ARS Solutions, LLC., (ARS) Known As: Asset Recovery Solutions is an Illinois-based debt collection agency whose existence goes back to 2009.

In that time, they have compiled an extensive history of consumer complaints filed with the Consumer Financial Protection Bureau and the Better Business Bureau. Prior to attempting to contact them or pay the debt, consumers should confirm that the information is accurate in order to avoid making a financial mistake.

The Collection Agency’s Information is As Follows:

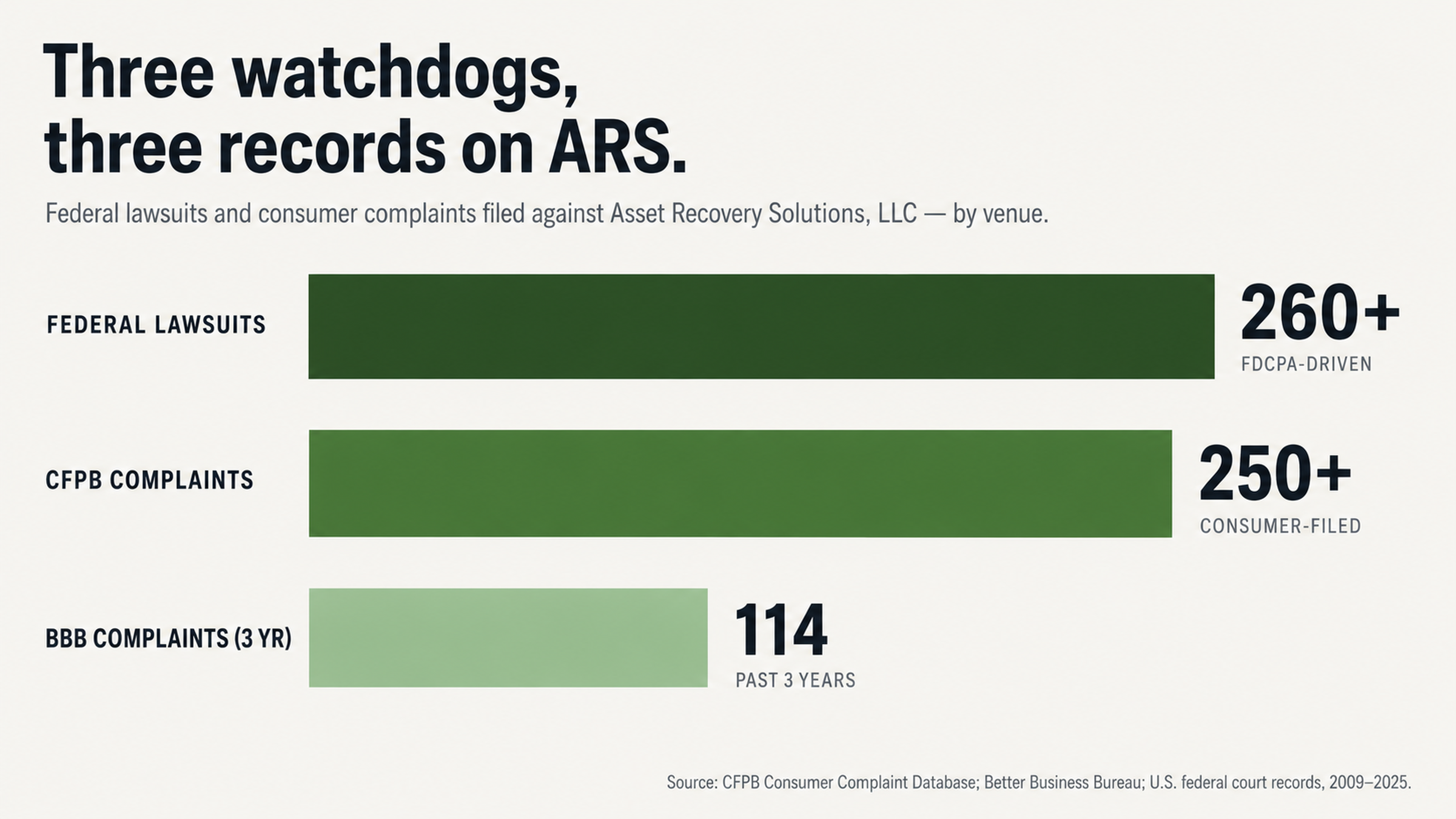

ARS has over 260 Federal lawsuits filed against them, mostly for violating the FDCPA. More than 250 complaints have been filed with the Consumer Financial Protection Bureau.

On the Better Business Bureau website, there are over 114 complaints filed in the last 3 years, with only 28.1% of them being resolved satisfactorily. Despite an A+ rating with the Better Business Bureau, the company has a 1-star rating with only 25 reviews.

The reason for the discrepancy is that the BBB rating is based on how a company responds to complaints, not on the customer satisfaction of the complaints themselves.

Reasons to Question the Legitimacy of the Collection Account

Inaccurate Collection Account Information

Anytime you find an unknown collection account on your credit report, it is essential to scrutinize every aspect of the account to ensure it is legitimate and accurate. Look for account numbers that you do not recognize and balance and past due amounts that do not make sense. Check the reported date of last payment and the date of first delinquency to ensure that it is your account.

A perfect example of why it is crucial to scrutinize the information is a complaint filed with the Better Business Bureau in November 2025. The complainant stated that their credit report showed the collection account with an original balance of $0.00, past due amount of $0.00, with no payment history, yet the account was reporting as a collection with a balance due of over five thousand dollars.

This type of discrepancy is an example of an inaccuracy that should be disputed to have the account removed from the report.

Collection accounts that were included in a bankruptcy should also raise a red flag.

In a complaint filed in September 2025 with the Better Business Bureau, the complainant claimed that Asset Recovery Solutions was attempting to collect a debt despite the debt being included in a Chapter 7 bankruptcy. The original creditor had already reported the debt as discharged from bankruptcy. Attempting to collect on this debt may be a violation of the bankruptcy discharge order.

