A mysterious collection account can land on your credit report and get your heart racing. If the account belongs to Unifin, you might feel a sense of dread wash over you, especially considering the dozens of complaints Unifin has had lodged against it with various consumer protection agencies.

Fortunately, you aren’t helpless when Unifin is listed on your credit report. You have options beyond paying what they say you owe.

It’s tempting to believe that you have no choice but to pay a collection account or leave it on your report once it appears. That’s what the debt collection companies hope you’ll think, at any rate. But the truth is, you have a lot more power in this situation than you probably realize. Keep reading to learn how you can fight back and clear your report.

Unifin is a debt collection company with a physical location in the Chicago, IL area. The company was incorporated on June 8, 2011, in Illinois and describes itself as a veteran-owned business. Unifin has been in business since June 2011 and is classified as a medium sized organization. Unifin primarily collects debt for credit card companies, banks, medical billing companies, telecom companies, utilities, and government backed loans such as those owed to the U.S. Department of Education.

Contact Information for Unifin

Here’s the information you need to know about Unifin:

Unifin is a debt collection agency that works with credit card companies, banks, medical providers, telecom companies, utility companies, and government agencies (including the U.S. Department of Education) to collect debts that are owed. They operate a 400-seat call center in Niles, IL, but they also have operations in Guatemala, Jamaica, the Philippines, and Latin America.

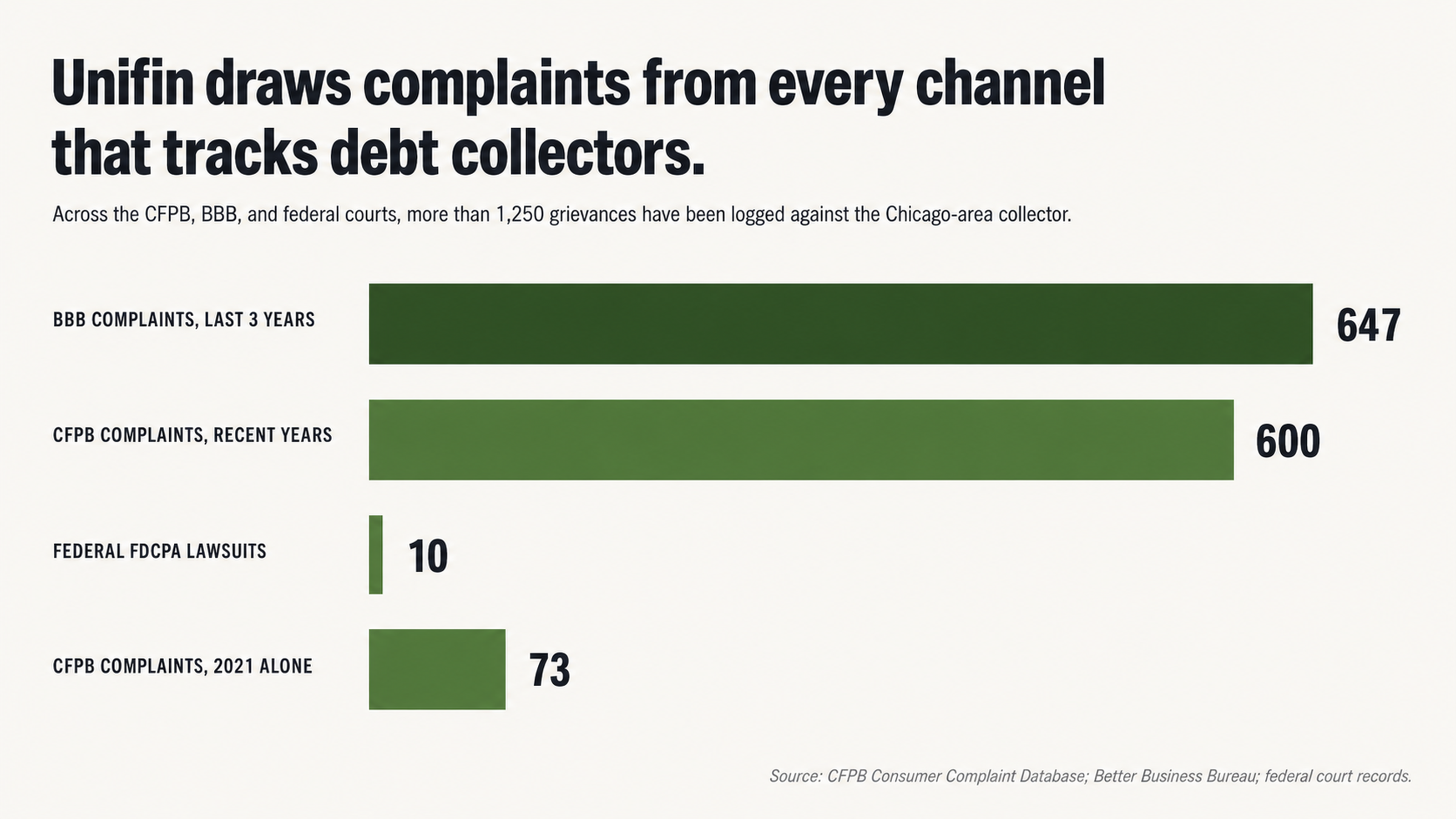

What is Unifin’s Reputation?

