Were you checking your credit report in preparation for a mortgage application when you saw a TSI Collections account on it for $2,847, from a medical bill you do not remember incurring? The account is already 18 months old and you never received one notice about the account.

If so, you are among the millions of Americans who are shocked to see a collection account from TSI Collections on their credit report.

According to a U.S. PIRG report, 79% of credit reports have errors or serious errors. Many of these errors include collection accounts that the consumer was unaware of, that the consumer had already paid, or that had balances that did not match any legitimate debt balance.

Your initial thought may be to call the agency and straighten the situation out. Before you do, there is one thing you need to know. In almost every instance, this is a mistake. What you need to know about TSI Collections and how to deal with this collection account, we will cover in this article.

Transworld Systems Inc. (TSI Collections) is one of the largest debt collection agencies in the country. TSI has approximately 56 offices throughout the U.S. with operations centers throughout the U.S., Canada, Latin America, India, and the Philippines. TSI collects a broad array of debts including medical, student loans, utilities, and other consumer debts.

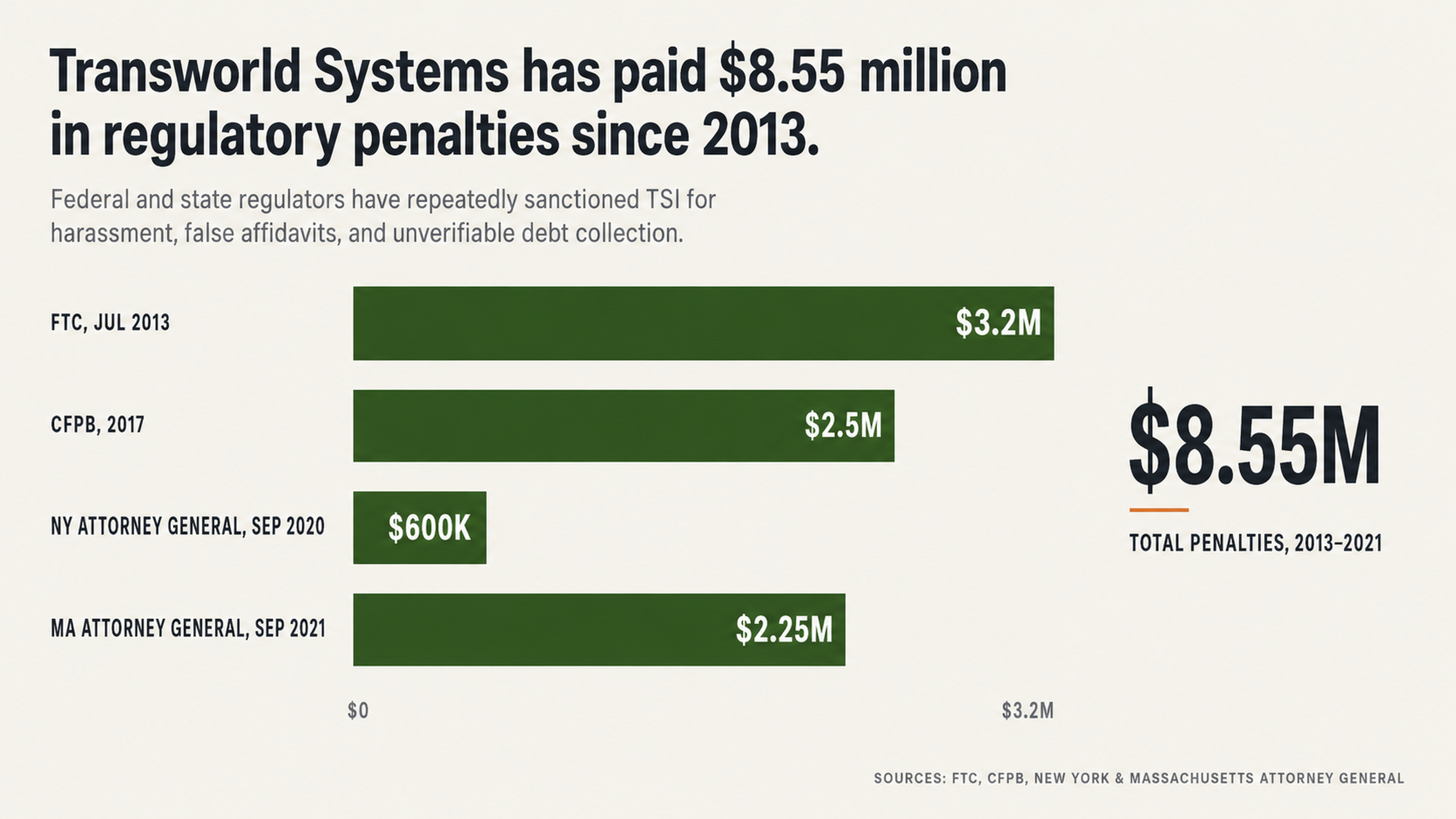

TSI Collections History of Violations

Although the company has been around for a while and is one of the largest in the industry, it has had some issues. In fact, since 2013, the company has paid $8.55 million in federal and state regulatory penalties and settlements, in just five cases.

