When you find Westlake Portfolio Management on your credit report, it’s like a punch in the face. You didn’t see the account coming, you don’t recognize the balance, and you just got knocked in the face with a credit score drop.

In the initial moments of discovering a collection on your credit report, most people make massive mistakes. These mistakes will follow you for years and years to come. You want to pay the debt off and make it go away. I get it. Unfortunately, that’s one of the worst moves you can make. You see, many collection accounts can be deleted from your credit report through a dispute process. This is especially true when you’re dealing with companies who have a long history of violating laws and regulations.

So, who is Westlake Portfolio Management?

Westlake Portfolio Management, LLC is a debt collection and loan servicing company based in Los Angeles, California. The company specializes in auto loans and services these loans for several different clients. Sometimes they acquire auto loan portfolios from other companies and service them for themselves.

Here is some basic information about Westlake Portfolio Management:

Westlake Portfolio Management is not a scam. They are a real debt collection company registered in several states and operate as a subsidiary of a large corporation. Unfortunately, that doesn’t mean they play fair. This company has racked up hundreds of consumer complaints over the years.

What the Numbers Say

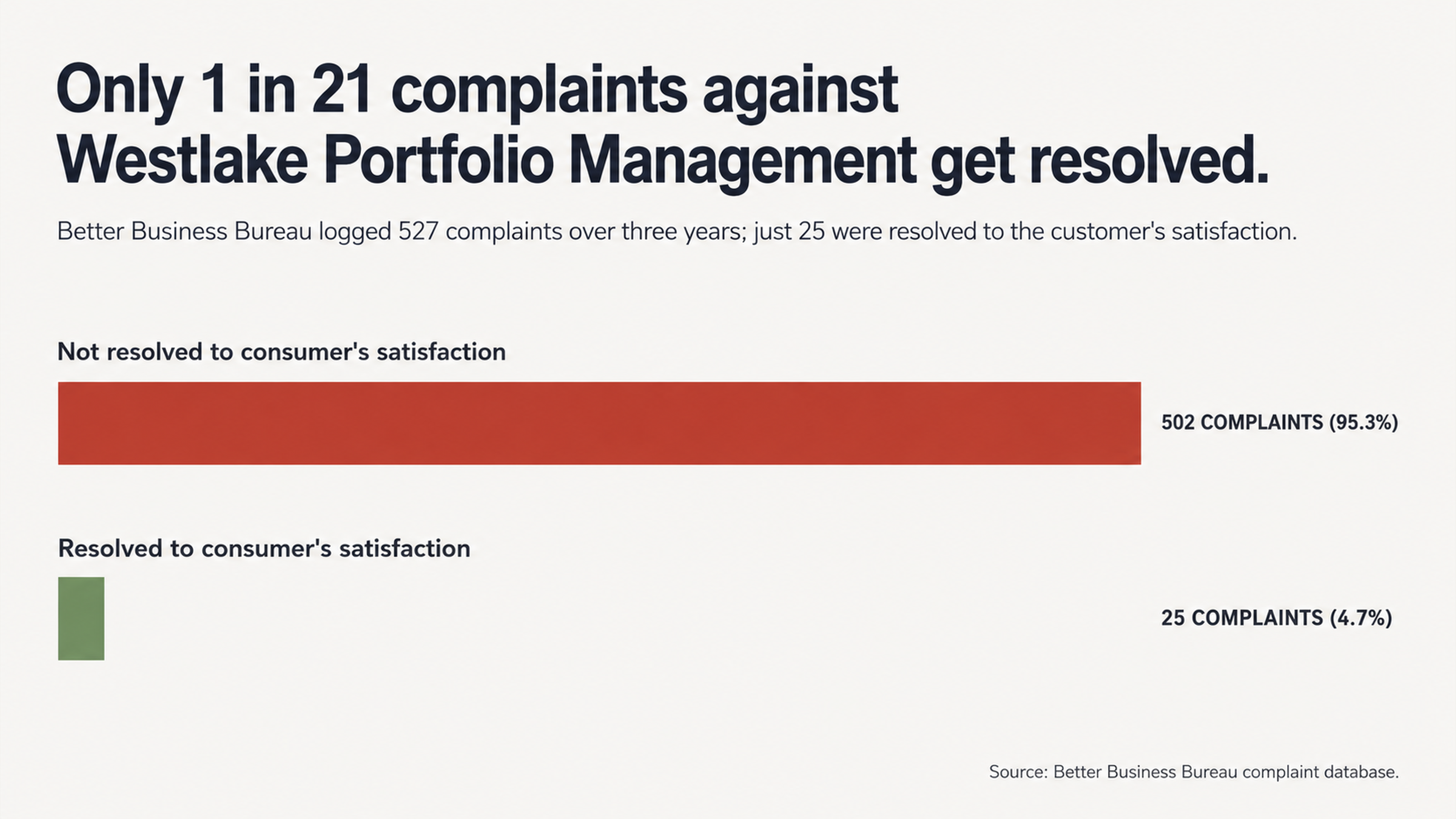

After some digging, it becomes clear that Westlake Portfolio Management has a bad reputation in the industry. Here are some numbers that you should find interesting:

- Over the last three years, the Better Business Bureau has received 527 complaints about this company. Only 4.7% of these complaints were resolved to the customer’s satisfaction.

