Are you reeling from the news that you have a Spire Recovery Solutions debt collection agency account on your credit report? Don’t panic — we have good news for you.

The federal government’s consumer protection laws outline specific items you can request from Spire Recovery Solutions, and ways you can dispute the debt to get it removed from your credit report.

In this guide, we will walk you through what you need to know about Spire Recovery Solutions so you can exercise your legal rights as a consumer to dispute their claims.

Who is Spire Recovery Solutions?

Spire Recovery Solutions is a debt collection agency based in Lockport, NY. According to the BBB profile for the company, here is their contact information:

The company is owned by veterans and was founded by Joseph Torriere and Jacob Torriere. They also have an office in Richardson, Texas and employ about 35 people. Their estimated annual revenue is about $6 million.

What has Spire Recovery Solutions done?

We ran an investigative search on Spire Recovery Solutions and uncovered the following track record of behavior that you should know before deciding how to handle the debt:

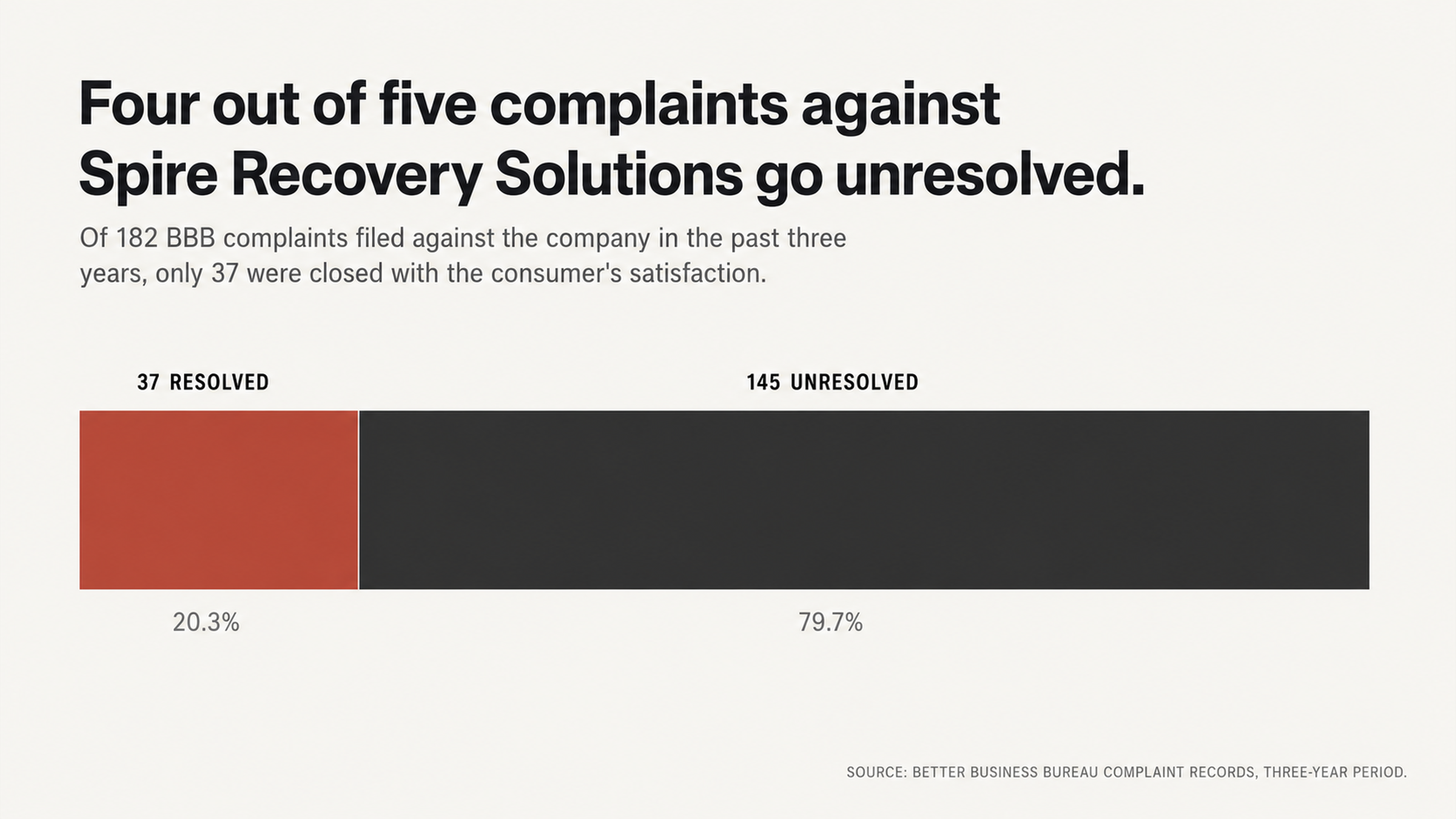

The Better Business Bureau reported that Spire Recovery Solutions has had 182 complaints filed against it in the past three years, including 46 in the past year. The company has a 1.42 star rating out of 5 on BBB.

Of 182 complaints filed with the BBB against the company, only 37 were reported as closed with the consumer’s complaint resolved. That means nearly 80% of consumers who complained about the company did not feel that their issue was adequately resolved.

Spire Recovery Solutions is a BBB accredited company with a B+ rating (though they claim an A+ rating on their website).

According to federal court records, there have been at least 10 lawsuits filed against Spire Recovery Solutions for FDCPA and TCPA infractions. In 2024 alone, four FDCPA lawsuits have been filed against the company. All of the lawsuits against Spire Recovery Solutions appear to have been settled out of court — and quickly, within a few months.

What are my rights when a debt collector like Spire Recovery Solutions contacts me?

Federal laws like the FDCPA and FCRA provide clear guidance on your rights as a consumer when dealing with debt collectors. Here are the top things to know about these laws and how you can use them to your advantage:

