Radius Global Solutions can be alarming to find on your credit report. But there’s no need to panic.

In this article, you’ll learn exactly who Radius Global Solutions is and how you can protect your legal rights. Debt collection agencies are out to scare you. Before you pay or respond, take a moment to educate yourself.

In this article, we’ll cover:

- A history of the company

- A list of complaints against the company

- How to verify debts

- What federal law says about your rights

- Why you should always dispute before paying

Don’t make a payment or respond before reading the rest of this article. Debt collectors profit from fear and urgency. By the time you finish reading, you’ll know exactly how to handle Radius Global Solutions.

Who is Radius Global Solutions?

Radius Global Solutions is a debt collection agency with 4,000 employees in 14 offices throughout the world. Their offices are in Jamaica, Panama, India, the Philippines, and Colombia. They collect on medical debt, utilities and telecom debt, financial services debt, and government debt.

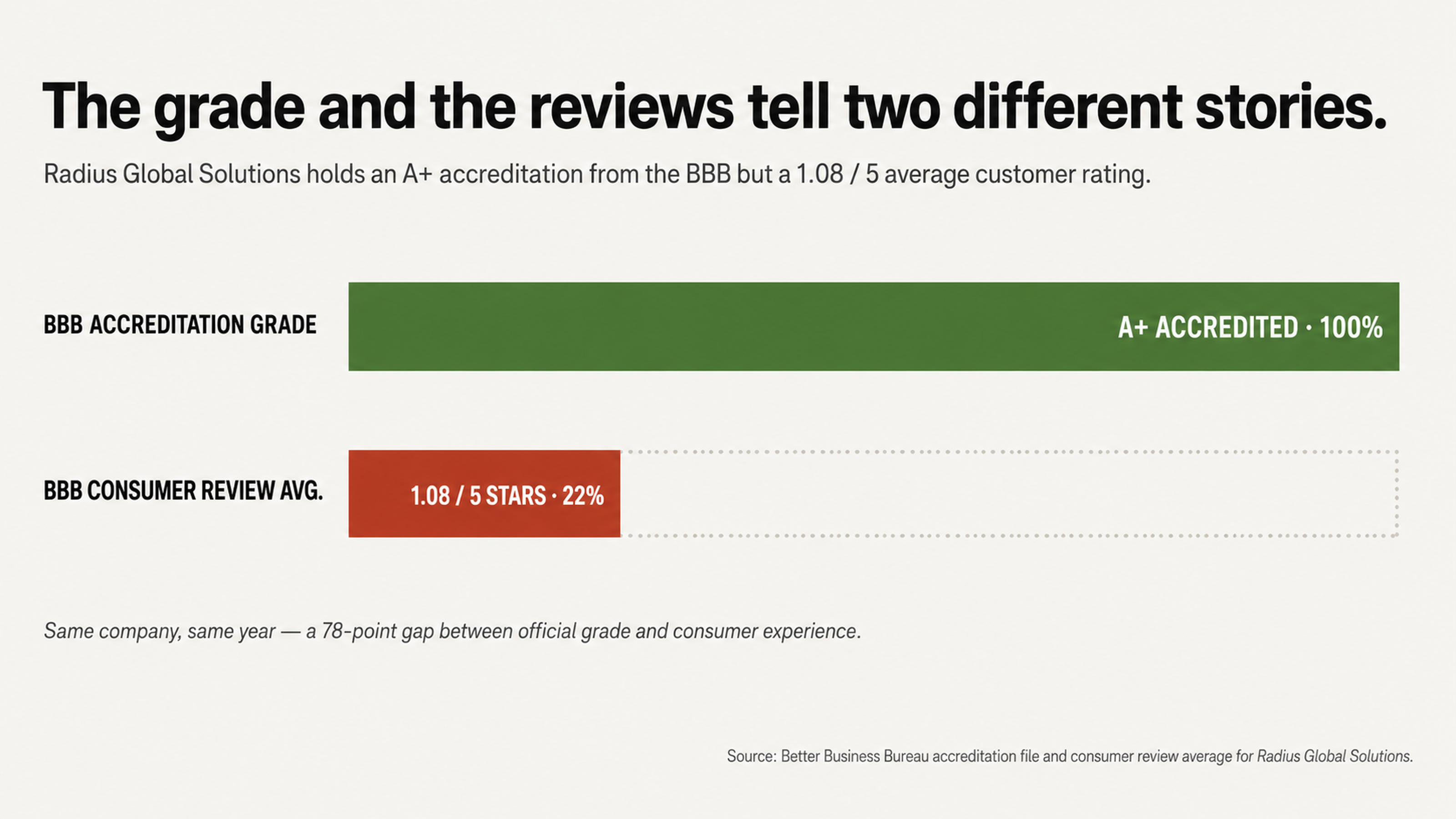

The company has an A+ rating with the Better Business Bureau (BBB), but their reviews aren’t as promising. The BBB gave them an average rating of 1.08 out of 5 stars. We can’t stress enough the importance of looking beyond a company’s ratings and reading the reviews.

Michael Barrist is the chairman of Radius Global Solutions. Previously, he was the CEO of NCO Group, which paid a record $3.2 million to the Federal Trade Commission (FTC) in 2012 for violating debt collection laws. Barrist’s company called consumers too many times a day and called them even after consumers asked them to stop.

What are the complaints against Radius Global Solutions?

The Consumer Financial Protection Bureau (CFPB) has received over 1,000 complaints about Radius Global Solutions in the last few years. In the last three years alone, 630 complaints were filed against the company. In January 2023, the Connecticut Department of Banking entered a consent order against the company. The consent order required the company to pay a civil penalty of $10,000 for attempting to collect debts from consumers while operating from foreign locations without a license.

What are your rights under federal law?

The Fair Debt Collection Practices Act (FDCPA) is a federal law that prohibits abusive debt collection practices. Here are a few of your rights under the FDCPA:

