Dealing with Source Receivables Management is the last thing you want to see on your credit report. You likely didn’t know that the account even existed, until you were denied for credit that you needed.

The truth that the collection industry doesn’t want you to know is that this single entry alone can lower your credit score by 100 points or more. And in many cases, it can stay on your report for up to 7 years, regardless of whether you pay or not. The fact that you owe money to someone, somewhere is not the issue. The credit report is the battlefield, and the outcome is completely dependent upon what is reported on it, and how long it stays there.

Source Receivables Management and other collection agencies hope you don’t know the difference. This article will discuss the secret information that the collection agencies are trying to keep from you. Once you realize where the power truly lies in this process, you will never be a victim again.

Who is Source Receivables Management?

Source Receivables Management, LLC, is a third-party debt collection agency located in North Carolina. Founded on March 11, 2008, SRM collects debts for telecommunications companies, healthcare providers, utilities, multi-family housing providers, and financial services companies.

Here is some basic information on the company:

SRM also goes by the trade names SourceRM and SRM. According to their website, they are licensed in all 50 states, and collect for Sprint and T-Mobile accounts, among others.

What does the complaint record say about Source Receivables Management?

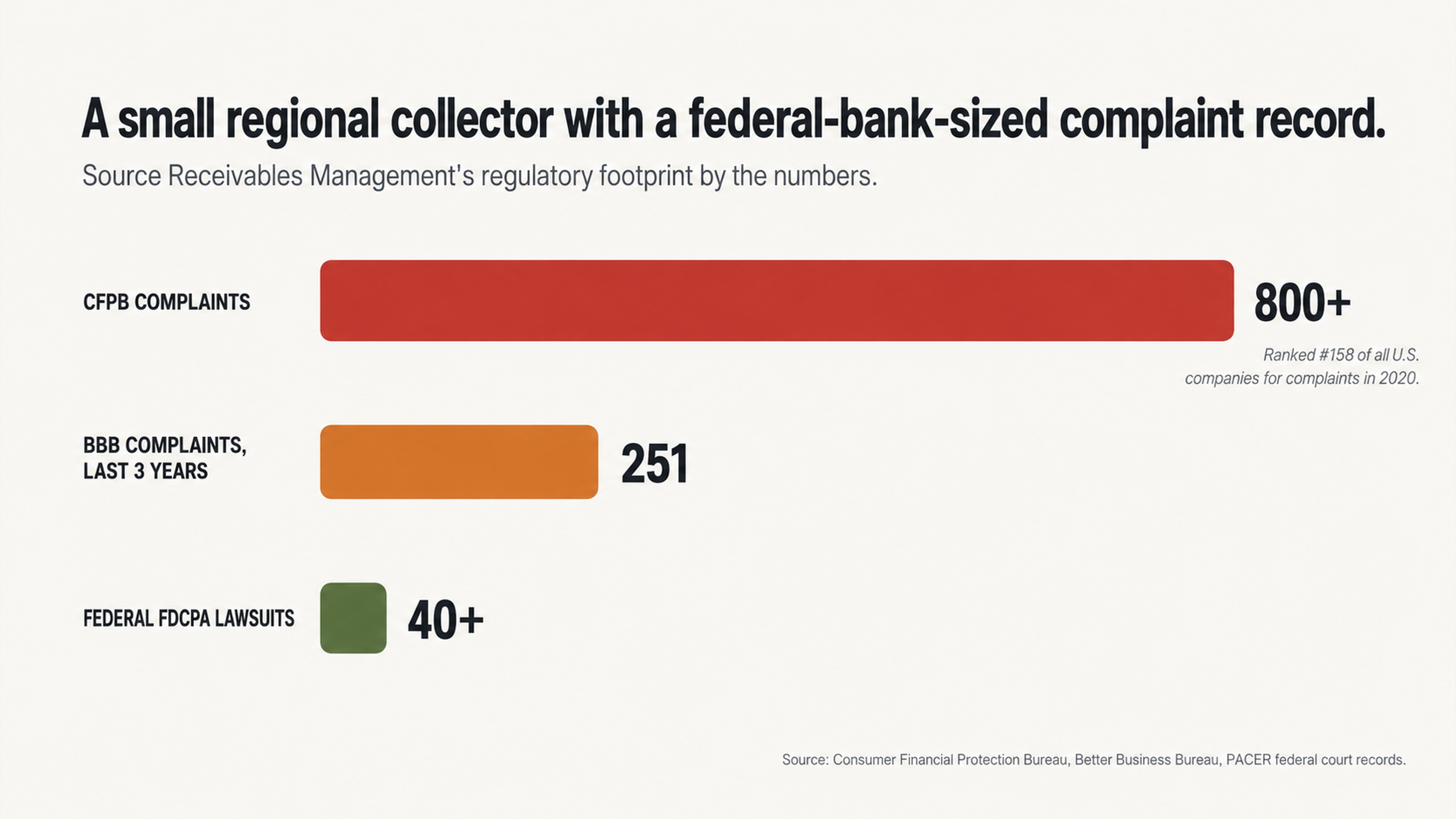

Source Receivables Management has a regulatory record that should raise some red flags for consumers. They have over 800 complaints registered with the Consumer Financial Protection Bureau, which is a high number for a relatively small, regional collection agency. In 2020 alone, SRM ranked #158 out of all companies (not just collection agencies), nationwide for the number of complaints filed against them. In other words, this small collection agency out of North Carolina ranked alongside some of the largest financial institutions in the country in the number of complaints they received in a single year.

The Better Business Bureau has given Source Receivables Management an F rating, which is the worst rating possible. According to the BBB’s records, there have been 251 complaints filed against the company in the last 3 years alone. They state, “This business has an F rating due to the company’s failure to respond to complaints and the pattern of complaints.”

According to the Public Access to Court Electronic Records (PACER) database, there have been over 40 federal lawsuits filed against Source Receivables Management for violating the Fair Debt Collection Practices Act (FDCPA).

Why paying first is usually the worst move.

The Payment Paradox

When you have a collection account on your credit report, the first thing you want to do is pay it off and be done with it. Unfortunately, this can be one of the worst things you can do. When you pay a collection account, the status is updated to "paid collection." However, it can stay on your report for up to 7 years from the original delinquency date. And in many cases, your credit score will barely improve at all, because the negative information is still on your report.

