What is Receivables Management Partners, LLC?

Receivables Management Partners, LLC (RMP) is a third-party debt collection agency. They operate in 46-48 states and serve over 200 hospitals and 30,000 physicians. RMP primarily collects medical debt and works as an agent on behalf of healthcare providers.

They are a subsidiary of Meduit, a healthcare revenue cycle management company that is owned by private equity firm NexPhase Capital. They also operate under the names RMP Services, RMP, LLC, and JP RMP.

Despite their A+ rating with the Better Business Bureau, RMP has over 1,200 complaints registered with the Consumer Financial Protection Bureau and more than 50 federal lawsuits against them for violating the Fair Debt Collection Practices Act.

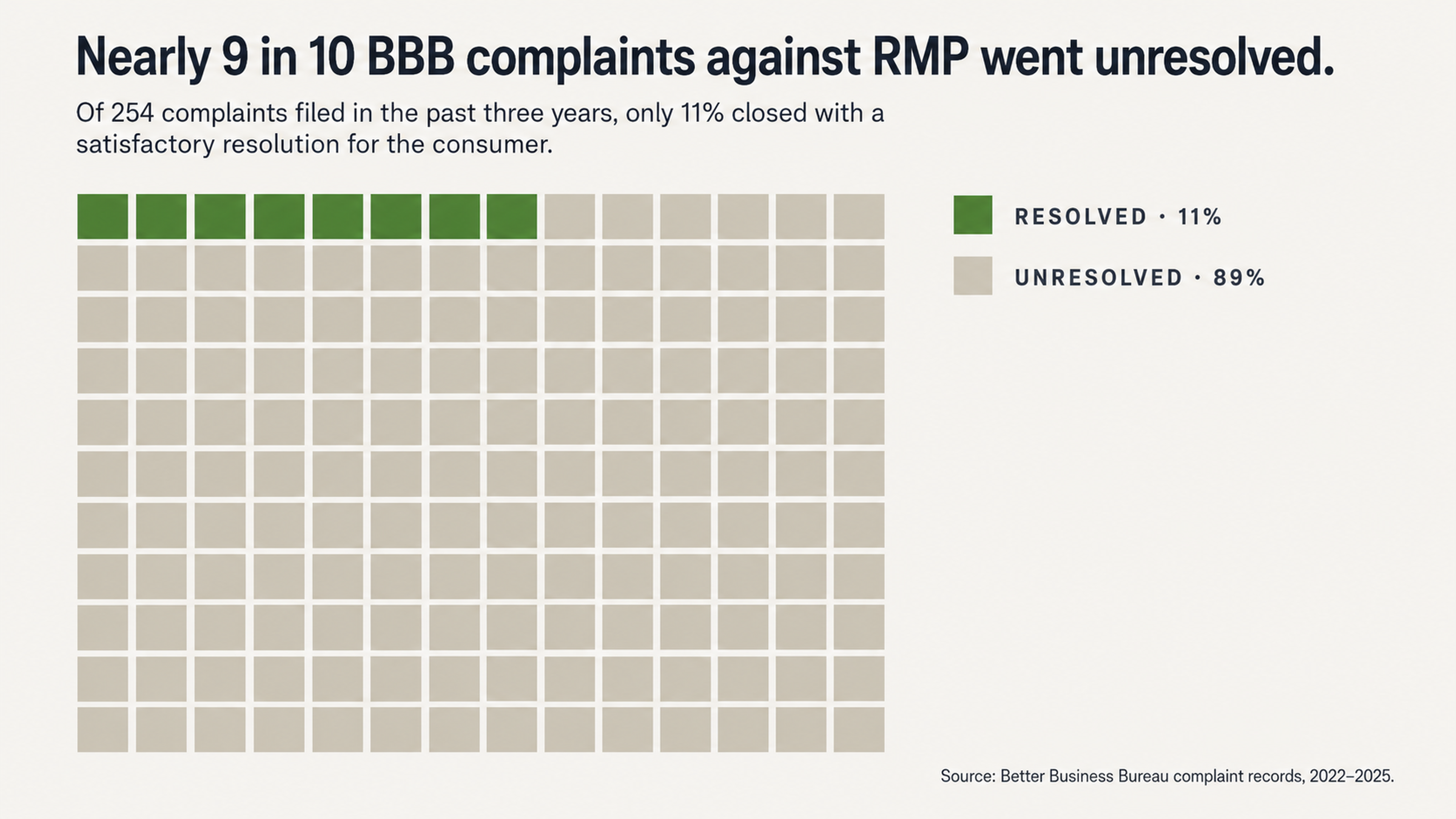

Their BBB page shows a 1.17-star customer rating (out of 5 stars) with only 11% of the 254 complaints they’ve received in the last three years resulting in a satisfactory resolution for the consumer.

The most common complaint categories for RMP surround disputed bills, customer service issues, and problems with how orders are handled.

A History of Litigation and Lawsuits

The details of several federal lawsuits against RMP give insight into the nature of some of the problems they have.

For example, the 2017 class action Rhoads v. Receivables Management Partners alleged the collection letters sent by RMP contained different amounts for the same debt, though without an explanation for the discrepancy. The letter supposedly stated one amount as the current balance due but then indicated a different amount for the same account.

In cases like this, it’s clear where a consumer might have grounds to dispute a collection account.

What do Debt Collectors Have to Prove?

In order to collect a debt, a debt collection agency has to prove several things.

They have to establish their right to collect the debt, prove the debt is valid, and show they have the authority to collect it.

To do that, they need to provide the name of the original creditor, the amount of the debt (including an itemized accounting), the date of the last payment or activity on the account, and proof they have the right to collect the debt.

When it comes to medical debt collection, it can be even more complicated because the billing process often involves insurance adjustments, charity care, and coding errors, all of which lead to frequent discrepancies.

Requesting verification of a debt isn’t an admission you owe it. It’s a right provided to consumers under the Fair Debt Collection Practices Act (FDCPA), and exercising that right means the collector must cease all collection activities until they can provide the necessary documentation.

Why Incomplete Records Happen So Often

