When you see a collection account on your credit report, your immediate reaction might be to panic and pay it off as soon as possible. That's exactly the reaction debt collection companies hope for.

Before you make that payment, it's crucial to know who is coming after you and where they have historically failed to comply with the law. Knowing their past mistakes gives you powerful leverage against them.

Northstar Location Services, LLC is a debt collection agency based in Western New York. They operate under the trade name The Northstar Companies and have been in operation since March 2001. Northstar collects debt on behalf of several large creditors, including Discover, Barclays, and Ally Financial.

Here is the essential business information for Northstar Location Services:

Understanding Northstar's History of Non-Compliance

What makes Northstar Location Services particularly interesting when it comes to disputing a debt is their long history of litigation. Over 500 federal lawsuits have been filed against Northstar, the majority of which allege Fair Debt Collection Practices Act (FDCPA) violations. This isn't a company that occasionally makes mistakes. This is a company that has a history of non-compliance that creates opportunity for you to dispute their claims.

Between December 2016 and July 2018, at least 14 proposed class-action lawsuits were filed against Northstar. These lawsuits alleged everything from false settlement offer deadlines and misleading IRS tax consequence warnings to failure to clearly state the amount owed and charging illegal fees.

One of those class-action suits, La Caria v. Northstar Location Services, was settled and received court approval in 2021. This means that a federal court has determined that there was merit to the consumers' claims against this debt collector.

The Consumer Financial Protection Bureau (CFPB) has received somewhere between 400 and 470 complaints about Northstar over the years, according to the CFPB Complaint Database, with 117 complaints in just the last year alone, according to more recent data. The most common complaint filed against Northstar is attempting to collect a debt that the consumer doesn't owe. This is a pattern of potentially collecting invalid debts that can serve as the kind of weakness you need to successfully dispute the debt.

Northstar's Documented History of Non-Compliance

Deceptive Collection Letters

The class-action lawsuits filed against Northstar show a particular pattern of problems when it comes to written communication. There have been rulings in court that Northstar sent letters with settlement offers that included deadlines that were not actually enforced. If a debt collector is telling you that you must respond to an offer by a certain date or it will expire and later honors that same offer past the deadline, then the letter they sent you was deceptive.

This is important when disputing a debt because collection letters must accurately reflect the terms they're offering. A letter that creates a false sense of urgency by providing a fake deadline violates the FDCPA's prohibition against using deceptive means to collect a debt. If you received a letter from Northstar that included a settlement deadline, there's a chance that the letter itself was a violation of your rights that can help your dispute.

In the case of Langley v. Northstar Location Services in Texas, the court denied Northstar's motion to dismiss after determining that the debt collector allegedly sent a letter attempting to collect a time-barred debt without informing the consumer that making a payment would revive the statute of limitations. Collecting a debt beyond the statute of limitations without making it clear that a payment would revive the debt is the type of practice that can invalidate a debt.

Wrong Person

A repeated pattern among consumer complaints is Northstar attempting to collect from the wrong person. One of the complaints filed with the BBB describes getting calls for a person who hasn't lived at that address for 62 years. That isn't just a simple administrative error; that is a fundamental failure to verify that you have the right person before attempting collection.

If a debt collector can't even verify that they have the right person, why on earth would you trust that they have verified the correct amount, the correct original creditor, or any other item of information that they're reporting to the credit reporting agencies? Every piece of information that a debt collector reports must be verified and accurate. If they're calling the wrong person, you can be sure they're reporting the wrong person's information to the credit reporting agencies, too.

As one Yelp reviewer put it: "These people are extremely rude, and hang up when they don't get what they want....but they keep harassing me....even though I'm not the person they need to be talking to, and the debt that they are supposedly trying to collect has already been paid!!!"

That combination of wrong-person contact and attempt to collect a debt that's already been paid is exactly the type of inaccuracy that can make disputing the debt successful.

