Do you have a ProCollect collections account on your credit report? While any unknown collection account can be scary, ProCollect has a history of regulatory issues and extensive litigation.

So, before you pay ProCollect, you need to know what you're really dealing with.

In this article, you'll learn how to identify the warning signs that something is wrong with your ProCollect credit report entry. You'll understand why you should ignore conventional wisdom about paying collections, and you'll discover the one approach that's guaranteed to get results. And you'll learn why having professional help is always the best option.

ProCollect

ProCollect, Inc. is a third-party debt collection agency. They work with creditors to collect outstanding debts. Some of their clients include multi-family housing, student housing, medical providers, and utility companies.

Here's some information you may find helpful:

What is the Record on ProCollect?

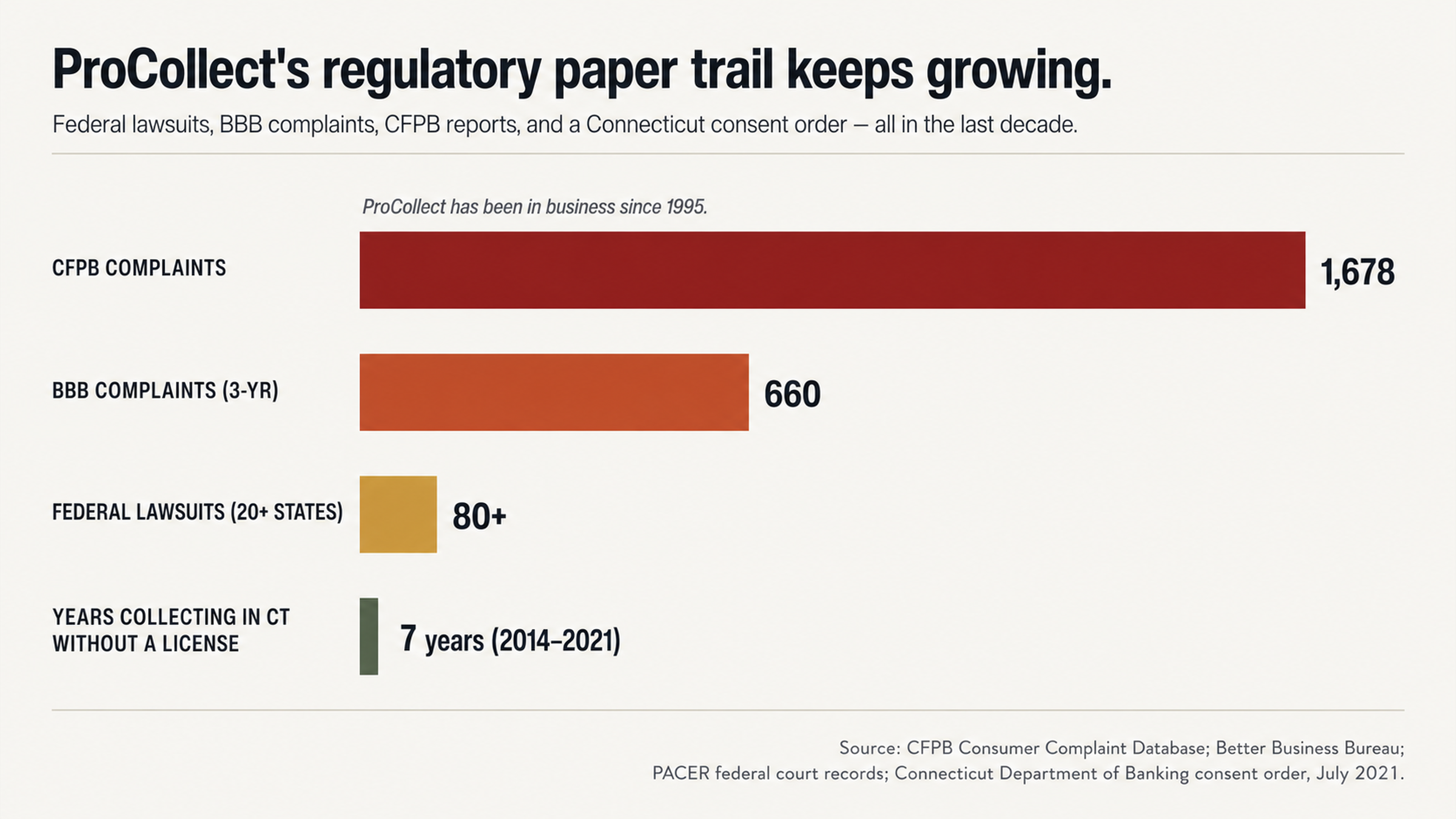

ProCollect has a history of regulatory issues. In July 2021, the Connecticut Department of Banking issued a consent order to the company after they found that ProCollect had been collecting debts from Connecticut residents without a license for seven consecutive years (2014-2021). The company paid $12,800 in penalties and back licensing fees.

Federal court records reveal that more than 80 lawsuits have been filed against ProCollect across over 20 states. Most of the suits involve alleged violations of the Fair Debt Collection Practices Act.

The Better Business Bureau reports 660 complaints against ProCollect in the past three years alone. The company has a B- rating and is not accredited by the BBB. The Consumer Financial Protection Bureau reports over 1,678 complaints, with half of them related to billing or collection issues.

Warning Signs Something is Wrong

ProCollect's history is concerning, but that's not enough to assume something is wrong with the account on your credit report. You have to dig into your report to identify potential issues. In fact, studies from U.S. PIRGs show that 79% of credit reports contain errors or other serious issues. It's safe to assume your report could have errors, too.

Suspicious Dates and Timeline Issues

One of the first things you should look for are suspicious dates. The date of first delinquency, for example, will determine how long the account can remain on your credit report. But collectors often report the wrong date, which can extend the amount of time they have to collect the debt. If the date of first delinquency seems off or is more recent than you think it should be, that's a red flag.

You should also look at the "opened" date. Is that correct? Were you even living at that address when the account was supposedly opened? In one consumer review, the author explains that ProCollect contacted them about a debt from an apartment complex in a city where they'd never lived:

"I have not lived in the United States since 2018, I have a passport to prove this."

Missing Information