- The average rating on Trustpilot is one star. In fact, 91% of their reviews are one-star reviews.

- On Pissed Consumer, Westlake Portfolio Management has a rating of 1.0 out of 5 stars.

Several of the common complaints against this company include:

- Not releasing titles on paid-off vehicles in a timely manner. Sometimes this takes several months or even years to resolve.

- Ignoring autopay set up with other loan servicers when the loan is transferred to Westlake.

- Repossessing vehicles without properly notifying consumers.

In 2015, Westlake’s parent company, Westlake Services LLC, paid $48.35 million to resolve a Consumer Financial Protection Bureau (CFPB) enforcement action. According to the CFPB, the company was using fake caller IDs to disguise themselves as pizza delivery places or family members calling to talk to borrowers. They were also making false threats of criminal prosecution and illegally disclosing information about debts to employers and family members of borrowers.

Mistake #1: Paying the Collection Without Verification

One of the biggest mistakes consumers make when they find a collection on their credit report is to pay it off immediately. This seems like a good idea. After all, don’t you want to pay off your debts and make them go away? The answer to that question is yes, but there is a catch.

Credit reports are not always accurate. In fact, research conducted by consumer advocate groups indicates that up to 79% of credit reports contain errors or discrepancies. This could mean someone else’s account is on your report. It could mean the balance is wrong. It could mean the account is a duplicate of something already on your report. Or, it could mean that the debt has already been paid or discharged.

When you’re dealing with Westlake Portfolio Management, in particular, the risk of inaccuracies is higher. The company has taken over the loans of several bankrupt companies, including US Auto Sales in May of 2023. Many of the complaints filed with the BBB describe issues where payment records have been lost, autopay set up with other servicers are ignored, or consumers are pursued for debts they already paid the original creditor.

Paying a collection account is not going to make it disappear from your credit report. Instead, it’s just going to change the status of the account from unpaid to paid. You’ll still have a negative account on your credit report for seven years from the date the account first became delinquent. This is going to negatively impact your credit score the entire time.

Additionally, when you make a payment on a collection account, you may be restarting the clock on the statute of limitations for that debt. In some states, if you make a payment on an old debt, the statute of limitations clock will start over. This means that a debt that couldn’t be pursued in court a few months ago, can now be pursued. Don’t pay unless you’re sure the debt is valid and yours.

Mistake #2: Trusting Pay for Delete Promises

Many consumers try to negotiate a pay for delete with collection agencies. This is when you offer to pay off the collection account in exchange for the agency deleting the account from your credit report. This seems like a fair compromise, but it rarely works out in your favor.

The Fair Credit Reporting Act requires credit bureaus to ensure the accuracy of credit reports. This means that they can’t just arbitrarily delete information because someone makes a phone call. Even if a collector agrees to delete an account after you pay it off, they may not follow through on their promise. This means you’ll pay off the full balance, but the negative mark will stay on your report for the full seven years.

Westlake Portfolio Management has been named as a defendant in at least eight federal lawsuits accusing the company of violating various consumer protection laws, including the Fair Debt Collection Practices Act (FDCPA) and the Fair Credit Reporting Act (FCRA). It’s unlikely that a company facing that kind of litigation is going to follow through on an agreement to illegally delete information from your credit report.

Instead of trying to negotiate a pay for delete after paying off the balance, you should challenge the accuracy of the account before you pay it off. If the information is inaccurate, fraudulent, unverifiable, or if the collector can’t provide documentation within the allotted timeframe, the account can be deleted from your report entirely. This isn’t a loophole, this is a federal law.

Mistake #3: Failing to Request Documentation

When consumers ask a collection agency to validate a debt, they assume the agency will just send them a form letter letting them know the debt is valid. Instead, a request for documentation is a proactive step you can take to dispute the debt. Sometimes this will expose some weaknesses in the collector’s position.

The Fair Debt Collection Practices Act (FDCPA) says that consumers have the right to request validation of a debt. This isn’t just about asking the collector to confirm that you owe the debt. Instead, you need to ask for proof including:

- The original creditor

- The amount you owe

- Documentation showing you’re responsible for the debt

If a debt collector is collecting on a debt they purchased from someone else, they may not have all of the documentation they need to respond to your request. This could include the original loan agreement, payment history, and chain of ownership. If they can’t respond adequately to your request, they aren’t allowed to continue collecting on the debt and should remove it from your credit report.