Unifin has had over 600 complaints filed against it with the Consumer Financial Protection Bureau (CFPB) in recent years. In 2021 alone, the CFPB received 73 complaints about Unifin. This ranks the company 335 out of all companies in terms of the number of complaints received in 2021.

The Better Business Bureau (BBB) reports that over 647 complaints have been filed against the company in the last 3 years, with 329 of those complaints being closed within the last year.

Unifin has also faced disciplinary action from the state of North Carolina. In 2016, Unifin entered into a Voluntary Settlement Agreement with the North Carolina Department of Insurance. They have also been sued in federal court at least 10 times for their allegedly illegal collection practices. One of the suits was a class action filed in March 2022 in the U.S. District Court for the Southern District of Florida.

Many of the complaints against Unifin describe unlawful debt collection practices, including: harassment (calling/texting repeatedly), incorrect identity (attempting to collect from the wrong person), zombie debt (attempting to collect on debts that are beyond the statute of limitations or have already been paid), and failure to validate debts.

The Unifin Myth of Immediate Payment

Don’t fall for the myth that you need to pay a collection account as soon as you see it on your report. While it might seem like the right thing to do, you’re essentially wasting your money. Paying a collection account will update the account’s status to “paid collection,” but it will still remain on your credit report for up to 7 years from the original delinquency date.

Debt collectors want you to pay them as soon as possible because it’s cheaper for them to operate that way. The longer they have to dispute a debt, the more it costs them in employee time, paperwork, etc. If you pay a debt right away, you’re giving them exactly what they want. You have a lot more leverage if you drag the dispute out.

Consider this complaint that was filed with the BBB against Unifin in Dec. 2025:

"I am continually receiving text from Unifin debt collector. I do not have any past debt and have always had good credit. I have not responded not knowing if this is a scam or if they think legit they have the wrong person. It is getting to be harassing receiving these."

This consumer is smart to not respond right away. In fact, it’s always better to err on the side of caution in a situation like this.

The Epidemic of Credit Report Errors

Did you know that up to 79% of all credit reports contain errors or inaccuracies? This statistic should always be in the back of your mind when dealing with a collection account. If almost 8 out of 10 credit reports contain errors, why should you assume a collection account is accurate?

Just consider this complaint that was filed against Unifin on SoloSuit:

"I just received a letter in the mail from Unifin stating I owe $1,xxx for a debt. I know for a fact this debt was paid off in 2016. It has been 6 years. My credit reports all say this credit card is paid off and the amount due is $0 and it’s not in collections. I also bought my first house last year and during the process they never said this was in collections at all."

This is just one example, but the point is, you should proceed with caution.

You can get a collection removed from your credit report if the information is inaccurate, incorrect, a mistake, or if they cannot verify the account within a reasonable amount of time. The burden of proof is on the collection agency to prove that the debt is valid, the information is accurate, and the debt is within the statute of limitations. This isn’t a loophole or a technicality. This is the law.

Your Strategic Advantages

Strategic Silence

There’s a common myth that states ignoring a debt collector will only make the situation worse. But the opposite is true. Sometimes, your best strategy is to say nothing at all.

Collectors need you to engage with them. They need you to call them back, talk to them, and negotiate with them. When you don’t give them that, you hold a lot of power.

When you talk to a debt collector on the phone, anything you say can and may be used against you. The relationship should always be entirely one way. Information should only flow from them to you. You don’t have to confirm your identity, acknowledge a debt, or give them any financial information over the phone. Any information you provide them is a weapon they can use against you later.

Just consider this complaint that was filed against Unifin:

"When I asked him to explain, he hung up. I pity anyone who does know their rights under the Fair Debt Collections Practices Act and has these vultures calling them. They are harassing, demeaning, insulting, and just plain rude."

When debt collectors can’t get what they want, they get frustrated. And when they’re frustrated, they’re likely to make mistakes.

The Power of a Paper Trail

If a debt collector makes you a promise over the phone, it means almost nothing. If a collector tells you they’ll remove the account from your credit report if you pay it, they’re probably lying. If they tell you they’ll settle with you for 50% of what you owe, that’s not a legitimate agreement. If they tell you they’ll stop reporting negative marks to the credit bureaus, don’t believe them.

Promises made over the phone mean almost nothing. If you pay a collector and they fail to follow through on their promises, you have no recourse. You can’t take them to court over a verbal agreement because it doesn’t exist.

But if you create a paper trail, you can protect yourself. Never send a debt collector money unless you have a written agreement that they’ll settle with you for that amount. Never give a collector financial information unless you have it in writing that they’ll use the information for a legitimate purpose.

When you communicate with a collector, always do it in writing. Send them letters via certified mail with return receipt requested. Keep everything in writing so you have proof if you need it later.

Consider this complaint that was filed against Unifin:

"I called to get info on the business and their employees were extremely rude. I told one agent I wanted the info on the business so I could file a complaint and he said ‘that’s fine, you can do whatever you want’ and hung up."