What the collection industry doesn’t want you to know is that when you pay a collection account, you are validating that the debt is legitimate, and belongs to you. And once you do that, many of your rights are gone.

One of the main reasons collection agencies want you to pay right now is because it allows them to close the account. When you pay, they don’t have to do anything else, and the account is closed. This is important to them because the collection industry is built around volume. Margins are thin, and agencies have to collect as much as they can as fast as they can in order to make a profit.

When you force them to verify the debt, and jump through hoops, it takes time and costs them money. It isn’t worth their while, so they want you to pay now and be done with it.

The Error Rate Reality

According to a study done by U.S. Public Interest Research Groups, 79% of credit reports contain either mistakes or serious errors. Let me say that again. Almost 8 out of 10 credit reports have incorrect information on them. This isn’t just some minor statistic. This is reality of the credit reporting system. It is so infested with errors and problems that the mere fact that an account is being reported is absolutely no indication that it is legitimate. And collection accounts are among the most likely to contain errors.

This is because most debts have been sold and resold so many times that the documentation is almost always incomplete. When the original creditor decides to charge off your account and sell it to a collection agency, they typically only provide the most basic documentation. And then when it gets sold and resold down the line, that documentation only gets worse and worse. By the time a debt finally ends up at a third-party collection agency like Source Receivables Management, there is a good chance that much of the documentation is already gone.

The CFPB complaints filed against SRM are full of consumers saying things like:

“I requested validation of the debt from the consumer. They would not send me the proper documentation.”

“They did not validate the debt at all.”

“This item is inaccurate because I never received a contract for the account from the consumer.”

In fact, failure to validate debts when requested by consumers, and inaccurate credit reporting are among the most common problems that consumers report about SRM.

The Strategic Approach to Source Receivables Management

Understanding Your Leverage

If you are unfamiliar with the credit reporting system, and your rights under federal law, you are at a tremendous disadvantage when dealing with a collection agency. That is exactly what they are counting on. See, the collection industry is all about leverage. And they know that when it comes to your credit report, all the leverage is on your side. You have numerous rights under federal law, including the right to dispute any item on your report that you don’t feel is 100% accurate. You have the right to request validation of any debt that a collection agency is trying to collect from you. And you have the right to have any information that cannot be verified reported to the credit bureaus removed.

