If you have an unfamiliar medical collection on your credit report, the first sign might be a collection notice in the mail. If you’re reading this, it’s likely that you’re seeing an unfamiliar collection agency reporting a medical collection.

If that agency is Nationwide Recovery Service, it is one of the oldest medical collection agencies in the country. Understanding who Nationwide Recovery Service is and how they operate is the first step to getting this account off your credit report.

A Medical Debt Collection Agency with a Bad Reputation

Nationwide Recovery Service is a medical debt collection agency, meaning they sit between healthcare providers and patients who owe money. In September 2023, they were acquired by ACCSCIENT, a global technology services company. ACCSCIENT has 18 offices across the globe and generates $350 million in annual revenue.

Despite their experience and deep pockets, NRS has terrible customer reviews. On WalletHub, the company averages 1.9 of 5 stars (37 reviews), with 70 percent of reviewers giving the company one star. NRS is not accredited by the Better Business Bureau (BBB), and the BBB gives their Georgia office an F rating, citing a failure to respond to consumer complaints.

The company’s federal court history is even more alarming. Since 1990, NRS has been sued in federal court over 65 times, mostly for violating consumer protection laws. These lawsuits involve violations of the Fair Debt Collection Practices Act (FDCPA) and the Telephone Consumer Protection Act (TCPA).

The damage that a medical collection causes to your credit report

The Seven Year Rule

If Nationwide Recovery Service has placed a medical collection on your credit report, you might already be aware of the damage that it is causing. When a collection agency reports a collection to the credit reporting agencies, it begins the seven year clock. This clock starts from the original delinquency date, and cannot be restarted by selling the debt or placing it with a new collection agency.

Many consumers believe that paying a collection will get it removed from their credit report, or at least shorten the amount of time that the damage is reporting. This is not typically the case. Paying an old collection will update the status to paid, but it will stay on your report for the full seven years.

In many cases, paying an old collection will not result in any improvement to your credit score. While newer credit scoring models may differentiate between paid and unpaid collections, the initial credit damage has already occurred. Before you pay an old collection, you need to understand this.

Why you shouldn’t pay a collection without verifying the debt

When a debt collector calls to demand payment, they use as much urgency as possible. This is a tactic to get you to pay without verifying the debt, and it plays on your emotions. The emotional response of owing a debt is one of the primary tools that collectors use to get consumers to pay.

Most collection agencies purchase debt from the original creditor for pennies on the dollar. When a hospital places your $2000 emergency room bill with a collection agency, they may have already given up on collecting it. The agency may pay less than $100 for the debt, so anything they collect is pure profit.

This means that even if you owe the debt, you may not need to pay it in full. But more importantly, if you pay the debt before verifying it, you are giving up your leverage. The reason that the collector wants you to pay right now is because once you start asking questions, you may discover a problem with their documentation.

Why you should always verify a debt

79 percent of credit reports contain errors or inaccuracies

Advocacy groups have shown that credit reports are wrong a surprising amount of the time. According to research by U.S. Public Interest Research Groups, 79 percent of credit reports contain mistakes or serious errors. These are not minor errors, but mistakes that could effect lending decisions, insurance rates, or employment.

When it comes to medical debt collection, there are even more opportunities for error. Billing for healthcare is extremely complex, and often happens months after care was provided. Insurance adjustments, appeals, and secondary insurance all create opportunities for miscommunication between the provider and the collection agency.

When a debt is sold to a collection agency, the documentation doesn’t always make the transfer. The collection agency may only receive the consumer’s name, social security number, and balance due, but not the underlying documentation to prove that the debt is valid. This is a legitimate reason to dispute the debt.

Consumer complaints describe a pattern of errors

When you read about consumers’ direct experiences with NRS, there is a pattern of potential errors and illegal activity. In a February 2024 complaint to the BBB, one consumer said that she received a voicemail from NRS so menacing that the hairs on the back of my neck stood up. The caller said I am going to have to hang up and go away, just like MY money.

Another consumer complained that NRS contacted her to collect a medical bill that she already paid. They were attempting to collect the balance that the provider wrote off because she was uninsured at the time. After she sent documentation showing that the bill was paid in full, the collection was removed from her credit report. Later, the same collection was filed again.

Attempting to collect a debt that has already been paid is a major compliance concern.