In July of 2013, the Federal Trade Commission (FTC) imposed a penalty of $3.2 million on TSI, at the time the largest penalty ever imposed on a third-party debt collector. The penalty was the result of the company’s using harassment in the form of excessive calls, calling after the consumer requested they stop calling, and failure to validate the debt.

Four years later, the Consumer Financial Protection Bureau (CFPB) imposed a penalty of $2.5 million on TSI for filing false affidavits and attempting to collect debts that the company could not show consumers owed.

The list of violations goes on. In September of 2020, New York Attorney General Letitia James imposed a settlement of $600,000 on TSI, after the AG’s office determined that TSI used fraud and deception to attempt to collect from defaulted borrowers and secure default judgments on a mass scale.

One year later, in September of 2021, Massachusetts Attorney General Maura Healey imposed a settlement of $2.25 million on TSI for excessive calling and filing false affidavits.

The CFPB complaint database reveals similar issues. Over 10,000 complaints have been filed against TSI with the CFPB. Of those, 1,572 complaints were for attempting to collect debts not owed, 627 complaints were for problems with written notifications about debts, and 413 were for false statements or representations. These numbers indicate that we are not talking about isolated incidents here.

Why Paying TSI Collections May be a Huge Mistake

The Payment Trap

When you first see a collection account on your credit report, you might feel like calling the collector and paying the debt as quickly as possible. This may seem like the fastest way to deal with the situation. Before you do that, there are a few things you should know.

Paying a collection account does not remove the account from your credit report. Instead, it simply updates the status of the account to paid. The account will still remain on your credit report and will still be viewable by lenders for up to seven years from the original date of delinquency. So, in the scenario above, paying the debt immediately would have done nothing for you except cost you almost three thousand dollars.

When debt collectors are willing to negotiate a settlement by accepting less than the full balance due, this should tell you something about the nature of the debt. If they will accept 40 or 50 percent of the balance due, this means that the full balance due was not a hard and fast balance, but rather a balance they hoped to collect. This means the debt was likely sold to the collector for pennies on the dollar, and the balance they placed on the debt was the return they hoped to make on the debt.

The Documentation Issue

Part of the reason TSI has been penalized millions of dollars is because of their documentation procedures, or lack thereof. In fact, the CFPB determined that over 2,000 collection lawsuits were filed by TSI using documentation that was fundamentally flawed. In these suits, affiants signed documents under penalty of perjury in which they claimed to have personal knowledge of the business records. In reality, these affiants had no such knowledge.

In addition, the CFPB found that documents submitted to the courts as redacted versions of the original document were actually created for purposes of the litigation.

These findings mean that many of the debts being reported by TSI are likely without the documentation necessary to prove that the consumer actually owes the debt. When a debt collector purchases a debt portfolio that contains thousands of accounts, they often receive very little information about the individual accounts. In some cases, the account balance may be wrong or the account number may be wrong. In some cases, the debt may have already been paid to another collector or to the original creditor.

Therefore, if you believe a debt TSI is attempting to collect from you has an error or inaccuracy in it, you should demand they prove you owe the debt before you pay it.

Strategies for Dealing with TSI Collections

Know Your Rights

Information is power and this is never truer than in debt collection. The debt collection industry survives on information about alleged debts that consumers cannot verify on their own. They use urgency, threats, and a barrage of questions to pressure consumers into paying debts immediately.

Consumers should know that their rights under the Fair Debt Collection Practices Act (FDCPA) allow them to remain silent in the face of collection calls. In fact, every question a debt collector asks is designed to provide them with more information than they need to collect the debt. Before answering any questions, consumers should evaluate the benefit of their response. In most cases, consumers do not need to respond at all.

Reading consumer reviews of TSI can help. One consumer reported in September of 2025 that, “TSI calls me every day, several times a day from different phone numbers. I owe them nothing.” Another consumer reported in August of 2025 that, “I asked for proof of debt. They sent me a typed up paper that stated nothing about the contract, nothing about the original creditor, nothing.”

These reviews illustrate a debt collection agency that relies on pressure more than documentation to collect debts.