Under the FDCPA, you can request written proof of a debt from a collector within 30 days of initial contact. The collector cannot continue to pursue the debt until it provides that proof.

Debt collection agencies cannot engage in abusive, unfair or deceptive practices. That means they can’t threaten to sue you if they don’t intend to follow through. They can’t misrepresent how much you owe. They can’t call you at inconvenient hours or places.

You can file a claim under the FDCPA for statutory damages up to $1,000, plus actual damages and attorney fees, if the debt collector violates any part of this law.

In a November 2024 review on the BBB website, one consumer accused Spire Recovery Solutions of engaging in this type of third-party contact: “This company contacted my children in an attempt to contact me,” the consumer reported. “They called every family member on my contact list, including my children.”

Another consumer review on the site from October 30, 2024 accused a representative of the company of misrepresenting himself: “I just received a call from a family member stating that Spire Recovery Solutions called them from the FBI,” the consumer wrote. “How can a company operate like this?”

Claims of this nature raise clear FDCPA red flags that warrant your attention.

Under the FCRA, everything on your credit report must be accurate, complete and verifiable. If you dispute an item on your report, the credit reporting agency must investigate and remove the item if it cannot be verified within 30 days.

This is where many debt collection accounts falter. A U.S. PIRG study found that 79% of credit reports contain some mistake or serious error. Every time a debt changes hands — from the original creditor to a debt buyer to a debt collector — the potential for errors and missing documentation grows.

That’s why the credit report dispute process is so effective. The debt collector has to provide documentation showing not only that you owe the debt and the amount is correct, but also that they have the authority to collect it. Many can’t. That’s especially true for very old debts, or those that have been sold and resold over time.

Why should I dispute before I pay?

When you get a collection notice from a debt collector, your first instinct might be to pay it — even if you don’t think you owe it — just to make the headache go away. But before you pull out your wallet or sign onto your computer to make an online payment, understand what will happen if you pay the debt.

