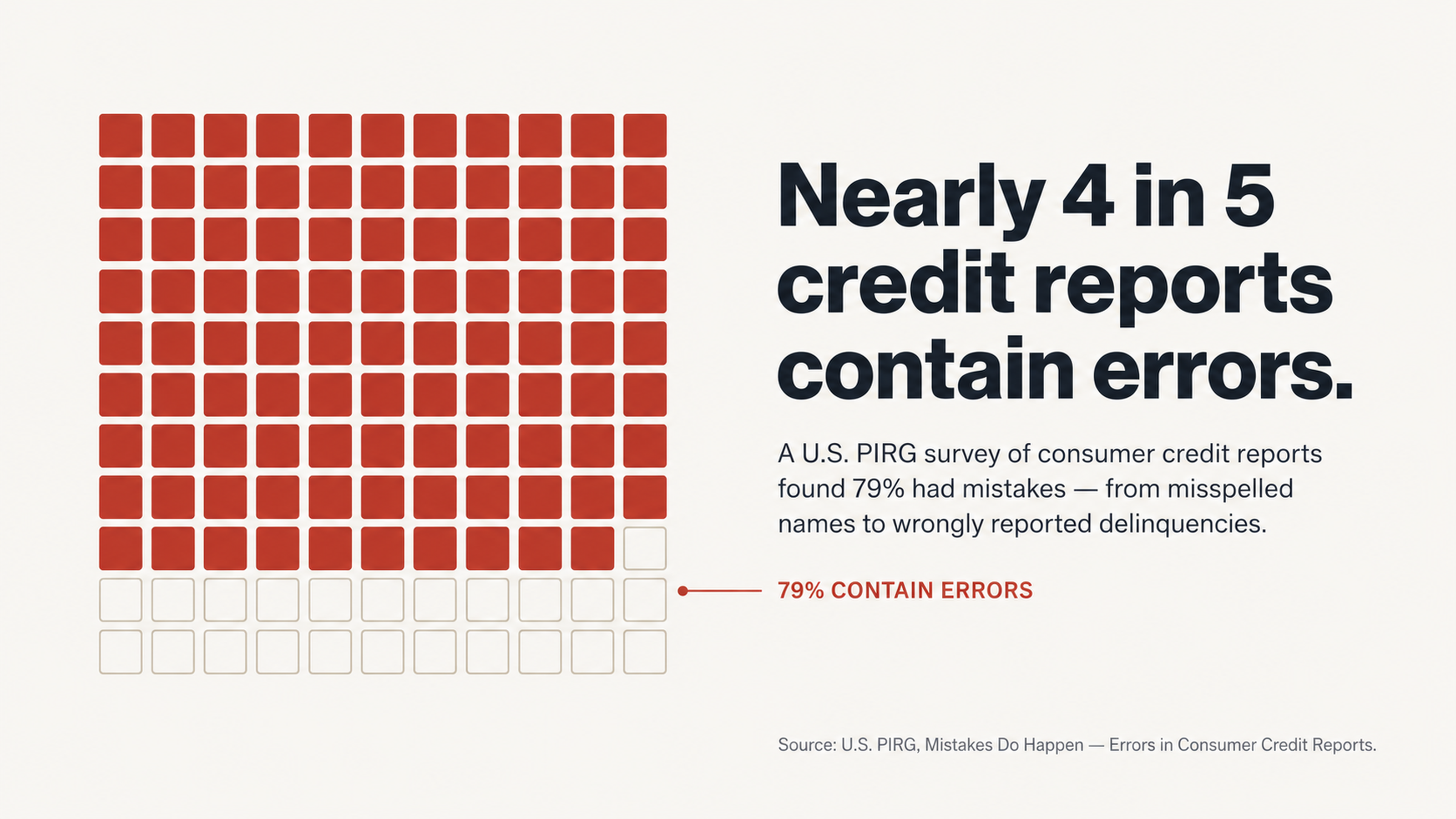

A study done by U.S. PIRG shows that 79% of credit reports contain errors or disputed information. That’s not a minority. That’s nearly four-fifths of all credit reports. If you assume a collection account might have some errors in it, you’re not being paranoid. You’re being informed by the available data.

Errors can be in the form of the wrong balance, the wrong date, someone else’s debt, debts that have already been paid, balances that include improper fees, and accounts that should have fallen off the report by now. Each one of those error types is a potential avenue for dispute.

The information balance in debt collection is weighted heavily towards the debt collector. They know what records they have. They know what documentation they have. You know only what you see on your report. The dispute process forces the debt collector to tell you what they actually have. And in many cases, what they have isn’t enough to verify the debt.

Professional Help

Navigating a successful dispute requires knowledge of the relevant laws, the proper way to document things, and the best times to dispute a debt. Consumers who try to handle collections on their own end up making costly mistakes. They reset the statute of limitations clock. They acknowledge debts they should have disputed. They agree to settlements that still harm their credit.

Credit repair professionals know the right way to maximize your chances of success. We know how to word a dispute. We know what documentation to request. And we know when to escalate a dispute that isn’t getting results. Most importantly, we know the economics of debt collection and how to make pursuing a debt too costly for the collector.

National Credit Systems, with their history of compliance issues, their unanswered complaints, and their pending federal investigation, is exactly the kind of debt you might need professional help with. There are patterns of failure here. The only question is whether or not you know how to use them.

Conclusion

National Credit Systems has racked up almost 3,000 complaints with the Better Business Bureau over the course of three years. They’ve been the target of over 570 federal lawsuits. They’ve earned an F rating from the Better Business Bureau. And they’re currently the target of an active investigation by the CFPB for possible violations of consumer protection laws.

A jury just awarded one consumer $500,000 because they proved that NCS didn’t properly investigate a disputed debt.

These are not the hallmarks of a company with rock-solid compliance protocols. Every complaint left unanswered is a potential flaw in how this collector operates. Every compliance failure is a potential flaw. Every regulatory finding is a potential flaw. Where there are flaws, there are potential disputes to be made. And consumers who get collection accounts removed from their credit reports are consumers who recognize that and proceed accordingly.

Paying a collection account changes your relationship to the debt. But it doesn’t remove the account from your report. Disputing the account puts the burden of proof on the collector. They have to demonstrate that everything they’re reporting is accurate, verified, and in compliance with the law.

Everything we’ve talked about suggests that National Credit Systems may have a tough time rising to that challenge.

Take Action Now

If National Credit Systems is reporting on your credit, you don’t have to go it alone. The compliance issues, the regulatory history, the court cases, and the complaints all create potential avenues for disputing the debt. And the professionals at FightCollections.com know how to make the most of them.

We specialize in fighting debt collectors and disputing erroneous information on consumer credit reports. We know the tactics that companies like National Credit Systems use. And we know where their tactics tend to break down.

Contact us today for a free consultation. Learn how we can help you resolve this collection account the right way.