Although seeing a collection account on your credit report from Sunrise Credit Services might be stressful, it could also be the start of a credit repair journey that makes your credit stronger than ever.

The key to making this happen is to realize that you have more control over the situation than you might think.

Unfortunately, many people panic when they see a collection notice and immediately send money to the debt collector. Not only do they end up with unsatisfying results, but they often find that their credit scores don’t improve much, if at all.

By taking a step back and using the right strategy, you can set yourself up for a much better outcome.

In this article, we will provide a roadmap to help you take this collections account and turn it into an opportunity for credit repair. With the right knowledge and strategy, you can overcome this obstacle and come out with a better credit report and the knowledge of how to avoid it in the future.

Who is Sunrise Credit Services?

Sunrise Credit Services, Inc. is a debt collection agency that is based in Long Island, New York. The company has been in business since 1974 and collects many different types of debts, including medical bills, credit cards, telecommunications accounts, student loans, and magazine subscriptions.

They represent clients such as AT&T, Comcast, Bank of America, and numerous health care providers. They work as third-party debt collectors and also have an affiliate company that purchases debt.

What the Record Says about this Debt Collector

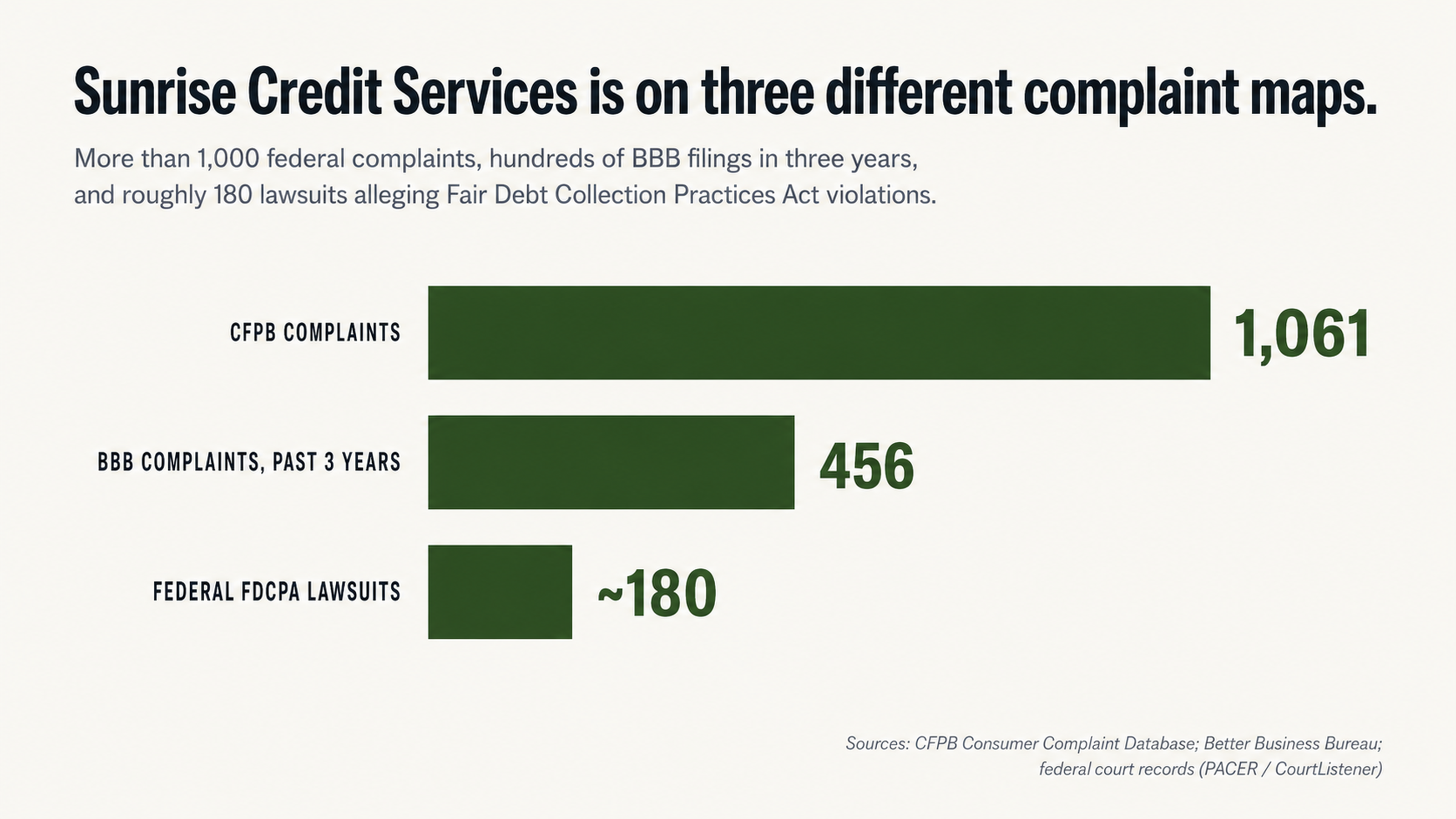

According to the Consumer Financial Protection Bureau database, there have been 1,061 complaints filed against this debt collector. Of those, 857 complaints were related to debt collection. This is a high number of complaints that have been filed with the federal government. In addition to these complaints, the Consumer Financial Protection Bureau lists a summary of the issues that consumers are complaining about.