Debt collectors don't always have the paperwork to prove you owe the debt they're reporting. When debts change hands multiple times, paperwork can get lost or corrupted. Sometimes critical verification paperwork goes missing altogether. This creates a knowledge gap that you can exploit to your advantage.

As you review the account on your credit report, look for missing information. Does the account description seem vague? Is there no information about the original creditor? Does the balance seem off? In one complaint filed with the BBB, the consumer explains that ProCollect was reporting a debt without a signed contract or any other valid agreement:

"I requested that they validate the debt. They have yet to provide any documentation."

Why Your First Move Shouldn't be to Pay

When you see a collection account pop up on your credit report, it's tempting to pay it right away to make it go away. That's what the collectors are hoping for. But before you do that, take a step back.

The Hidden Problem with Paying a Collection

The thing is, paying a collection can actually make your credit worse. When you pay a collection account, you're updating the status of the account from "unpaid" to "paid." But the account remains on your report for the full seven years. You paid the money, but the damage remains.

Paying a collection can also renew the statute of limitations, which can give collectors more time to sue you for the debt. So, what you thought was putting the problem behind you may have just opened you up to more collection activity.

Information Asymmetry

Collectors understand how this works, but most consumers don't. There's an information asymmetry here that collectors exploit to their advantage. They know how the system works, and they're using that knowledge to get you to pay up.

Financial Stress

Collectors are also trained to use financial stress to their advantage. When you're in a state of stress about money, you don't think as clearly. And that's exactly what they're counting on. Debt collectors know how to apply just the right amount of pressure to get you to do what they want.

If you're worried about an impending credit check for a job, an apartment, or a loan, you're not thinking clearly. And the collectors will use that to their advantage.

Consumers have reported that ProCollect representatives use pressure tactics to get them to pay. Here's one example from a consumer review:

"When I asked her a question about this debt she told me I had until [specific date] to pay this debt or else, and that if I did not pay it she was going to mark this account as 'refused to pay' simply because I had questions."

In another review, the consumer explains how the representative responded when they tried to report identity theft:

"She said, 'Well if you didn't do it, why are you calling all upset about it?'"

Understanding Your Rights

So, what are your rights when dealing with a debt collector? Under federal law, you have significant protections, but you have to understand how to use them.