Inadequate Information

Legitimate collection accounts should have all of the necessary information to validate that it is your account and that all of the information is correct. If there is missing information, it may indicate a problem with the collector’s documentation and may aid in having the account removed. Examples include:

• The original creditor name is missing

• The original account number is missing

• There is an unclear description of what makes up the debt

According to a study by U.S. PIRG, approximately 79% of all credit reports contain some type of mistake or serious error. Therefore, anytime there is incomplete information or something seems fishy; it is likely that this could be grounds for removal from your credit report. The burden of proof is on the collection agency to prove that the information is accurate and complete, not on you to prove that it is incorrect.

Paying the Collection Account May Not be the Best Option

Paying an unknown collection account may seem like the best option to avoid any potential consequences; however, this may not always be the case. When a collection account is paid, it is updated to show that the account has been paid; however, the negative information will still remain on your report. Therefore, paying a collection account does not necessarily mean that it will be removed from your report. The goal should be to have the account completely removed from your report.

A paid collection account will still show up on your report and may still negatively affect your credit score. This is because paying a collection account means that you had a debt go into collection, which is what the credit scoring formula does not want to see.

Why Collectors Try to Create a Sense of Urgency

Debt collectors will often try to create a sense of urgency to get consumers to pay debts as quickly as possible. This can be done by calling consumers multiple times per week or by making false statements to consumers.

According to a complaint filed with the Better Business Bureau in January 2026, a representative from Asset Recovery Solutions claimed that they were going to serve papers at the consumer’s home and their place of employment. Despite the threats, no one ever came to either location.

These are common tactics used in the debt collection industry. They want to create a false sense of urgency to scare consumers into paying a debt. It is essential not to fall for these tactics and to do your own research to determine the best course of action.

