Seeing a collection account on your credit report is similar to discovering an uninvited houseguest in your home. If the collection agency is NCB Management Services, then you’ve got some red flags to watch out for. NCB has a concerning history, so keep reading to learn what you need to know.

A U.S. Public Interest Research Groups study shows that 79% of credit reports contain errors or other inaccuracies. Before you even call, pay, or stress, you need to consider that the NCB collection account on your credit report could be one of them.

While you can’t assume the account isn’t legitimate, you can’t take for granted that the information the collection agency is reporting about the account is accurate. There are all sorts of problems with the information reported by collection agencies, but consumers never notice because they assume it must be right.

In fact, before you do anything, take a deep breath. The debt collection industry makes its money off of urgency and intimidation. You have the upper hand if you know what you’re doing, so let’s get started.

Who is NCB Management Services?

NCB Management Services, Inc. is a debt collection agency that works as a third-party debt collector and debt buyer. Here is their contact information:

NCB collects debts for credit cards, personal loans, auto loan deficiencies, and mortgage servicing accounts. They have collected debts for original creditors including Bank of America, Capital One, and Santander Consumer USA. In August 2021, Dallas-based private equity firm Trive Capital acquired a majority stake in the company.

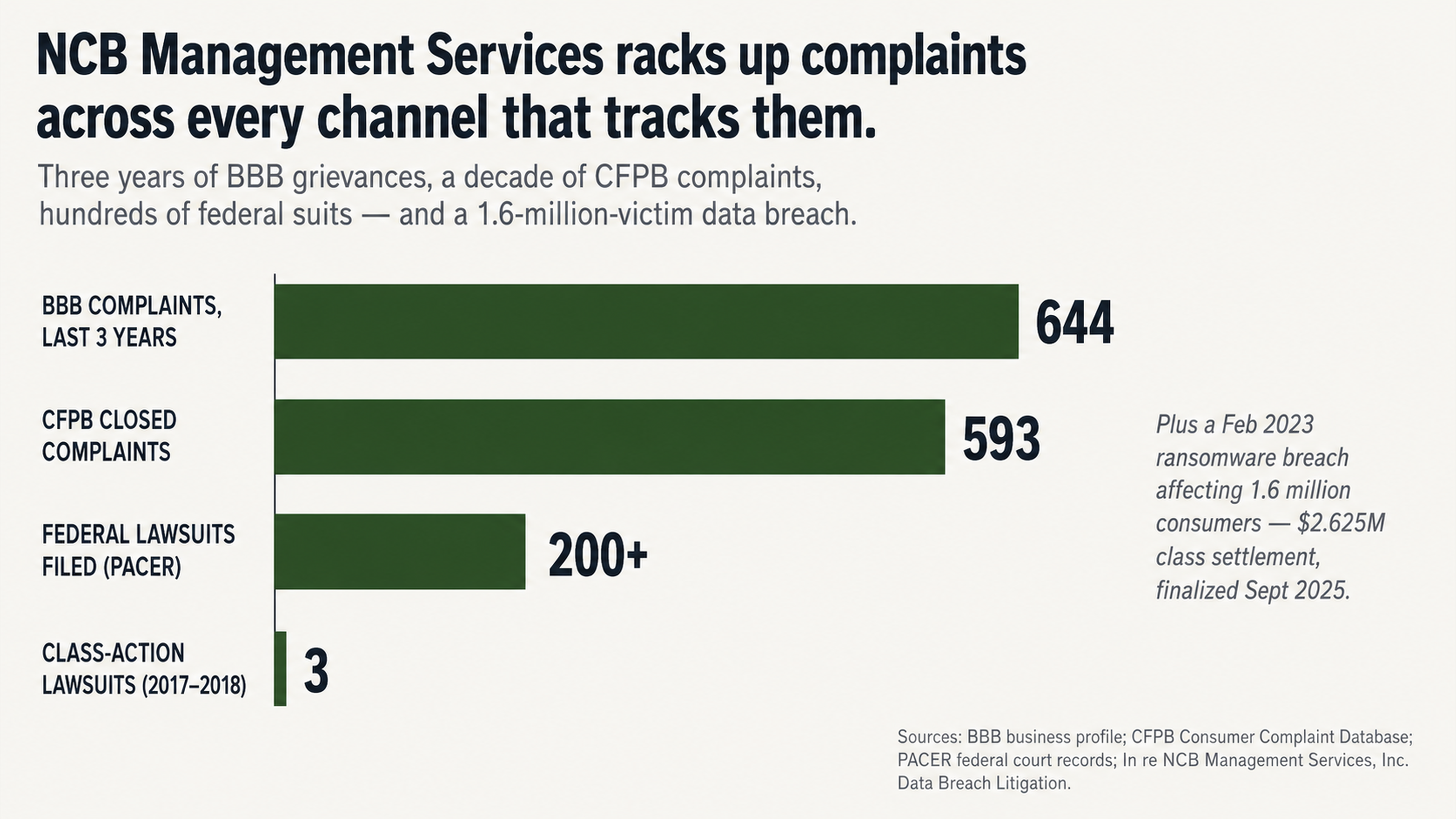

Why You Should Be Concerned

As you can see, NCB has been around for a long time and collects all sorts of debts. You might not need to be concerned about their presence on your credit report at all. Then again, you might. Let’s look at their history.