You have the right to request proof of a debt in writing. The company must send you the amount you owe, the original creditor, and the date of your last payment in writing. The company cannot continue to collect the debt until they send you this information.

The FDCPA has been used against Radius Global Solutions in the past. Court records show the company has been involved in at least 40 federal lawsuits. Many of the cases were for violations of the FDCPA. Some examples include failure to properly disclose rights to dispute a debt, using improper envelope markings in collection letters, and displaying the original creditor’s name when they were supposed to keep it private.

How to dispute a debt

If you write to the collection agency to dispute a debt, the burden of proof is then on the agency. They must then verify the debt, which means they need to show the amount you owe is correct, the debt has not passed the statute of limitations, and you are the correct consumer who owes the debt. Many agencies do not have the proper documentation, so this is when your rights come in handy.

The credit reporting agencies also have their own set of federal laws to follow. If the agency cannot verify the debt within a reasonable amount of time, the credit reporting agency must remove the item from your credit report. This is not a loophole. This is the law.

Why paying immediately can backfire

Some consumers assume that paying a collection will fix their credit. In some cases, it doesn’t. When you pay a collection, the status of the collection is changed from “unpaid collection” to “paid collection.” However, the negative mark will still be on your report for up to seven years from the original delinquency date.

In many credit scoring models, a paid collection will hurt your credit just as much as an unpaid collection. The derogatory mark will still be there, so it’s best to dispute it first. If the collection agency cannot verify it, or if the information is incorrect, it may be deleted without having to pay.

How to avoid the error trap

It’s estimated that 79 percent of credit reports have errors or discrepancies. It’s extremely important to check your report for errors before paying a collection agency.

Some of the most common complaints against Radius Global Solutions is for attempting to collect debts that are not owed. One consumer posted a complaint on the BBB’s website and said, “The name and phone number belonged to me, but they assigned it to someone else with the same first and last name.” Another consumer had the same issue.