The problem is that most consumers don’t know any of this. And so when a collection agency comes at them aggressively, making threats and demands, they don’t know how to react. In some cases, they pay the account right away, just to make the problem go away. In others, they may dispute the account online at the credit bureau website, but when the collection agency verifies it, they don’t know what to do.

But the fact is that the law is on your side, and there are ways to deal with Source Receivables Management strategically, in a way that protects your interests, and your credit score. According to federal law, you have the right to request validation of a debt within 30 days of initial contact from a collection agency. When you do this, they are required to obtain verification of the debt from the original creditor, including the amount of the debt, the name of the original creditor, and proof that they have the legal right to collect the debt.

The fact is that in many cases, collection agencies can’t do this. The documentation doesn’t exist, or they can no longer access it. And in many cases, they are trying to collect debts that aren’t even legally enforceable. The class action lawsuit Rawson v. Source Receivables Management established important precedent.

Essentially, the judge ruled that, “Plaintiff alleges Defendant violated the FDCPA by sending her collection letters which would lead the least sophisticated debtor to believe a debt was legally enforceable when, in fact, it was time-barred.” In other words, they were trying to collect debts that they knew they couldn’t legally enforce. And there is nothing unique about SRM in this regard. This is a common tactic across the collection industry.

Why Silence is Golden

When you are talking to a debt collector on the phone, the worst thing you can do is admit that you know them, recognize the debt, or acknowledge your address. Essentially, anything you say can and will be used against you. They will ask you to confirm your Social Security number, date of birth and address. And they will ask you to discuss payment options. All of this information can be used against you later if you decide to dispute the debt or negotiate settlement.

On the other hand, if you put everything in writing, you have a paper trail of your communications, and you don’t have to worry about saying something you didn’t mean to. Plus, debt collectors hate written communication. It takes time and effort to draft a letter, mail it and then follow up. They want to get you on the phone where they can pressure you into doing what they want. If you refuse to talk to them on the phone, and only communicate in writing, you maintain control of the situation.

Here is what some consumers are saying about their experience with SRM:

“I explained to her that I was going to file a complaint with the Consumer Financial Protection Bureau, she told me to go ahead and do it.”

“When I told her I was explaining and she needed to quit interrupting me, she became rude.”

“I asked to speak with a supervisor and she said I could but they were all busy.”

What’s required to remove a collection account.

The Verification Process

If there is a collection account on your credit report, and it is inaccurate, erroneous, or fraudulent, you have the right to dispute it with the credit reporting agency, and have it removed. You also have the right to request validation of the debt from the collection agency. If they cannot provide it within 30 days, the account must be removed from your report. This isn’t some loophole or secret. This is your right under federal law.

When you dispute a collection account with the credit bureaus, they contact the collection agency to verify the information. They are required to respond within 30 days, and provide verification of the debt. This typically includes:

The name of the original creditor

The amount of the debt

The fact that the consumer is responsible for the debt

If the collection agency can’t provide this information, or doesn’t respond at all, the credit bureaus must remove the account from your report. In some cases, collection agencies will re-report deleted accounts to the credit bureaus, hoping that no one will notice. But this is a violation of federal law, and can subject them to penalties.

The CFPB complaints against SRM include numerous consumers who say that the company is re-reporting accounts to the credit bureaus that they have already deleted:

“Defendant Source Receivables Management is attempting to collect a debt from me that has already been deleted.”

“I had this collection removed through another credit repair agency in 2015 and the account is now being pursued by Source Receivables Management.”

In addition, many consumers complained about SRM’s failure to validate debts when requested:

“This business will not return calls to validate debt.”

“I wrote the consumer and requested validation of the alleged debt. To date I have not received any response.”

Documentation Failures Create Opportunities

Debt collection is a volume business. Agencies buy accounts for pennies on the dollar and try to collect as much as they can. In most cases, the original creditor only provides limited documentation when selling off the debt. And each subsequent buyer sells it again with even less documentation. By the time a debt gets to a third-party collection agency like SRM, much of the documentation may already be gone.