Over the last three years, NCB Management Services has racked up 644 complaints with the Better Business Bureau (BBB), including 168 complaints that were closed in the last year.

In fact, the BBB states, “BBB routinely advises consumers of pattern of complaints against companies and takes other actions in cases where companies are unresponsive to consumers. However, due to the extreme volume of complaints against this company, only a small sample of the complaints against this company are shown.

All complaints against this company are given to the company for response. All complaints are processed through our automatic system, which contacts the company for a response. Due to the volume of complaints, only 1 out of every 10 complaints processed through our system is shown below.”

On the consumer review website WalletHub, NCB Management Services has an average rating of 1.9 out of 5 stars, with 71% of the reviews being 1-star reviews. The Consumer Financial Protection Bureau (CFPB) complaint database lists over 593 closed complaints against the company for issues like failure to validate debts, repeated calling, and attempting to collect the wrong amount.

In February 2023, NCB experienced a data breach via a ransomware attack that exposed the personal data of roughly 1.6 million consumers, including Social Security numbers, credit card numbers, and account balances. The breach resulted in a class action settlement of $2.625 million that was finalized in September 2025.

Warning Signs of a Problematic NCB Collection Account

While it’s true that you shouldn’t ignore collection accounts without paying them, it’s also true that you shouldn’t pay them without investigating for potential issues first. Some consumers who carefully evaluate their collection accounts discover that the accounts aren’t even valid. Let’s look at a few warning signs that you might have a problematic NCB collection account.

Inconsistent Dates

When you pull your credit report, you can see the date that the original account went delinquent, the date that the creditor charged off the debt, and the date that NCB reported the collection account. If any of these dates don’t make sense, you may have a problem.

For instance, the Fair Credit Reporting Act (FCRA) says that collection accounts can only be reported for seven years from the date of first delinquency. If NCB is reporting an old debt with a new date of first delinquency, that could be a problem.

In fact, federal court records show that NCB has already been sued for this issue. In the case of Chandler v. NCB Management Services, a judge ruled that NCB’s disclosure of the statute of limitations was potentially misleading to the least sophisticated consumer. If NCB is misleading courts about the dates, they might be misleading the credit reporting agencies, too.

Lack of Account Details

If you see a collection account on your credit report, you should see plenty of details about the account. For instance, you should see the name of the original creditor, the original account number, the current balance, and the date of charge off. If you’re missing any of this information, that’s a red flag.

That’s because debt buyers like NCB don’t always get all the details when they buy debt portfolios. While they may have spreadsheet information about your debt, they may not have copies of your original contract or monthly statements.

In fact, several consumers have filed complaints against NCB for this very issue. One consumer on the Pissed Consumer website reported that NCB called repeatedly about a loan the consumer never took out. When the consumer asked for documentation, NCB asked for more information instead of providing proof.

If you don’t recognize the original creditor or the account number, or if the balance doesn’t look right, that doesn’t necessarily mean that NCB made a mistake. However, these types of inconsistencies can be evidence of a larger problem.

Why You May Be Able to Remove Your NCB Collection Account

As you can see, NCB Management Services has a history of problems, from inconsistent dates to a lack of documentation. While these issues can make your life more difficult, they can also create opportunities to remove the account from your report.

The Debt Buyer Documentation Problem

When debt buyers like NCB purchase debt portfolios, they often don’t get the documentation to back it up. Instead, they get a spreadsheet with all the relevant information, but no contracts, no statements, and no proof of anything.

That’s a problem because the FDCPA requires debt collectors to validate debts when consumers request it. If NCB can’t validate your debt, you may be able to dispute the account with the credit reporting agencies and get it removed altogether.

According to PACER, over 200 federal lawsuits have been filed against NCB, mostly for alleged violations of the FDCPA. That suggests that NCB has a problem validating debts when consumers challenge them.

Court Rulings Highlight Systemic Issues

While NCB may be able to validate some debts, federal court rulings suggest that the company has systemic issues that could impact your account.

For instance, in the Barr v. NCB Management Services case, the Supreme Court of the state of West Virginia ruled on allegations that NCB contacted third parties despite the consumer’s express wishes otherwise, accessed credit reports improperly, and attempted to force consumers to pay debts by using other consumers’ credit cards. The judge ruled that consumers do have a private cause of action against NCB in these situations.

Between 2017 and 2018, at least three class action lawsuits were filed against NCB for failure to disclose whether debts would increase because of interest, as well as for providing conflicting information about the amount of the debt. In one Wisconsin class action, the plaintiffs alleged that NCB claimed the same debt was both $610.22 and $562.17.

These court rulings aren’t isolated incidents. Instead, they suggest systemic problems that could affect whether NCB has accurately reported your account. If a judge thinks NCB has a problem, you should, too.