What do collection agencies not want you to know?

Don’t answer the phone

One of the most effective tools in dealing with a collection agency is not to answer the phone. Many collection agencies will call several times a day and rotate phone numbers so you cannot block them.

One consumer posted on the website Pissed Consumer and said, “These people call me every day twice a day and they are rotating through phone numbers.” Don’t answer the phone. Instead, send them a letter and make them put it in writing.

Don’t fall for fake authority

Many collection agencies will pose as attorneys or government representatives. The CFPB has received complaints about Radius Global Solutions for impersonating attorneys or government officials.

Legitimate collection agencies will never pose as someone they are not. They also will never threaten to sue you if they don’t intend on doing so. If a collection agency calls posing as an attorney or government official, or threatens to sue you, make sure you get it in writing and take note of the conversation.

How to use your free credit reports as intelligence

Your free credit reports are exactly what they sound like: free. You can request a free credit report from each of the three credit reporting agencies (Equifax, Experian, and TransUnion) once a year.

It’s a good idea to request a credit report from each agency because they may have different information on you. Check each report for:

- Different account numbers

- Different balances

- Different dates

- Different creditor names

Anything that is different between what the collection agency has on you and what your report says may be a reason for disputing the debt.

Collections can be removed from your credit report if:

- The information is not accurate

- The debt is past the statute of limitations

- The account is fraudulent

- The collection agency cannot verify the debt within a reasonable amount of time

Your free credit report can help you determine if any of these reasons exist.

What to do if a collection agency has changed balances

Some consumers have complained that Radius Global Solutions is reporting inaccurate balances. One consumer posted a complaint on the BBB’s website in 2023 and said, “They are reporting new higher numbers to my credit every month which is not even close to legal.”

If the balance has been changed, it may be a good idea to dispute it.

The data breach factor

In May 2023, Radius Global Solutions suffered a data breach that affected 632,204 people. The breach included Social Security numbers, dates of birth, health insurance provider information, treatment payment history, and patient treatment codes.

The breach is not only a concern for identity theft. If a collection agency has suffered a breach, it may be a sign that their records are not accurate. If they cannot protect data, can you trust that your information is accurate?

Following the breach, several law firms across the country began investigating class action suits. The agencies said they are investigating claims for people who were affected by the breach. Patient treatment codes and treatment payment history were compromised in the breach.

How to protect yourself

If you were affected by the breach, you should monitor your credit report closely. The data that was compromised is the exact data needed to commit identity theft and open new credit accounts.

If you see any new accounts or inquiries that you did not initiate, you should report it immediately to the credit reporting agencies and the Federal Trade Commission.

You may also want to consider placing a fraud alert or credit freeze on your accounts. This will make it more difficult for someone to open a new account using your information, and if there’s an issue in the future, you will have a paper trail.

Why professional help matters

If you have a collection on your report, it may be a good idea to get a professional to help you. A credit repair professional can help you understand your federal and state rights and can help you navigate the process.

According to the CFPB, only .2 percent of complaints against Radius Global Solutions were closed with monetary relief. Sixty-seven percent were closed with an explanation.

If you are going to dispute a collection, it’s a good idea to get help. A credit repair professional can help you understand your rights and understand how to identify violations. They can also help you write an effective dispute letter and negotiate on your behalf.

What does a credit repair professional do?

A credit repair professional can:

- Understand your rights

- Identify violations

- Negotiate with collection agencies

- Escalate claims when necessary

If you hire a credit repair professional, you also won’t have to speak directly with the collection agency. This means you won’t accidentally validate a debt, restart the statute of limitations clock, or give them information they can use against you.

You don’t have to face Radius Global Solutions alone. FightCollections.com is a team of professionals who will dispute the debt on your behalf and negotiate with the collection agency. Contact us for a free consultation.