Have you noticed that the way to remove State Collection Service from your credit report is not through their phone number or payment portal? It’s actually by forcing them to prove their claims about you while you protect your legal rights every step of the way.

In this article, we will walk you through how this works, using the information we have gathered about this medical debt collection agency. At the end of this article, we will show you how to get professional help to remove this account and restore your credit score. Not to worry though - we will cover everything you need to know before then.

If you found this article after finding State Collection Service on your credit report, you might feel like you just discovered a landmine in your financial path. This Wisconsin-based medical debt collection agency has been around for over 70 years, providing revenue cycle services to hospitals and healthcare systems all over the country.

Despite industry recognition (including a Best in KLAS award for 2024) and an A+ rating from the Better Business Bureau, this company has terrible customer reviews. This disparity between the awards and reviews is a dynamic you see often in the debt collection industry. Collectors know the rules of the game. Consumers do not. If you know who you’re dealing with, you’re one step ahead.

Who is State Collection Service?

State Collection Service, Inc. is a third-generation family-owned debt collection agency headquartered in Madison, Wisconsin. The company specializes in healthcare debt. In fact, about 85 percent of their business comes from hospitals, medical groups, and health systems.

State Collection Service is a Compassionate Medical Debt Collector (According to Them)

State Collection Service describes itself as a compassionate healthcare revenue cycle partner. They are HITRUST certified and just earned a 2024 Best in KLAS award for debt collection services. In 2008, the company merged with Protocol Financial Service of Minnesota. They have branch locations in Beloit, West Allis, and Geneva, Illinois. The company chairman and CEO is Thomas Haag. The president is Terry Armstrong.

Despite the picture they paint, we found that State Collection Service has been sued in multiple federal class-action lawsuits alleging deceptive collection practices. While they have an A+ rating from the Better Business Bureau, their customer reviews average just 1 out of 5 stars. This suggests that while State Collection Service does a great job of checking procedural boxes, they have a lot to learn about treating their customers right.

State Collection Service Earns an A+ Rating from the BBB (But Their Customer Reviews Tell a Different Story)