We also checked online reviews from customers to see what they have to say about their experiences with this debt collector. On the Better Business Bureau website, this debt collector has an average customer review of 1 out of 5 stars. On Google, their reviews are only slightly better, averaging 1.6 out of 5 stars. On the Better Business Bureau website, they list 456 complaints that have been filed against this debt collector in the past 3 years. In the past year, 231 complaints have been filed against them.

In addition to complaints, we found that there have been approximately 180 federal lawsuits filed against this debt collector for alleged violations of the Fair Debt Collection Practices Act. There have also been several class action lawsuits filed against them, alleging everything from sending misleading collection notices to refusing to accept a consumer’s dispute of a debt. Lawsuits filed against a debt collector for violations of the FDCPA are a sign that they have a history of problems in their collection methods.

Why Your First Move Should Be to Dispute the Debt

If you see a collection account on your credit report, your first instinct is probably to pay the debt collector as quickly as possible. Most people believe that if they pay the collection account, it will be removed from their credit report and their credit score will improve. Unfortunately, this isn’t typically what happens.

Paying a collection account will update the status of the account from “unpaid” to “paid,” but it will still remain on your credit report. A paid collection account will still have a negative impact on your credit report, even though you’ve paid it. Many consumers have learned this the hard way, writing a check only to find that their credit report still shows a collection account.

The debt collection industry makes a lot of money off consumers who don’t understand how credit reporting works. Most debt collectors are very pushy about trying to get consumers to pay them as quickly as possible. Knowing your rights and taking the time to understand the situation will serve you much better than reacting out of pressure from a debt collector.

In addition to understanding how paying a collection account affects your credit report, you should also understand the credit reporting time limit for collection accounts. The credit reporting time limit for collection accounts is 7 years. This 7-year clock starts from the original delinquency date of the debt. Paying a collection account does not change the credit reporting time limit.

Some consumers have successfully negotiated with a debt collector to have a “pay for delete” agreement. With a pay for delete agreement, the debt collector agrees to remove the collection account from the consumer’s credit report in exchange for payment. Unfortunately, most of the time these agreements don’t work out in the consumer’s favor, and they are left with an empty checkbook and the same collection account still listed on their credit report.

Understanding the credit reporting time limit for collection accounts can help you make a strategy for how to deal with a collection account on your credit report. If paying a collection account doesn’t result in it being removed from your credit report, it’s worth considering whether or not you should pay it at all.

A Breakdown of the Entire Industry

Mistakes on Credit Reports Are Very Common

According to a study done by U.S. Public Interest Research Groups, 79% of credit reports contain errors or other mistakes. This means that it’s entirely possible that the collection account you’re looking at is not even supposed to be on your credit report at all. The credit reporting agencies consider a negative credit listing to be valid until someone proves otherwise.

On collection accounts, there are often mistakes related to the amount, account number, date, and even the consumer’s identifying information. Whenever a debt is sold, transferred, or assigned, the documentation can get lost or destroyed, leading to errors. Since most collection accounts have been sold multiple times, the paperwork and documentation are often missing.

If there is a mistake on a credit report, it’s up to the consumer to catch the error and dispute it. Unfortunately, this means that the consumer is often at a disadvantage when it comes to collection accounts. Debt collectors don’t have to verify that a debt is valid before listing it on someone’s credit report. However, consumers can use this same system to their advantage if they understand how to dispute a debt.

What Debt Collectors Can’t Always Verify

When a consumer disputes a debt, the debt collector must verify that the debt is valid and that it belongs to the consumer. Unfortunately, many debt collectors are unable to verify debts, especially if they are older or have been sold multiple times. In many cases, the original documentation no longer exists.

We found one Better Business Bureau complaint from a consumer who says that when they asked the debt collector to validate a debt, they were told that the company couldn’t provide the documentation because it didn’t exist. Despite this fact, the debt collector continued trying to collect the debt. We see many consumers complaining about this same issue when working with this debt collector.

In 2018, a federal lawsuit was filed against this debt collector. In the lawsuit, the consumer claimed that when they told the debt collector that they disputed the debt, the representatives told them that it would be futile to dispute because they owed the debt.