The reason incomplete records are so common with medical debts is the number of hands the account has to pass through before it ends up at a collection agency.

Hospitals and healthcare providers will sell or assign accounts to a collection agency, sometimes in batches that contain thousands of accounts.

With each transfer, there’s an opportunity for data to be lost or corrupted, or perhaps the information was never transferred in the first place.

Though RMP mostly collects debts on behalf of healthcare providers rather than debt they purchased themselves, many of the complaints against them include allegations of attempting to collect debts that were already paid, debts in the wrong amount, or debts that don’t belong to the consumer at all.

Looking at CFPB complaint data, the top reasons consumers complain about RMP include: Claims they don’t owe the debt, Attempts to collect the wrong amount, and Failure to provide enough information to verify the debt.

This isn’t a problem unique to RMP. According to U.S. PIRG, 79% of credit reports contain errors or other serious mistakes.

When a debt collector reports inaccurate information to the credit bureaus, those errors can multiply.

Why Paying a Collection Doesn’t Help

One of the reasons consumers end up paying collection agencies is they believe it will help repair their credit.

Unfortunately, paying a collection doesn’t work that way.

When you pay a collection, the account status will be updated to reflect that fact. But it will still remain on your credit report for the full 7 years.

Having a paid collection on your credit report still indicates to lenders you had an account that became delinquent and went to collections.

The damage has already been done.

While some newer credit scoring models don’t count paid collections against you, many lenders still use older models where paid and unpaid collections are treated the same.

Paying can also reset the statute of limitations.

In some states, when you make a payment on an old debt, you can reset the clock on the statute of limitations. This gives the collector a brand-new window in which they can legally sue you for the debt.

You might also reset the clock on the credit reporting period. In some cases, a payment can restart the 7-year clock for credit reporting.

All of this is why it’s so important to dispute first and negotiate later.

The Power of Time

Every state has a statute of limitations (SOL) that governs how long a creditor or collector can sue you to collect a debt.

Once the statute of limitations has expired, the debt is time-barred. Collectors can still attempt to collect, but they’ve lost the big gun.

The older a debt gets, the less likely a collector is to file a lawsuit because it simply isn’t cost-effective.