This collector is content to yell at people over the phone, but if they’re forced to respond in writing, they might sing a different tune.

You Should Dispute All Debt Information

Claims You Owe What a Debt Collector Claims You Owe

A consumer’s biggest mistake is to assume that they owe what a debt collector says they owe. This is a very dangerous assumption to make. Debt is bought and sold. Records are lost. People are confused with other people. The statute of limitations expires. Every collection account should be disputed because errors are just too common to assume you owe what a debt collector claims you owe.

Another December 2025 complaint to the Better Business Bureau:

"December 17, 2025 I received a letter stating I owed $2,823.09. I contacted [the company] they confirmed the account was closed. I am 90 years old, I believe they are trying to scam the elderly."

This may be intentional fraud or it may be simple error. In either case, had this consumer paid without disputing the debt, the outcome would have been the same.

Debt collectors benefit from information asymmetry between debt collectors and consumers. Debt collectors know the system, the laws, and the loopholes. Most consumers do not. Information asymmetry creates an environment in which debt collectors can use urgency and fear to collect payments on debts that may not be valid or may not be legally collectable.

Dispute-First Philosophy

Rather than assuming a collection account is valid until proven otherwise, it makes much more sense to assume the opposite: all collection accounts should be disputed. Errors are so common, it makes sense to approach collection accounts with a healthy dose of skepticism rather than blind trust. This is not about avoiding debts you may owe. It is about not paying debts you do not owe or debts that are no longer valid.

Under federal law, a debt collector must be able to validate a debt they are attempting to collect. They must show documentation of the original creditor, the amount of the debt, and proof the debt is yours. When they cannot do this, which is more often than you might imagine, the collection account has no legal basis to remain on your credit report.

One consumer complaint to the Better Business Bureau is typical of the documentation problems that occur in the debt collection industry:

"When I asked a question about the account, the lady skipped my question and started reading an extremely long script that had absolutely nothing to do with what I asked. I then asked her if she had a date of service, she replied no and hung up."

A debt collector who cannot answer basic questions about a debt is unlikely to be able to survive a formal dispute process.

Why You Need Help from a Professional

Why You Should Not Represent Yourself

While a consumer has every right to represent themselves in disputing a collection account, the reality is that hiring a professional usually generates better results. Credit reporting agencies and debt collectors respond differently when communications come from professionals rather than consumers.

Information asymmetry that favors debt collectors over consumers works to the consumer’s advantage when professionals get involved. Credit repair specialists know the games debt collectors play, they know the laws debt collectors commonly violate, and they know which pressure points will force action. They speak the language of compliance and consequences that debt collectors understand.

Unifin has been named in at least 10 federal lawsuits for violating the Fair Debt Collection Practices Act. Claims include: deceptive settlement offers, improper disclosure of consumer information to third parties, failure to validate a debt, and using unfair means to collect a debt.

A consumer advocate will recognize these violations where an individual consumer may not.

What a Professional Advocate Can Do for You

A credit repair professional will thoroughly investigate a collection account for accuracy, documentation issues, or other violations of law. They will prepare a dispute letter that uses the right language to get the right response and follow up in the right way to force credit reporting agencies to do their jobs. This is a time consuming process that requires specialized knowledge that most consumers do not possess.

When debt collectors cannot validate a debt or continue to report inaccurate information, a professional advocate knows how to escalate the situation appropriately. They know when to file a complaint with the Consumer Financial Protection Bureau or a state Attorney General and when other remedies are more appropriate. This is knowledge that translates into leverage that individual consumers rarely possess.

The point here is not to help consumers avoid debts they may owe but to make sure only accurate, valid, and legally collectable debts ever appear on a credit report. Given that nearly 80% of credit reports contain at least one error, consumers need this kind of protection. It is not a luxury. It is a necessity.

Bottom Line

Having Unifin on your credit report is not the end of the world. In fact, it may be just the beginning of the process to remove an inaccurate or invalid collection account from your credit report. The myths that debt collectors use to their advantage – you must pay now, you cannot dispute a debt, if you ignore this it will go away – all serve the debt collector. They do not serve the consumer.

The history of consumer complaints, regulatory actions, and federal lawsuits against Unifin mean that Unifin’s debt collection practices invite scrutiny. If a debt collector has this kind of history, it is even more important to question assumptions of accuracy. Your rights under the Fair Debt Collection Practices Act and the Fair Credit Reporting Act are designed to protect you against debt collection practices that favor speed over accuracy.

What to Do Next

Do not let Unifin or any debt collector push you around and dictate your next move. The dispute-first strategy protects consumers against paying a debt they do not owe and ensures any debt they do owe is properly documented and validated. This is not about scamming the system. This is about using the system the way it was designed.

FightCollections.com specializes in pushing back against debt collectors by disputing inaccurate information on credit reports and holding debt collection agencies to account. We know the games companies like Unifin play and we know how to respond.

If Unifin is on your credit report, we can investigate the account, identify potential violations, and seek removal through the proper legal process.

Contact FightCollections.com today for a free consultation. Let our advocates even the playing field and get you the accurate credit report you deserve.