In other reviews, consumers describe NRS attempting to re-age debts by changing the date of delinquency, calling family members and disclosing debt information, and continuing to call after the consumer has asked them to stop. Each of these activities, if they happened as described, would be violations of federal law.

Why you should dispute medical collections

The power of requesting debt validation

When you dispute a debt, you are asking the collector to prove that it is valid. The FDCPA requires that the collector provide documentation showing that you owe the debt, the amount is accurate, and the collector has the legal right to collect it.

For a debt collector, responding to a dispute requires finding the original documentation and assembling a response. This can be time consuming, especially for a company like NRS that has a high volume of collection accounts. Many collection agencies cannot properly respond to verification requests.

If the collector cannot validate a debt, the credit reporting agencies must remove it from your credit report. This does not mean that the debt magically goes away, but the agencies cannot report information that they know may be inaccurate.

Silence is golden when dealing with a collection agency

Collection agencies rely on your emotional response when they contact you. Your sense of obligation, guilt, and fear are all tools in their toolkit. When they call, their goal is to get you to pay as quickly as possible.

The best way to combat this is to avoid interacting with the collector at all. Do not call them, and if you talk to them on the phone, do not give them information or make promises to pay. Every time you talk to a debt collector on the phone, you give them an opportunity to confirm your contact information, obtain a payment, or extract additional information from you.

When you send a written dispute to the credit reporting agency, you create a paper trail and they must respond. This process levels the playing field, as the collector must meet the legal burden of proof.