Westlake’s weakness when it comes to documentation mostly stems from the fact that they’re taking over loan portfolios from other companies. For example, Westlake Portfolio Management took over the portfolio of US Auto Sales when the company went bankrupt in May of 2023. Many of the complaints filed with the BBB describe consumers whose payment records were lost in transition. Others describe autopay set up with the previous servicer that isn’t being honored.

A class action lawsuit was filed against Westlake Portfolio Management in a California federal court in 2024. The lawsuit, titled Hueston et al v. Westlake Portfolio Management LLC, accuses the company of trying to collect on auto warranty plans that don’t exist. According to the suit, the company misrepresented the amounts their clients owe them and violated UCC provisions requiring proper notice before repossessing a vehicle.

Mistake #4: Responding to Guilt and Pressure Tactics

Debt collectors know how to work with people. They understand that most consumers feel a sense of moral obligation to pay their debts. So, they use guilt and pressure tactics to get consumers to take action quickly. One of the BBB complaints against Westlake Portfolio Management describes the company sending consumers letters threatening action instead of invoices for their debts. According to the complaint, the letter says if they don’t pay, they may repossess the car.

When consumers respond to guilt and pressure, they’re allowing the collector to dictate how they’ll proceed. Instead of taking the time to verify the debt and make sure everything is correct, consumers end up paying off the balance as quickly as possible.

Westlake Services LLC, the parent company of Westlake Portfolio Management, paid $48.35 million to resolve a CFPB enforcement action in 2015. According to the Bureau, the company was making false threats about prosecuting consumers criminally. They were also using phony caller ID to disguise themselves as the consumer’s family member or a pizza delivery place on over 137,000 loan accounts. If you’re dealing with a company whose parent has engaged in this kind of behavior in the past, you should expect that they’ll try to use guilt and manipulation to get what they want from you.

Instead of responding to these tactics, you should ignore them. You aren’t obligated to talk to a debt collector on the phone. You don’t have to respond to their letters or emails. If you want to dispute the debt or request documentation, you should do so in writing through the proper channels. This will ensure you have a paper trail to refer back to later if you need it.

Mistake #5: Going It Alone

Finally, many consumers try to deal with a collection agency on their own without any professional assistance. While you certainly have the right to do this, the reality is that the collection agency has probably dealt with dozens of consumers this week alone. They have a system down for handling disputes and they know how to brush consumers off.

Why You Need Professional Help

Professional credit repair experts understand what documentation you need to request and when. They understand the deadlines you need to meet and the steps you need to take to maximize your chances of successfully removing a collection account from your report. They’ll also know which disputes are most likely to work and how to word your disputes to ensure the collection agency responds the way you want them to.

If you’re dealing with a company like Westlake Portfolio Management that has been sued in federal court multiple times for violating the FDCPA and FCRA, you need professional help. Attorneys who specialize in consumer law and credit repair specialists know the ins and outs of these cases. They understand the strengths and weaknesses and know how to use them to your advantage.

The stakes are too high for you to go this alone. A collection account from Westlake Portfolio Management can stay on your credit report for seven years. During that time, it could affect your ability to get a mortgage, an auto loan, a credit card, or even a job. Some consumers have reported to Trustpilot that they’ve paid more than double the original amount they borrowed because of the financing terms offered by Westlake.

Over the course of seven years, the difference between a successful dispute and an unsuccessful one could be tens of thousands of dollars in interest. For many consumers, hiring professional help is worth it just for the money they’ll save in interest over the course of seven years.

Conclusion

Westlake Portfolio Management is a debt collection company operating as a subsidiary of a larger corporation that has paid almost $50 million in federal fines for violating debt collection laws. The company itself has racked up hundreds of consumer complaints over the last few years and is currently facing several federal lawsuits accusing them of violating various consumer protection laws.

That doesn’t mean that every debt that Westlake Portfolio Management is collecting is invalid. However, it does mean that as a consumer, you should proceed with caution when dealing with this company. The errors, documentation issues, and law violations listed above provide you with plenty of ammunition to dispute the account with the credit bureaus.

What to Do Next

If you see Westlake Portfolio Management on your credit report, don’t pay it. Don’t panic. And, whatever you do, don’t engage with their pressure tactics. Instead, the account may be eligible for deletion through the dispute process. Especially considering this company’s history of law violations and consumer complaints.

FightCollections.com is a website dedicated to helping consumers fight debt collectors and remove questionable collection accounts from their credit reports. We understand the weaknesses of companies like Westlake Portfolio Management and know how to use federal consumer protection laws to your advantage.

Contact us today for a free consultation. Our specialists will review your credit report and evaluate the Westlake Portfolio Management account. Then, we’ll help you come up with a strategic plan to dispute the account and potentially remove it from your report. Your credit report depends on you making the right moves now instead of the wrong ones later.