The FCRA

Under the Fair Credit Reporting Act (FCRA), you have the right to dispute any information on your credit report that you believe is inaccurate, incomplete, or unverifiable. When you file a dispute, the credit reporting agency has to investigate and remove any information they can't verify. That means the burden of proof is on the collector.

You also have the right under the FCRA to expect that information reported to the credit bureaus about you is accurate and complete. When collectors report debts without the proper paperwork, or when they use the wrong dates, or when they attribute debts to the wrong person, they may be violating the FCRA. And you can use those violations as the basis for removing the account from your report.

The FDCPA

The Fair Debt Collection Practices Act (FDCPA) says that debt collectors can't harass you, make false statements, or engage in other unfair practices. More than 80 federal lawsuits have been filed against ProCollect, alleging violations of the FDCPA, including harassment (Section 1692d), false representations (Section 1692e), and failure to validate debts (Section 1692g).

Under the FDCPA, collectors have to verify your debt if you request it within 30 days of the initial contact. They can't keep trying to collect until they verify the debt. The problem is, many collectors don't have the verification paperwork, because it was never included in the debt portfolio they bought.

The Right Dispute Strategy

If you're going to dispute the debt, you have to do it right. That means understanding the economics of the debt collection industry. When collectors buy debt portfolios, it's often for pennies on the dollar. But pursuing validation of a debt costs money. Court costs, paperwork, man hours — it all adds up. And sometimes, it costs more than the debt is worth.

So, when collectors are faced with a request for validation, they have to decide whether pursuing that validation is worth the cost. Sometimes, the path of least resistance is simply to delete the debt.

Why Collectors Can't Verify

Collectors often can't verify because they don't have the paperwork. When debts get sold and resold, paperwork goes missing. Sometimes the original contract and signed agreement are lost. Other times the payment history is corrupted or incomplete.

In their reviews, consumers have noted that ProCollect often can't provide adequate verification:

"They are refusing to provide me the adequate debt validation documentation for this debt."

The company is "collecting a debt from the wrong person."

When the consumer tries to explain they have the wrong person, the representatives hang up the phone:

"They have hung up on me three times while I was attempting to give them proof that I am not the correct person."

Why You Need Help

If you're going to navigate the dispute process successfully, you need to understand the nuances of the FCRA and FDCPA. You need to understand what collectors are looking for and how to exploit the system to your advantage. Most importantly, you need professional help in your corner.

The Nuances of Procedure

If you want a dispute to succeed, you need to understand the procedure correctly. There are timelines and specific wording that has to be used. There's specific documentation you need to request and a specific way you have to request it. If you don't get it just right, your dispute may fail.

Professionals who work in credit repair understand those nuances because they do this kind of work every day. They can help you craft a successful dispute and give you a much better chance of getting the desired outcome.

The Collector's Playbook

Credit repair professionals also understand the games collectors play. They recognize the stall tactics and know which responses mean the collector is on weak ground. They know how to escalate a dispute if the initial efforts are met with resistance. And they know how to keep pushing until they get the results you need.

Emotional Distance

Finally, professionals can help you maintain the emotional distance you need from this process. When collectors push and prod, trying to get a rise out of you, they're talking to your advocate, not to you. That means you don't have to deal with the manipulation.

In consumer reviews, people have talked about how ProCollect representatives use phrases designed to get an emotional rise out of people:

"Representative became very rude and threatening when I started asking questions."

The representative "muted me for over 10 minutes instead of assisting me."

Conclusion

If ProCollect is on your credit report, don't panic and don't pay until you've taken a closer look. The company has a history of regulatory issues, extensive litigation, and many consumer complaints. Not every debt is necessarily valid or properly documented. It's up to you to verify before you validate their claims by paying them money.

The red flags here — from suspicious dates to missing documentation to pushy collection representatives — all point to the same thing. You should always dispute first and ask questions later. Sometimes, saying nothing at all is the right strategy.

Ready to get started? Contact us at FightCollections.com for a free consultation. Our advocates can help you review your report, identify the red flags in your ProCollect listing, and help you craft a strategy to pursue removal. Your credit report tells the story of your financial history. Make sure it's an accurate one.