Paying a collection account changes the status of the item on your credit report from unpaid to paid. However, the item itself will remain on your report for seven years from the date of the original delinquency — not from the date you paid it.

If you pay a very old debt, you may inadvertently restart the clock on the statute of limitations in your state, which could leave you vulnerable to a lawsuit for a debt that was previously time-barred.

When you pay a debt, you are also acknowledging that you owe it — which means you’ve waived your right to dispute it later.

Your first move with any collection account should always be to investigate and dispute — never to pay.

Why might I win if I dispute?

Debt collection agencies often don’t have all the documentation they need to prove a debt is valid. When debts are sold and resold, paperwork can get lost or misplaced. That might mean the collector doesn’t have account statements, a copy of your signed contract or your payment history.

Because the burden of proof is on the collector and not the consumer under the FDCPA, that’s a problem for them — not for you.

In a review of Spire Recovery Solutions filed with ComplaintsBoard, one consumer said they asked the company to verify their debt: “They stated they couldn’t provide me with any documentation unless I made a payment arrangement first,” the consumer reported. “I hung up as I knew they couldn’t provide documentation.”

Once a debt has been sold, the original creditor has already written it off — they don’t care about collecting it anymore, and aren’t likely to lift a finger to help the debt collector document the item. So if you think you’re doing the right thing and paying a collection account because you want to make things right with the original creditor, think again. The debt buyer owns your account now, and any money you pay on it goes straight into their pocket.

Warning Signs of a Problem Collection Account

If you are dealing with a collection agency and are concerned about their practices, there are certain red flags to watch for. If the agency is asking you to pay immediately without sending a written validation of the debt, this is a major warning sign. Threatening you with arrest, wage garnishment, or a lawsuit (if they have not filed a lawsuit) is against federal law. If they refuse to validate the debt, it could be because they don’t have the documentation to do so.

If the debt collector is using abusive or threatening language, this is never acceptable under the FDCPA, no matter how much money you owe. Calling you before 8 am or after 9 pm is against federal law. Continuing to contact you after you have sent a cease-and-desist letter is a violation of your rights. Contacting your employer about your debt (other than to verify your employment to find you) is also against the law.

Many of the reviews from Spire Recovery Solutions customers include allegations of these types of behaviors. Calling family members, even children, is mentioned in several reviews. Some reviewers state that the representative refused to send them the validation. While these behaviors are documented on various review sites, it is always a good idea to take them with a grain of salt.

What is a legitimate debt collector?

A debt collector will send you a written validation of the debt within 5 days of contacting you. They will state that they are a debt collector every time they speak with you. They will not contact you if you have disputed a debt (until your dispute has been resolved). They will send you documentation showing that the debt belongs to you and that the correct amount is being collected.

If the collection agency does not meet these standards, they may be operating illegally or attempting to collect a debt that they cannot validate. Just because they do not have the proper documentation does not mean you didn’t owe money to anyone, it simply means that this particular debt collector cannot prove that the debt belongs to you, which is what matters.

How to Dispute a Credit Report

If you are disputing a collection account that is on your credit report, you need to understand the process. When you dispute an item on your report, this opens an investigation that must be conducted according to federal law. The credit bureau has 5 days to notify the entity who furnished the information (in this case, Spire Recovery Solutions). Then, the furnisher has 30 days to investigate your dispute and respond to it. If they are not able to validate the information, the credit bureau must delete it from your report.

When you are disputing an item on your report, your dispute should clearly state what you believe is wrong with the information. This could include the fact that the balance is incorrect, the date is wrong, this is not your account (possibly identity theft or confusion with another individual), this account is past the statute of limitations or this account has been paid. If your dispute is general, you will likely get a general response. If you have specific concerns, they will need to provide specific documentation to prove their point.