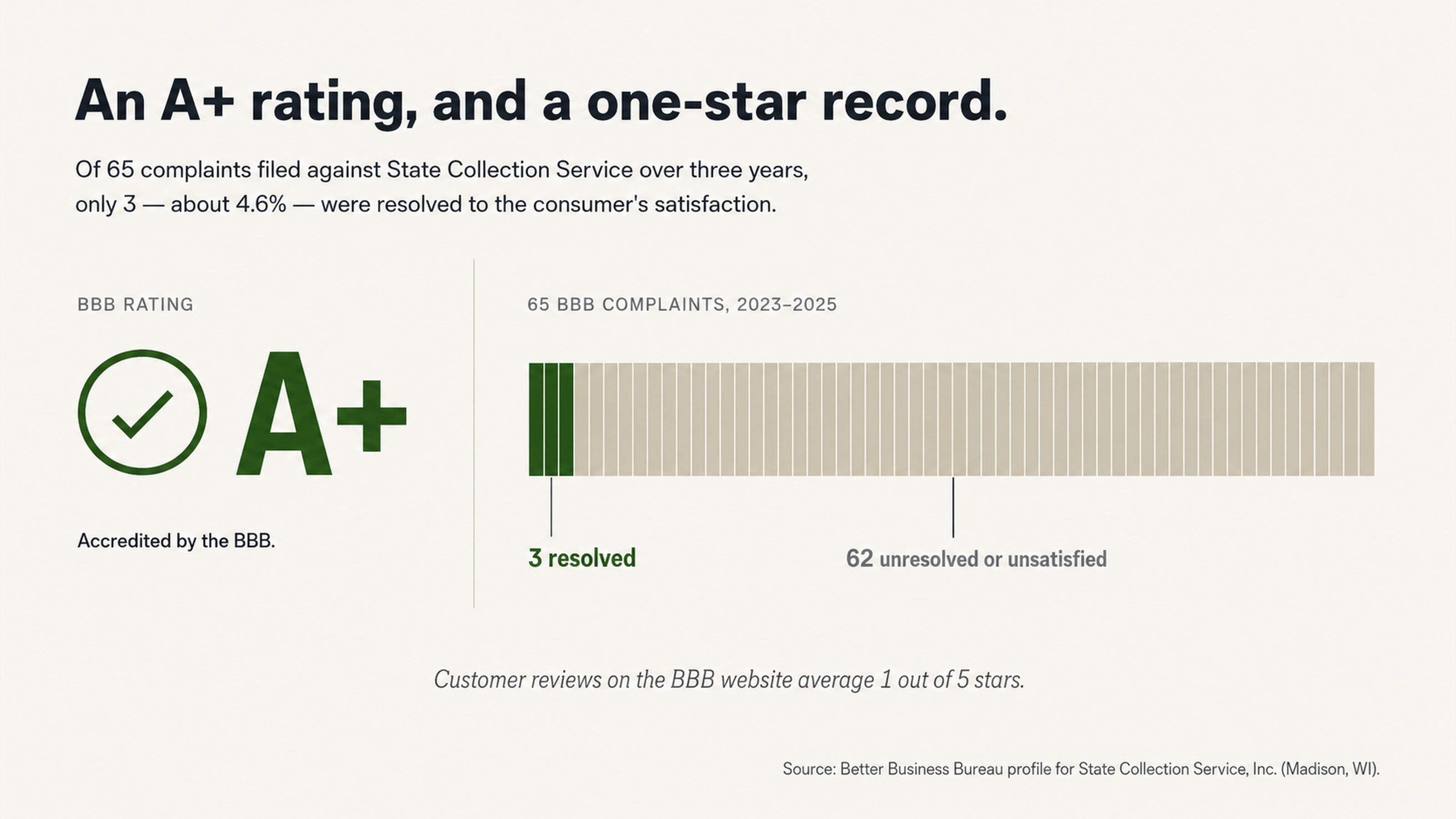

We were shocked at what we found when we researched State Collection Service’s rating and reviews on the Better Business Bureau (BBB) website. On one hand, they have an A+ rating and are accredited by the BBB. On the other hand, every single customer review on their profile is 1 star. On WalletHub, 75 percent of the 24 reviews are 1 star.

Over the last 3 years, the BBB has received 65 complaints about State Collection Service. Of those, 24 are complaints about problems with their order or account, 20 are billing disputes, 11 are about service issues, and 5 are customer service complaints. Of those complaints, 62 of them received a response from the company, but only 3 of them were resolved to the satisfaction of the consumer. If you do the math, you find that only 4.6 percent of the complaints they received over the last 3 years were resolved satisfactorily. This tells you that the customer service at State Collection Service leaves a lot to be desired.

But what are consumers saying about State Collection Service? We found that many of the complaints allege that the company is harassing them, that they never verified the debt, or that the debt they’re trying to collect is having a big impact on their credit score.

In February 2023, one reviewer wrote on the BBB website, "continues to contact me, performing several hang up calls, harassing texts, and spam like email. Has never provided any clear indication of why I am even receiving these calls! Just that I owe them money somehow. Definitely seems very scammy!"

One reviewer on WalletHub said that she lost 120 points off her credit score because of what she called "false info." She said that she was 100 percent covered by Medicaid and had not received any bill prior to the collection showing up on her report.

Several Federal Lawsuits Allege that State Collection Service Engages in Deceptive Practices

We also found that State Collection Service has been a defendant in at least 11 federal lawsuits over the last decade. Several of those suits are class actions alleging that the company engages in deceptive practices. For example, in the lawsuit Williams et al v. State Collection Service (Case No. 2:17-cv-00532-PP in the Eastern District of Wisconsin), the plaintiffs allege that the collection letters the company sent failed to clearly state the amount of the debt. They claim the letters contained language indicating that there were multiple accounts in several different departments.

In another class-action suit filed in 2018 called Cajigas (Case No. 2:18-cv-01864), the plaintiff alleges that State Collection Service made false threats about reporting debts to the credit reporting bureaus. Specifically, the lawsuit claims that the company threatened to report medical debts to credit bureaus within 30 days even though the law prohibited them from doing so for at least 180 days (a new policy regarding the credit reporting of medical debts took effect in September 2017).

In 2015, a court in the Northern District of Illinois found that State Collection Service had violated the Fair Debt Collection Practices Act (FDCPA). The court awarded the plaintiff $1,001 in statutory damages plus attorney fees. While State Collection Service has successfully defended several other suits, most of those dismissals were based on technicalities like standing rather than an actual vindication of the way they collect debts.

Why You Shouldn’t Pay State Collection Service

You know the feeling. You find a collection account on your credit report and you just want it to go away. So you pay it. We can’t blame you. That’s what collectors like State Collection Service count on. They want you to feel so anxious about the situation that you do whatever it takes to make it go away as fast as you can.

The thing is, paying the collection just means it goes from being an unpaid collection to a paid one. The account will still be on your credit report for up to 7 years. If you paid State Collection Service, the original creditor (probably a hospital or medical practice) has already written that debt off and moved on. Once they assign it to a collection agency, they no longer have any financial interest in whether or not you pay it. So don’t feel like you owe a moral obligation to pay a debt just because a collector says you do. Most of the time, that isn’t true.

Instead of calling State Collection Service to pay, you should just not talk to them at all. Every time you talk to a debt collector, you’re giving them an opportunity to convince you to pay a debt you may or may not owe. Every time you talk to them, you’re giving them more information about you that they can use to collect from you. Every time you talk to them, you’re giving them the chance to talk you into a payment plan you can’t afford. Instead of engaging with them, write them a letter. If you do decide to pay State Collection Service, make sure you get it in writing first.