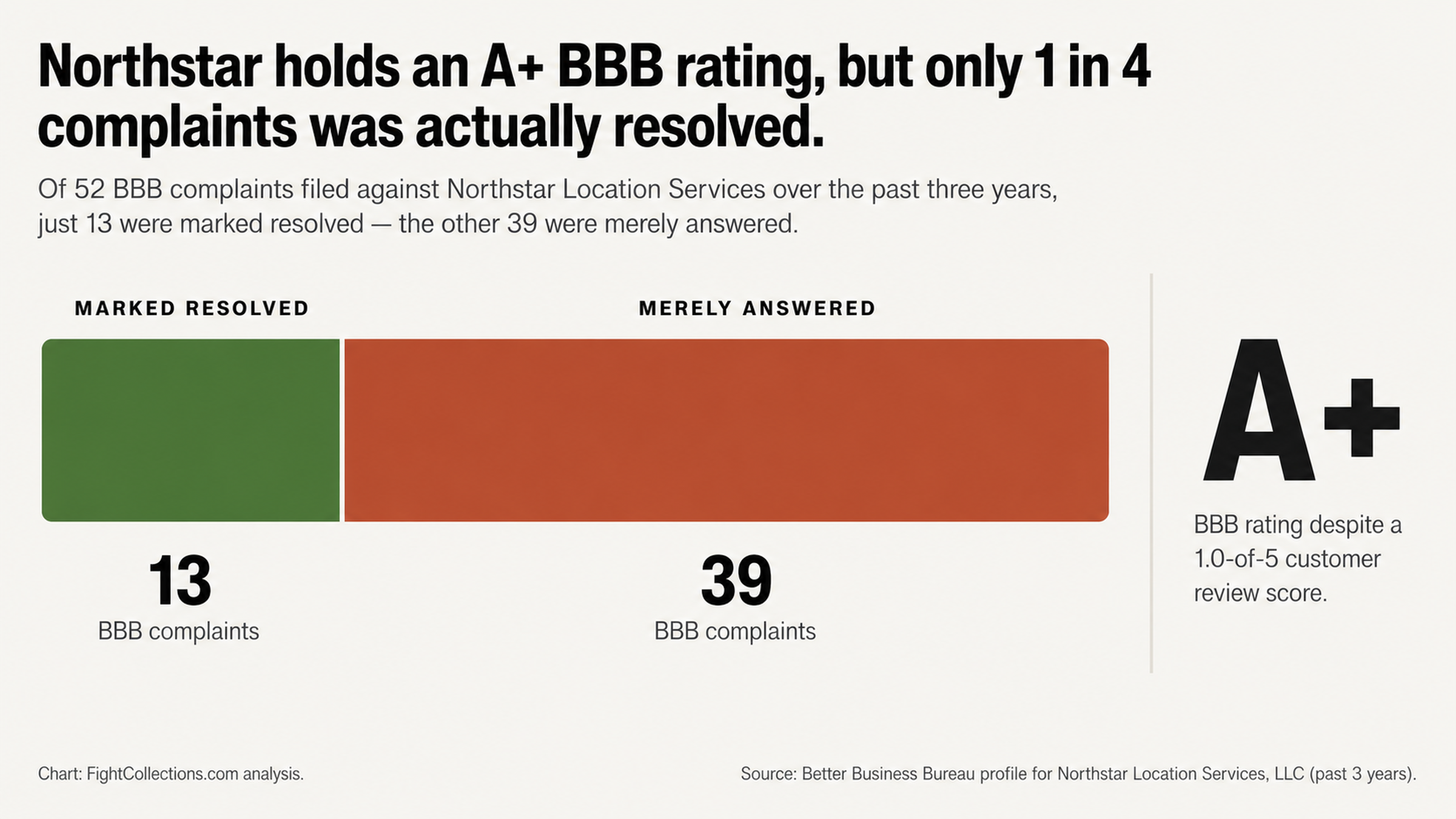

Northstar's A+ BBB Rating

A+ Rating and 1-Star Reviews

Despite hundreds of complaints filed against them with the Better Business Bureau (BBB), Northstar Location Services has an A+ rating and a customer review rating of 1.0 out of 5 stars. This isn't a contradiction; it's how the BBB rating system works and why allowing an A+ rating to lull you into thinking a debt collector has your correct information is a mistake.

The BBB rates businesses based primarily on whether they respond to complaints rather than whether those responses actually resolve the consumers' problems. Northstar has had 52 complaints filed against them in the past three years alone, according to the BBB's records. Of those 52 complaints, only 13 were listed as "resolved." The other 39 were merely "answered." Answering a complaint isn't the same as resolving it and having the right information about the consumer.

In fact, the company isn't even accredited by the BBB, meaning they haven't pledged to comply with the BBB Standards for Trust or gone through the BBB accreditation process. They have an A+ rating solely because they answer complaints, not because they're showing signs of ethical business practices and accuracy in their record-keeping.

What the Consumer Complaints Say About the Documentation

The content of the complaints filed through the BBB provides insight into the types of documentation weaknesses Northstar may have.

One complaint filed in May of 2025 says: "I demanding a cease and desist order!!! Ya'all been harassing me and my family everyday. WE do NOT owe any debt to anyone!"

Another complaint filed in September of 2025 alleges elder abuse and harassment of the next of kin.