Mistakes to Avoid When NCB Reaches Out

The way you react to a collection agency’s first contact could severely limit your choices later. Your immediate reactions are likely the wrong reactions. Knowing what not to do is as crucial as knowing what to do.

Don’t Take the Bait and Answer the Phone

It’s tempting to answer a debt collector’s call and straighten everything out. Don’t do it. A phone call works entirely in the debt collector’s favor and not at all for you. You won’t have a record of what they say, you can misinterpret their meaning, and you’re at their mercy.

One customer complaint to the BBB said, “I receive 3-4 calls a day every day from a different number.” Another customer told the BBB, “Laura called me and demeaned me by stating things like you can’t even afford 25.00? when I told her I couldn’t afford payments.” You’re playing with fire anytime you engage with a debt collector over the phone.

You’re well within your rights to demand they stop calling you. You can force them to communicate only in writing. That levels the playing field.

The Dangers of Paying Too Soon

Paying what you owe might seem like the simplest way to make a collection go away. Unfortunately, it’s not that simple. Paying a collection changes its status from “unpaid” to “paid,” but it stays on your report just the same. You’ve gained nothing in terms of how that account is viewed by lenders. You’ve also just lost your leverage to negotiate its removal.

Making a payment can even reset the statute of limitations on some debts. Several consumers complained that NCB tried to collect debts that had passed the statute of limitations. If you make a payment on one of those debts, you’ll reset the clock and start the process all over again. One customer reviewing NCB on Wallet Hub wrote, “They bought a debt from another company that was over 7 years old … completely illegal and I turned them in to the CFPB.”

Before you send NCB a single penny, you need to confirm whether the debt is valid and whether it’s too old to collect. You should also explore the possibility of having it removed from your report altogether. Payment should be your absolute last resort.

How to Get NCB Off Your Report

To remove a debt from your credit report, you’ll need patience, persistence, and possibly some expert guidance. It starts with knowing your rights and how to enforce them.

Demanding Validation

The law allows you to demand validation of any debt someone says you owe. This isn’t a courtesy — it’s a legal right. When you properly demand validation, NCB must provide you with written proof that you owe the debt, that you owe the amount they’re claiming, and that they have a legal right to collect it.

The validation process must happen in writing. Not only does a paper trail help you keep track of your dispute, but it also gives you a timeline for your dispute and prevents miscommunication. If NCB fails to validate within the allotted time or fails to provide adequate validation, you can dispute the collection with the credit reporting agency and possibly have it removed from your report.

Several customers have filed complaints against NCB saying the company failed to provide adequate validation when they requested it. In some cases, instead of providing validation, NCB demanded more information from the consumer. That suggests that challenging the company’s right to collect could be an effective way to remove the debt from your report.

The Case for Working with a Pro

When you try to deal with a debt collection agency on your own, you’re at an extreme disadvantage. You have to educate yourself on your rights and the process for asserting them even as you’re trying to navigate it. The debt collector knows exactly what you need to remove the debt from your report and how to avoid giving it to you.

A credit repair expert knows exactly what documentation a collection agency needs to produce and how they’re likely to try to weasel out of producing it. They’ll know when the validation NCB provides is inadequate and how to proceed with your dispute. Most importantly, they’ll provide a layer of insulation between you and the high-pressure tactics of the collection agency.

If there’s one collection on your report that has issues, it’s worth considering the possibility that there are other problems on your report. If the system screwed up one entry, how do you know it didn’t screw up others? A professional may be able to spot errors you didn’t realize existed, giving you the opportunity to clean up your report and raise your credit score.

The Bottom Line

While one or two of these incidents might be a coincidence, the sheer scope of NCB Management Services’ offenses is staggering. From a data breach affecting 1.6 million customers to over 200 federal lawsuits to hundreds of complaints about harassment, errors, and failure to validate, the writing is on the wall. Any entry on your credit report from NCB deserves a raised eyebrow and a healthy dose of skepticism.

Your credit report is a record of your financial responsibility, and you deserve to make sure that only accurate, verifiable information is included on it. The law provides you with numerous protections that few consumers use because they don’t know they exist. NCB Management Services knows those protections exist, and they’re counting on you not to use them.

Don’t let them push you into a reactive response. The debt collection industry makes billions of dollars a year off consumers who react emotionally instead of strategically. You have time. You have options. You have rights.

Take the First Step Right Now

The specialists at FightCollections.com know how to deal with debt collection agencies like NCB Management Services. We understand the games they play with documentation and validation. We understand how to enforce your rights and remove invalid collections from your credit report.

If you see NCB Management Services on your credit report, don’t pay them. Don’t call them. Don’t assume they’re valid. Instead, contact us for a free consultation. Let us evaluate your situation and identify the red flags. Let us help you develop a strategy for removing NCB from your report and improving your credit score.

Contact FightCollections.com today and start the dispute process. The collection currently dragging down your credit score may not survive the scrutiny of a professional. You owe it to yourself to find out.