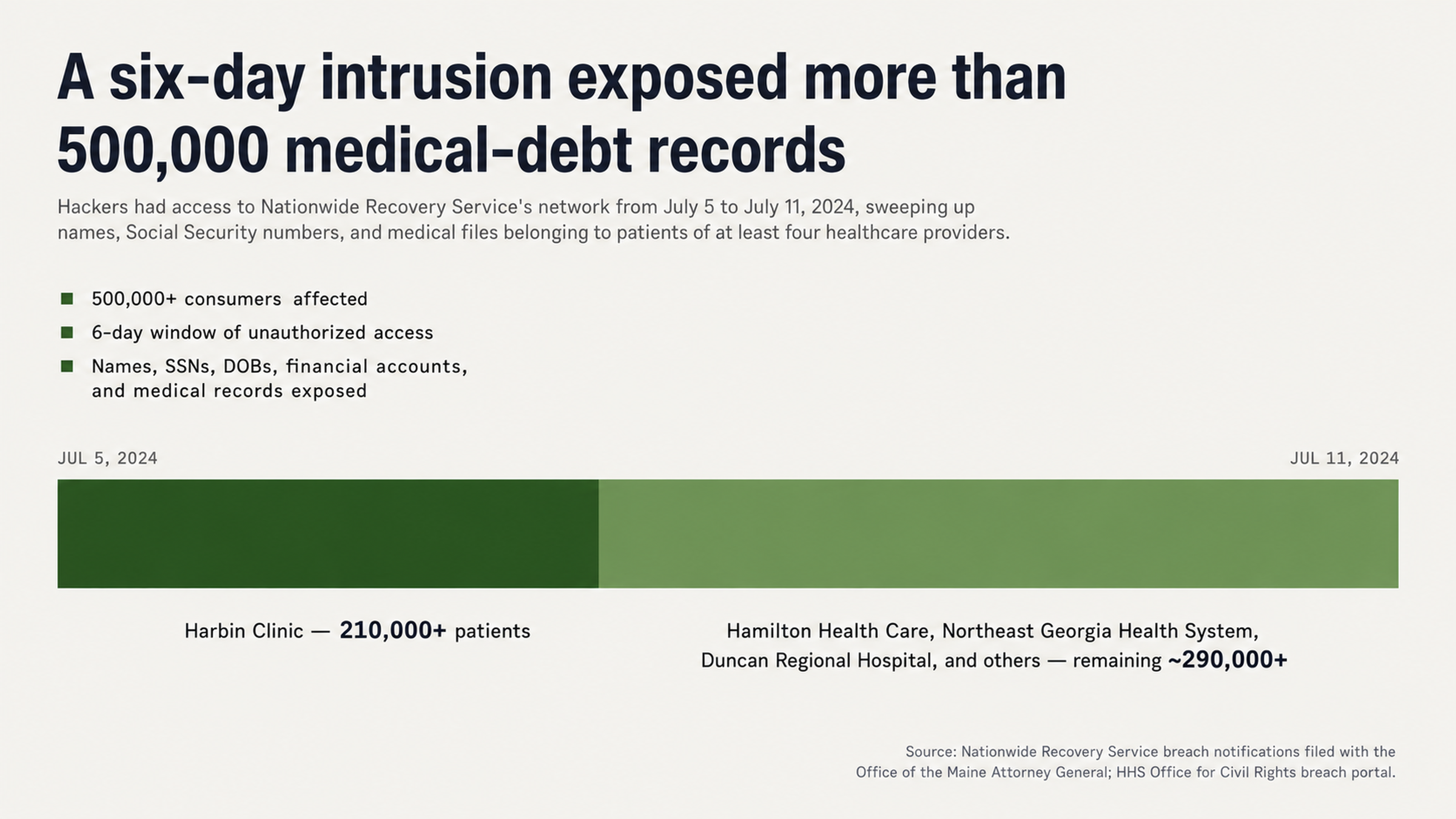

Why you should be concerned about the 2024 data breach

In July 2024, Nationwide Recovery Service announced a data breach that exposed the personal data of over 500,000 consumers. The breach occurred between July 5 and July 11, 2024. The breach affected consumers whose medical information was being collected by NRS on behalf of several healthcare providers.

The data breach included names, social security numbers, dates of birth, financial account information, and medical records. Several healthcare providers were affected, including Harbin Clinic (over 210,000 consumers affected), Hamilton Health Care, Northeast Georgia Health System, and Duncan Regional Hospital.

If you are disputing a debt from Nationwide Recovery Service, the data breach may provide additional justification. If you were involved in the breach, you may have collection accounts on your credit report that were misassigned to your identity, or the balance may have been altered during the breach.

The breach may affect debt validation

When a collection agency experiences a data breach, it can create unique problems for debt validation. When hackers gain access to consumer data, they may alter balances, misassign accounts, or co-mingle personal identifying information.

Consumers who have collection accounts from NRS on their credit report during or after the breach period may have reason to demand additional verification. The collector still has the burden of showing that their records are accurate, despite the breach.

At least two class action investigations are underway related to the 2024 breach. Law firms are seeking consumers who were affected, and may ultimately file a class action lawsuit. This additional scrutiny may make the company more likely to respond to consumer disputes and verification requests.

How to deal with an inaccurate medical collection

Why you need professional help

Debt validation and disputes require a good understanding of federal regulations, timelines, and documentation. A professional credit repair expert can help you navigate the system and meet deadlines. They can also help you understand how to properly document your communication and avoid pitfalls that might damage your case.

Collection agencies respond differently when they know a consumer has hired a professional. When credit repair experts send a validation request or dispute letter, it sends a message that the consumer is represented and willing to take action.

Additionally, professional credit repair experts understand the most common mistakes that consumers make when disputing debts. They can help you avoid accidentally validating a debt, missing a deadline, or admitting to a debt that you do not owe.

When you find one error, look for more

When you discover an error with a debt that Nationwide Recovery Service is collecting, it should prompt you to take a closer look at your entire credit report. If there is one error, there may be more. The same systemic problems that caused one inaccuracy may have caused others.

Many consumers who successfully dispute one debt often find more when they take a closer look. You might find other medical collection accounts from different agencies with the same documentation problems. You might find errors from original creditors. Whatever prompted you to dispute one debt should cause you to take a hard look at everything.

This is the difference between credit repair and credit maintenance. Instead of waiting for a medical collection to cause a problem when you apply for a loan or a job, you are taking a proactive approach to managing your credit report. Find the errors and correct them before they cause problems.

Conclusion

Don’t pay a medical collection until you verify it

If you have a medical collection from Nationwide Recovery Service on your credit report, don’t pay it until you verify that it is yours. With the company’s history of consumer complaints, federal lawsuits, and data breach affecting over half a million people, you have every right to be skeptical.

Instead, start with a dispute. If the information is inaccurate, a duplicate, or not properly verified, you have the right to have it removed. Paying the collection before you verify it gives up your leverage, and may not even help your credit score.

FightCollections.com is a credit repair agency that specializes in verifying collection accounts. We understand what the collection agency needs to show to verify a debt, and the steps needed to properly dispute it. If you have a Nationwide Recovery Service account on your credit report, contact us for a free consultation.

This is your credit report, and you deserve to have it accurate.