These complaints describe a debt collector that isn't verifying relationships or the validity of debts before aggressively pursuing consumers for payment.

Credit repair experts who have worked with consumers that Northstar is pursuing estimate that about 40 percent of Northstar cases involve either an incorrect balance or a debt that isn't valid at all. That error rate is consistent with other studies that have been done on the overall accuracy of credit reports, which show that credit reports frequently contain mistakes. If nearly half of the debts that Northstar is pursuing could potentially be incorrect, that means the odds are ever in your favor if you choose to dispute rather than pay.

Why Disputing the Debt Works

The Burden of Verification

Federal laws like the Fair Credit Reporting Act (FCRA) and the FDCPA aren't just laws designed to protect you; they're also laws that give you the opportunity to fight back. When you dispute a collection account on your credit report, the collection agency is required to verify the debt. They must prove that they have the right person, the right amount, and the legal right to collect it.

That's a burden that a company that has been sued more than 500 times for violating consumers' rights under the FDCPA may struggle to meet. Every class-action settlement and every ruling in consumers' favor is a sign of systemic problems with Northstar's documentation and processes. If they could easily verify all of their debts, they wouldn't keep losing in court. The burden of verification is one that you can use to your advantage when disputing the debt.

The Economics of Debt Collection

Debt collectors purchase debt portfolios that contain thousands of individual accounts. They pay mere pennies on the dollar for those debts. That means investing the time and money necessary to verify and document a single disputed debt often costs more than the debt is actually worth.

If a debt collector must pay to thoroughly document the debt, legally review all processes, and validate every step of the way, they'll likely decide it isn't worth their time and expense.

The Lawsuit That Probably Won't Come

Many consumers pay collection accounts because they're afraid the debt collector will sue them if they don't. In most cases, that fear is unwarranted. Before a debt collector files a lawsuit, they conduct a cost-benefit analysis to determine whether the debt is worth their time and expense. For most debts, the answer is no; filing a lawsuit costs too much for the return they're likely to see. The threat of a lawsuit is just that—a threat designed to get you to pay without taking the time to dispute the debt.

Northstar has been the defendant in more than 500 federal lawsuits. They know exactly how much money it costs to litigate. They know that it costs too much to pursue most debts. When you force them to verify a debt, you're forcing them to decide whether this particular debt is worth that cost. Don't assume they'll come after you with a lawsuit. Assume they'll decide it isn't worth the cost and give up.

One complaint filed with the BBB includes a threat from a debt collector: "The caller also told me, 'I know it's [name], we will destroy your credit if you do not respond.'" That kind of threat is designed to bypass your rational thinking and force you to react out of fear. When you recognize these tactics for what they are, you can respond strategically rather than reacting emotionally.

Why You Shouldn't Pay

Paying the Debt Doesn't Make it Go Away

Perhaps the most significant mistake consumers make when they find a collection account on their credit report is assuming that if they pay it off, the account will be removed. When you pay a collection account, you're not deleting it; you're simply changing its status from unpaid to paid. The collection account will still remain on your credit report for seven years from the original delinquency date.

A paid collection is still a collection, and it still tells anyone looking at your credit report that you had an account go to collection.

When you pay a debt, you're also giving up your leverage. Once you've paid, you've acknowledged that the debt is valid and you've lost the right to dispute its accuracy. If there were documentation or verification issues or compliance problems that would have resulted in having the account removed, you've just forfeited those opportunities. You've essentially agreed that the debt collector did nothing wrong, even if their processes were completely flawed.

The "don't pay" warning that you find repeated throughout consumer advocacy materials is there because most people will default to paying when they find a collection account on their credit report. The impulse to pay to "do the right thing" and resolve the situation feels responsible. In reality, it often results in worse outcomes than a strategic dispute would have provided.

Why Remaining Silent Is Often the Smartest Response

Engaging with a debt collector directly puts you at a disadvantage. This is what they do for a living; they know exactly what to say to get you to do what they want. They'll get you to commit to paying, acknowledge that you owe the debt, or provide information that helps their case against you. The information imbalance when you speak directly with a debt collector always tips in their favor.

When you work through a professional dispute process, you avoid engaging in a conversation where the debt collector controls the dialogue. Instead, you shift the interaction to the documentation and shift the burden to the debt collector. Every piece of information that they cannot produce and every verification they cannot complete is one more reason to dispute the debt successfully.

It is possible to have a collection account removed when the information is incorrect, when the debt collector cannot verify within the allotted time frame, or when the account is fraudulent. The path to removal lies through the dispute process, not the payment process. Choosing the right process at the outset means that you have more possible outcomes in your favor.