Unfortunately, we found several reviews from consumers who paid their debts only to have State Collection Service continue to pursue them for payment. One reviewer on the BBB website said that State Collection Service contacted her for over a year attempting to collect a medical bill she didn’t owe. She said she actually worked at the hospital where they were attempting to collect from her and was on a payment plan that showed she had paid the bill in full.

Paying State Collection Service will not get it off your credit report any faster than disputing it will. So why not dispute it and see what happens? Here is how to do it.

How to Remove State Collection Service from Your Credit Report

Understanding the rules regarding credit reports is the first step to removing an inaccurate collection account. But you have to actually read your report to understand what is going on. Under federal law, you are allowed one free credit report from each of the 3 major credit reporting bureaus (Experian, Transunion, and Equifax) every 12 months. You can access those reports at AnnualCreditReport.com.

Unfortunately, we found that 79 percent of credit reports contain errors or serious inaccuracies, according to U.S. Public Interest Research Groups. That is because the credit reporting system favors speed over accuracy. It also favors debt collectors who don’t verify the information they are reporting before they report it.

We found several reviews from consumers who say that State Collection Service is attempting to collect debts from them that they do not owe or did not verify. One reviewer on WalletHub said that State Collection Service posted an outstanding debt on their credit report when they had proof of payment. He called it "fraud."

Another reviewer said that State Collection Service sent him notices attempting to collect a debt from a clinic in a state where he no longer lives. He said he had not lived there for over 2 years.

If you initiate a dispute about something on your credit report, the credit reporting bureau must investigate and respond within 30 days. If you know how to initiate a dispute the right way, this can be a powerful tool for removing inaccurate information from your credit report.

However, the Fair Credit Reporting Act (FCRA) and the Fair Debt Collection Practices Act (FDCPA) are complicated laws with nuances that are difficult for the average consumer to understand. If you do not understand the laws the right way, you may not know how to dispute the account properly or how to force the bureaus to take action within the right amount of time. If they do not respond correctly, you may not know how to escalate your dispute to get the resolution you need.

When State Collection Service Can’t Verify the Debt

We found that when consumers dispute debts with State Collection Service, the company responds to their disputes by verifying that they have the debt with the original creditor but are unable to provide copies of the original contract and other documentation the consumers request. While this may meet the minimum requirements of the law, it may leave consumers without the documentation they need to verify whether the debt is valid.

You can dispute information on your credit report if it is inaccurate or false. You can also dispute it if it is fraudulent or if it cannot be verified within a reasonable amount of time. As we said above, we found that State Collection Service has been sued in several federal lawsuits alleging that the company engages in deceptive practices like failing to clearly communicate the amount of the debt a consumer owes.

We also found documentation suggesting that it is not unusual for State Collection Service to fail to verify a consumer’s debt before attempting to collect it. If you initiate a dispute the right way, citing federal law and including all the right documentation, you may be able to have your collection account removed. It is not a guarantee, but it is worth a shot.

The Truth About Medical Debt Collection

So what do you do if State Collection Service is attempting to collect an inaccurate debt? Unfortunately, medical debt can be incredibly complicated to collect. This is because the billing systems are complex, involving insurance companies, patients, and providers. There are a lot of places where errors can happen. So it is not surprising that we found so many consumers who claim that State Collection Service attempted to collect debts from them that were not valid.

Do not attempt to handle a debt collection situation like this on your own. You need professional help to understand how the laws protect you and to help you navigate the dispute process. With that kind of help, you can remove inaccurate collection accounts from your credit report and start repairing your credit.

Summary

After reading this article, do you still have questions about how to remove State Collection Service from your credit report? Let’s summarize what we learned.

State Collection Service is a third-generation family-owned debt collection agency based in Madison, WI. They specialize in medical debt and primarily serve hospitals and healthcare systems. Despite their industry awards and A+ rating from the BBB, consumers give them an average of 1 out of 5 stars on every review platform we could find. Several federal lawsuits allege that the company engages in deceptive practices like making false threats about credit reporting or failing to clearly communicate the amount of the debt.

Unfortunately, we found several consumer reviews alleging that the company harassed them or attempted to collect debts they did not owe or could not verify. When consumers dispute their debts, the company verifies with the original creditor but cannot provide them with copies of their original contract or other documentation.

The good news is that you have the power to remove inaccurate collection accounts from your credit report. But you cannot do it alone. You need to understand the federal laws that protect you and you need to understand how to initiate a dispute the right way to force the bureaus to take action within the right amount of time.

Get Help Now

Are you ready to talk about how you can remove State Collection Service from your credit report? Start with a free consultation with one of our credit experts.

At FightCollections.com, we help consumers dispute inaccurate information on their credit reports and hold debt collection agencies accountable when they fail to follow the law. If you have a collection account from State Collection Service on your credit report, we can help you understand your obligations, identify the most important things you need to dispute, and navigate the process to remove the inaccurate information.

Contact us today to start your journey toward repairing your credit report.