At the same time, documentation becomes harder to track down. Files get lost. Computer systems get replaced.

That’s why older debts are frequently very good candidates for a successful dispute.

What Do Consumer Complaints Say About RMP?

BBB reviews for Receivables Management Partners include several common themes.

One consumer wrote in 2025 that RMP had been texting them pictures of their bills with their private health information (PHI) on them. The consumer stated they never gave RMP permission to text them at all.

Another consumer reported calling RMP regarding a bill they felt should have gone through their insurance. According to the consumer, RMP was supposed to have tried to bill their insurance again but instead reported them to the credit bureau.

A third consumer stated they were receiving daily automated voice messages from RMP regarding a past due medical bill. After speaking with the hospital’s billing department twice, each time the hospital confirmed with the consumer they owed no balance.

The consumer noted they had received in excess of 7 calls within a 7 day period, which could be a potential violation of CFPB Regulation F.

Why Consumer Complaints Matter to Your Case

Complaints like these indicate there may be systemic problems with verification and accuracy.

When a collection agency reports debts that the hospital cannot verify, or when they attempt to collect accounts that should have gone through insurance, it may indicate a problem with their documentation process.

Those are the kinds of weaknesses a well-drafted dispute letter can exploit.

The collection industry survives because consumers don’t understand their rights and/or don’t take the time to dispute collection accounts they don’t think are accurate.

When you realize verification is a requirement and errors are common, you begin to gain the upper hand. The burden of proof is on the collector. All you have to do is ask the right questions.

How to Dispute a Collection Account

Disputing a collection account effectively requires targeting the right information.

You want to challenge the amount they claim you owe, whether the debt is really yours, whether the statute of limitations has expired, whether they followed the proper procedure when the account was transferred, and whether they have access to the original paperwork from the original creditor.

Credit bureaus have 30 days to investigate a dispute. If the collector cannot verify the disputed information during that time, the item must be deleted from your credit report.

Collections for which the collector has incomplete records frequently fail the verification process. That’s because the collector doesn’t have the records to back up their claims.

Your dispute should be specific, not generic. Say exactly which information you believe is inaccurate. Request a complete payment history, the original signed contract, proof of assignment, and any other documentation the collector would need to validate their claim in court.

Why You Need Professional Help

Successfully disputing a collection account requires knowledge of the law and the games collectors play.

Advocacy firms that specialize in credit disputes have dealt with thousands of consumers and thousands of different collection accounts. We know where the documentation process tends to break down and how to craft a dispute that will expose those weaknesses.

We also know how to push back when the initial response from the credit bureaus or collectors isn’t satisfactory.

You can try to navigate the process on your own, but you’ll be at a disadvantage. Collectors understand the law and the deadlines. They understand most consumers will either pay them because they’re afraid or ignore them and suffer the consequences.

When you hire a professional, you level the playing field. You bring the same expertise to your side of the dispute.

Trying to learn how to do this on your own can be expensive. You make a partial payment that restarts the statute of limitations. You admit to the debt over the phone. You miss a deadline and wipe out one of your defenses.

All of those individual mistakes can dog you for years in the form of a collection account on your credit report.

The Bottom Line

Receivables Management Partners, LLC, has a business model built around collecting medical debts, but their history indicates there may be a significant disconnect between the debts they attempt to collect and their ability to document those debts properly.

Over 1,200 complaints with the CFPB. More than 50 federal lawsuits. An 11% resolution rate with the BBB.

You don’t have to accept a collection account like this at face value. You have the right to request verification, and collectors have the obligation to provide it. When they can’t meet that burden, the collection account can be deleted from your credit report altogether.

Silence and strategic disputes are far more effective than panic payments. The documentation trail is where the collection industry is most vulnerable, and a well-crafted dispute can force them to prove what they may not be able to prove.

Don’t wait any longer. Contact us at FightCollections.com today for your FREE credit report review.

Our team will help you uncover errors and disputes, challenge questionable collection accounts, and negotiate with collectors when possible to remove unverifiable accounts.

Every month an unverified collection account sits on your credit report is another month it could be holding you back from the loans and interest rates you deserve. Don’t wait. Reach out to us at FightCollections.com to start the dispute process today.