Under the FDCPA, debt collectors must accept a consumer’s dispute, regardless of whether or not they believe the debt is valid. In this case, the debt collector’s refusal to accept a dispute is the subject of a federal lawsuit.

The #1 Thing to Do First

Why You Should Always Dispute First

If there is a collection account on your credit report, the very first thing you should do is dispute it. You can dispute debts directly with the credit reporting agencies, and if the debt collector can’t verify that the information is valid, they must remove it from your report. Putting the burden of proof on the debt collector gives you the upper hand.

You can get a collection account removed from your credit report if the information is inaccurate, mistaken, fraudulent, or if the debt collector can’t verify it within a reasonable amount of time. Since so many credit reports contain errors and debt collectors often have a hard time verifying debts, this is a common outcome of disputing a debt. It never hurts to dispute a debt because it doesn’t cost anything to do so.

On the other hand, if you contact the debt collector directly, you could be doing more harm than good. Contacting a debt collector directly can restart the statute of limitations, help them verify your contact information, and give them an opportunity to pressure you into paying. For these reasons, it’s best to dispute a debt through the proper channels rather than contacting the debt collector directly.

How to Dispute a Debt the Right Way

If you’re going to dispute a debt, you can’t just claim that you don’t owe it. You need to identify the inaccuracy or mistake, request that the debt collector verify the debt, and follow up to make sure the credit reporting agencies and debt collector do what they’re supposed to do. There are deadlines and documentation requirements for each step of the way.

The FDCPA and FCRA give consumers many rights when they’re dealing with debt collectors. If a debt collector violates one of these federal laws, the consumer may be entitled to have the disputed item removed from their credit report. They may also be entitled to damages because of the violation of their rights. With 180 federal lawsuits filed against this debt collector, it’s clear that these laws can be effective when consumers know how to use them.

To understand the process well enough to dispute a debt successfully, consumers need to understand the terminology and procedures that will trigger the debt collector’s obligations. This is another way that the debt collection industry takes advantage of consumers. They are counting on consumers not understanding their rights and the process well enough to demand their rights. Once a consumer understands the process and their rights, the balance of power shifts in their favor.

Taking the Next Step

Moving Forward with Credit Repair

Getting a collection account removed from your credit report isn’t the end of your credit repair journey. In fact, it’s just the beginning. Now that you understand the importance of monitoring your credit report and how negative accounts can end up on your report incorrectly, you’ll be better equipped to avoid similar situations in the future.

Credit repair isn’t just about getting negative accounts removed from your credit report. You can also build a stronger credit report by using your credit accounts responsibly, keeping your utilization ratio low, and making sure your payments are on time. Rather than just erasing the past, you’re building a credit report that will serve you well into the future.

Many consumers find that once they’ve made it through the process of disputing a debt, they’re more financially fit than they were before the debt showed up on their credit report. They understand their credit report better, they understand their rights, and they know how to advocate for themselves. All of these skills will continue to serve them well long after the debt has been removed.

Why You Need Help from a Professional

While the dispute process is straightforward, there are a lot of nuances that can make or break a successful removal. If you’ve never disputed a debt before, it can be hard to understand all of the technical, legal, and strategic issues involved. A professional does this kind of work all the time and will understand how to navigate the process successfully.

If you work with a consumer advocacy firm that specializes in removing collection accounts from credit reports, they will understand the documentation and verification issues that are likely to arise. They’ll be able to help you identify those issues and write a dispute letter that will trigger the debt collector’s obligations under the law. If the debt collector doesn’t comply, they’ll understand how to escalate the situation.

In addition to understanding the process, professional advocates will also be very familiar with how this particular debt collector operates. They’ll understand their tactics and be able to anticipate how they will react in different situations.

Finally, working with a professional advocate will help level the playing field. Debt collectors do this for a living and have staff, attorneys, and systems in place to maximize the amount of money they collect. When you have professional advocates in your corner, you won’t be on your own against all of these resources.

The Bottom Line

Receiving a collection account from Sunrise Credit Services is not the end of the world. In fact, it could be a great opportunity to take the bull by the horns and improve your credit report. Now that you understand that paying a debt might not be the best option, you can formulate a strategy to dispute the debt and have it removed.

Based on the complaints and lawsuits that have been filed against this debt collector, it seems that many of the debts they’re trying to collect can’t be verified. Start with a dispute to see if this is the case with your debt.

The first step in writing a new chapter in your credit report is scheduling a free consultation to talk about your credit report and situation. Do you have a collection account on your credit report from Sunrise Credit Services? Let us help you.

At FightCollections.com, we specialize in working with debt collectors and using the dispute process to remove questionable collection accounts from credit reports. Let us help you write a better chapter in your credit report. Contact us today.