Disputing the Account

Consumers have the right to dispute any information on their credit reports they believe may be inaccurate or incomplete. Under the Fair Credit Reporting Act (FCRA) consumers have the right to dispute directly with the credit reporting bureaus any information on their credit reports they believe may be inaccurate or incomplete.

The credit reporting bureaus have 30 days to investigate consumer disputes. This creates a timeline that works to the consumer’s advantage. Debt collectors who have purchased debt portfolios with incomplete documentation on the accounts may not be able to respond to consumer disputes within the 30-day timeline. If they cannot verify the information disputed by the consumer, the credit reporting bureaus must delete the information.

This is not a loophole or technicality. This is the law working as intended when Congress created it to protect consumers from inaccurate credit reporting.

TSI Collections Consumer Complaints

Patterns of Behavior

If you type TSI Collections into your favorite search engine and add reviews, you will likely come across hundreds of reviews from consumers about their experiences with TSI. On the consumer review platform PissedConsumer, TSI has a rating of 1.4 stars.

The Better Business Bureau (BBB) reports that over 1,055 complaints have been filed against TSI in the last three years, with 344 of those coming in the last year alone. Of those complaints, 81 were related to billing issues.

Many of the complaints are about many of the same issues. Consumers report that TSI is attempting to collect medical bills they have already paid. They report that TSI is attempting to collect debts beyond the statute of limitations. Many consumers indicate that when they requested validation of the debt, they received inadequate documentation or no response at all.

In November of 2025, one consumer filed a complaint with ConsumerAffairs that read in part: “TSI is trying to collect money from me that I do not owe. I was never contacted at my last known address. When I called to inquire about the charge they recently added to my credit report, they refused to provide me with the original bill or any proof that they ever sent me an original bill.”

Consumers consistently report that TSI is placing debt collection accounts on their credit reports without providing them the documentation they need to verify the debt.

TSI Collections Lawsuits

When debt collectors violate federal and state consumer protection laws, consumers have the right to file lawsuits against them to recover damages. TSI is no exception. The company has been the subject of thousands of federal and state lawsuits. In fact, over 480 federal lawsuits against TSI for violations of the federal Fair Debt Collection Practices Act (FDCPA) and state consumer protection laws can be found in the federal court database Pacer.

Some recent cases are worth mentioning. In 2023, a class action case was filed against TSI for allegedly sending collection letters to consumers that grossly mischaracterized elements of the debt and failed to disclose that the debt was time-barred. Also, in 2023, the Ninth Circuit Court of Appeals reversed a lower court decision dismissing a lawsuit against TSI that claimed the company knowingly filed meritless debt collection lawsuits against consumers.

These cases matter because they demonstrate that courts continue to find TSI’s practices worthy of their attention.

Why You Need Professional Help from a Credit Repair Company

Effectively disputing information on your credit report requires knowledge of federal and state consumer protection laws and time to devote to the process. While you may be able to handle the dispute on your own, you should consider seeking professional help from a credit repair company.

Keep in mind. We are not talking about hiring a company to help you avoid debts you owe. We are talking about hiring a company to help you make sure debt collectors are following the law and placing only accurate and verifiable information on your credit report.

If TSI has paid over $8.55 million in regulatory penalties because they were not following the law and were filing false affidavits and pursuing debts without proper documentation, you have every right to demand they prove you owe the debt before you pay it or allow them to leave it on your credit report.

Credit repair professionals understand the laws and procedures in place to protect consumers and they have the time and expertise to help consumers through the process.

Final Thoughts

TSI Collections on your credit report is not the end of the world and does not mean you have to accept the damage or pay them what they are asking for. This is a company that has paid millions of dollars in regulatory penalties, had thousands of consumer complaints filed against it, and been the subject of a lot of class action lawsuits because of the way they handle debts.

The company has documented issues with documentation and verification procedures and debt collection practices that provide consumers with the opportunity to get accounts removed from their credit reports.

The point is, do not pick up the phone or mail a check. Understand your rights and demand verification. If necessary, seek professional help. Collections can be removed from credit reports when the information is incorrect, erroneous, fraudulent, or cannot be verified within the applicable timeframe. Given TSI’s history, many of the accounts they are reporting may fall into one of these categories.

Do you have TSI Collections on your credit report? If so, you do not have to go it alone. At FightCollections.com, we specialize in representing consumers in disputes with debt collectors. Our team understands the unique issues consumers face when dealing with TSI and the best strategies for successfully dealing with them.

Take the first step in reclaiming your financial health today. Request your free consultation from our team of consumer advocates and let us review your credit report for errors and inaccuracies and develop a strategy for your individual circumstances.

You have the right to accurate credit reporting. Let us help you. Don’t let a debt collection account from a company with TSI’s history decide your financial future. Contact us at FightCollections.com today.