You can have items removed from your report if they are inaccurate, erroneous, fraudulent or if the furnisher is not able to verify them within the allowed amount of time. The key here is to remember that, when you dispute something, the burden is on the debt collector to show that the information is accurate. You don’t have to prove that the information is inaccurate, they must prove that it is accurate.

Why You May Need Help with a Debt Collector

When dealing with a debt collector, the playing field is not level. The debt collector deals with thousands of consumers and knows exactly how to navigate the system. They know what type of response the credit bureau is looking for and what type of documentation the regulators will not challenge. As a consumer, you may only go through this process when dealing with your own credit report.

Working with a credit repair professional can help level the playing field. We understand exactly what type of language will trigger a valid investigation (and what type of language will get a canned response). We know how to escalate a dispute if we don’t get a satisfactory response. We can help identify any violations of the FDCPA which can aid in having the account deleted.

The fact that Spire Recovery Solutions has been the target of at least 10 federal lawsuits regarding their collection practices may indicate that this particular collection agency has some systemic problems that a credit repair professional can recognize and use to your advantage.

When they quickly settle lawsuits (such as the Miller v. Spire Recovery Solutions which was settled approximately 2 months after the suit was filed) it may indicate that they would rather settle than have their practices challenged in court.

What to do After a Successful Dispute

If you are successful in disputing a collection account and having it removed from your report, don’t think that this means you no longer have to pay attention to your credit report. In fact, this should be the very beginning of your ongoing credit monitoring. You are entitled to a free copy of your credit report from each of the 3 major credit reporting agencies every year. You can access these reports on the website AnnualCreditReport.com. Make sure to review them carefully to ensure there are no inaccuracies or accounts showing up that you don’t recognize.

If Spire Recovery Solutions (or any other collection agency) attempts to re-report a deleted collection, this is a violation of both your FCRA and FDCPA rights (unless they have new information to validate the debt). Make sure to document this carefully, as it may be grounds for a lawsuit.

Improving Your Credit Report Going Forward

While addressing any collection accounts on your credit report is a priority, once you have handled those, you can focus on improving your credit score going forward. Your payment history on your current accounts is the most important thing, so making sure you are paying your bills on time is crucial. Keeping your credit utilization ratio on your revolving accounts below 30 is also a good idea.

Opening accounts that will report positive information to the credit bureaus and monitoring your report on a regular basis are both important parts of improving your long-term credit health. The knowledge you gain about your FDCPA and FCRA rights will serve you well if you have future issues with debt collectors or problems on your credit report.

In Conclusion

Spire Recovery Solutions has a history of consumer complaints, federal lawsuits and a low consumer satisfaction rating. With 182 complaints registered with the BBB, a 1.42-star consumer review rating and at least 10 federal lawsuits alleging violations of the FDCPA, this debt collector has obviously caused significant problems for consumers.

You have rights that the law will enforce for you. The FDCPA and the FCRA are not just legal technicalities, they are laws that give you the power to insist that a debt collector proves any debt they are attempting to collect. Approaching the situation with a dispute-first strategy simply means that you are making the debt collector prove that they have the documentation for the debt (which they may not).

Paying a collection account prior to investigating whether or not it is accurate and/or disputable is often the worst thing you can do. It gives the debt collector all the power, does not help your credit score the way deleting the account would and may validate a debt that is not yours. Educating yourself about your rights changes a frightening letter into an opportunity to take charge.

What to Do Now

If you have a Spire Recovery Solutions collection account on your credit report, you don’t have to face it alone. At FightCollections.com, we specialize in working with consumers to help them fight debt collectors and delete questionable collection accounts from their credit reports. We know the games that debt collectors play and the loopholes in the law that can help us get accounts deleted.

Every month that a collection account is on your credit report can cost you money in higher interest rates, higher insurance rates and missed opportunities. Don’t wait any longer, contact us at FightCollections.com today for a free consultation to talk about your situation and find out how we can help you enforce your legal rights when dealing with Spire Recovery Solutions and improve your credit.