The complaint from the Al v. Source Receivables Management class action lawsuit is illustrative. Essentially, the lawsuit alleged that SRM was sending collection notices to consumers with a notation on the front of the letter saying, “Please see the reverse side for our Company’s policies and your privacy rights.” The problem was that the reverse side of the letter was blank.

Now, we know that everyone makes mistakes. But if a collection agency can’t even be bothered to print information on the back of a collection notice, what are the chances that they have kept all the documentation for the underlying account? And in some cases, the collection agency may actually admit that they don’t have all the documentation. When they offer to “settle” the account for less money than they are claiming you owe, that is a tacit admission that they don’t have all the documentation. Because if they did, why would they be willing to accept less?

The fact is, negotiations are an admission that the debt amount is not fixed. And if that is the case, how do we know that any of the information is accurate?

The difference professional intervention can make.

Why Consumers Usually Lose

When consumers try to deal with a collection account on their own, they are almost always at a disadvantage. Collection agencies do this for a living, and they have all the knowledge and expertise. They know exactly how the system works. They know how to respond to consumer disputes, and how to negotiate settlements. Most importantly, they know how to get consumers to do what they want them to do.

Consumers on the other hand, usually have no idea what they are doing. In many cases, they end up filing a simple dispute with the credit bureau, saying they don’t recognize the account or think it is an error. But in most cases, the collection agency can easily verify the account, or at least say that they have. And at that point, the consumer doesn’t know what to do.

In other cases, the consumer may call the collection agency and try to negotiate a settlement. But they don’t know what they are doing, and may end up admitting things they didn’t intend to, or promising to pay when they shouldn’t.

The credit damage from a collection account is the main issue for most consumers. This isn’t a moral issue about whether or not you owe someone money. And it usually isn’t even a legal issue about whether the collector can sue you and make you pay. It is a practical issue about the fact that the account is on your report, lowering your credit score, and preventing you from getting approved for a house, a car or a job.

Professional intervention, on the other hand, approaches the problem from the perspective of credit damage, and how to remove it. This means understanding the legal technicalities that are required for debt validation. It means knowing which documentation requests are most likely to get a response, and which procedures are mostly likely to result in deletion of the account. And it means having a plan in place in case the collection agency decides not to play ball.

The Value of Expertise

Collection agencies have in-house counsel, compliance officers and procedures in place for dealing with consumer disputes all day every day. Consumers have none of that. And when they try to deal with a collection agency on their own, they are almost always at a disadvantage.

We have already discussed how SRM has been the subject of over 40 federal lawsuits for FDCPA violations. That type of history makes it worth hiring an expert to deal with them. At the very least, they will be able to tell you whether the same factors are at play in your situation, and you may have the same grounds for a lawsuit.

In addition, professional credit repair experts provide accountability. They keep a record of all correspondence with the collector, and make sure that everything is done properly. If the collector violates federal law at any point in the process, you will have someone to help you enforce your rights. And if you need to file a lawsuit, you will have an expert witness who understands the process and your situation.

Conclusion

If Source Receivables Management is on your credit report, you still have options. Their 800+ complaints with the CFPB, their F rating with the BBB, and their history of being sued for FDCPA violations are all indicators that you should proceed with caution.

What they don’t want you to know is that the system is rigged in your favor. There are rules and procedures that have to be followed. And there are rights you have as a consumer that the collection agencies don’t want you to know about.

The credit reporting system is fraught with errors. Almost 80% of reports have at least one error, and many have several. Proceeding to pay a collection account without first verifying the information at the credit bureau is like assuming you are guilty until proven innocent. The stakes are too high and the error rate is too great. You have the right to verify the information, and proceed accordingly.

Don’t let them push you around and tell you what to do.

Take Action Now

If Source Receivables Management is on your credit report, you need to act now. You are losing money and opportunities every month that the account is on your report and damaging your credit.

At FightCollections.com, we specialize in verifying collection accounts at the credit bureaus. We understand what documentation is required for a collector to prove a debt, and we understand your rights under federal law. We have helped consumers remove inaccurate, erroneous, and unverifiable collection accounts from credit reports.

Call us now for your free consultation, and find out how we can help you. There is no obligation, and no up-front fee. So why wait? Call us now.