Using Your Credit Report as a Tool

Obtaining a Copy of Your Report

Under Federal law, consumers are entitled to one free copy of their credit report from each of the three reporting agencies per year. Requesting a copy of your report from each agency will help you to identify any differences in the way that the information is being reported from agency to agency.

ARS may report different balances to Equifax than they do to Experian or TransUnion. Alternatively, they may report different dates of first delinquency to one or more of the agencies. Any discrepancy should be disputed to have the account removed.

Documenting Inconsistencies

Any information that you find to be inconsistent or inaccurate should be well-documented. Make a copy of the information on your report, including the verbiage that they used to describe the account. Also, keep copies of any dates, balances or other information that you do not recognize. All of this information can be used to file a dispute and have the account removed from your report.

Keep detailed records of everything to ensure that you are prepared in the event that you need to escalate the situation by filing a complaint with the Consumer Financial Protection Bureau or with an attorney.

The information and complaints about ARS on the Better Business Bureau’s website can also be useful. The rating and the complaints are further evidence that this is a collector that has a history of having issues with consumer’s credit reports. This documentation can aid in disputing accounts with this agency to have them removed.

Filing a Dispute Prior to Paying

Error Rate Studies have shown that up to 79% of all credit reports contain some type of mistake or error. Therefore, before paying off an unknown collection account; it may be a good idea to dispute it to confirm that the information is accurate and complete.

ARS and most other debt collection agencies do not have the documentation to support the accounts that they are collecting on. It is not uncommon for this agency to purchase accounts from other collection agencies and attempt to collect on accounts without having any documentation to support their claims.

ARS was even the subject of a class action lawsuit in 2016. The lawsuit was filed in the Northern District of California and claimed that at least 10,000 people received collection letters from this agency that may have violated their privacy. This is an example of how debt collection agencies may not be in compliance with all laws and regulations.

Removing Inaccurate Information

Inaccurate, erroneous, fraudulent or unverifiable information should be removed from consumer credit reports. If you suspect that this information is on your report, you should file a dispute with each of the credit reporting agencies to have it removed. The credit reporting agency will contact the collection agency to have them verify the information. If they are unable to do so within a specified period of time, typically 30 days; the account should be removed from your report.

ARS has a history of failing to validate debts that they are attempting to collect. In several complaints filed with the Consumer Financial Protection Bureau, consumers claim that this agency is attempting to collect debts without documentation to support their claims.

Other consumers claim that the agency is attempting to collect accounts that the consumer does not recognize. Some consumers even claim that the agency is providing different balance information than what the consumer was previously aware of. In all of these situations, the information cannot be verified and should be removed from the consumer’s report.

Why You Should Hire a Professional

Knowledge is power when dealing with debt collectors. While you may have some knowledge about your consumer rights; chances are that the debt collector has more knowledge about the laws and regulations than you do. For this reason, it is a good idea to hire a professional to help resolve the issue.

ARS employs people who are knowledgeable about debt collection practices. In fact, the CEO of the company is a former employee of both Sallie Mae Bank and Arrow Financial Services. His knowledge of the debt collection industry may aid the company in attempting to collect accounts; however, with the right representation, consumers should still be able to have inaccurate information removed from their report.

Debt collection agencies do not want consumers to retain the services of professionals to aid in resolving unknown debts. This is because the collector will not have the upper hand and will be unable to use their tactics to get consumers to pay debts. Most likely, the professional that you hire will be able to get the debt removed from your report without paying the collection agency.

Communicating in Writing

Finally, insist on communicating in writing. This will ensure that you have a paper trail and written proof of what the debt collector is telling you. Unfortunately, the verbal statements of debt collectors cannot be trusted. Many consumers have filed complaints alleging that debt collectors have lied to them.

In one complaint filed with the Consumer Financial Protection Bureau; the consumer claimed that ARS added almost $7,000 in interest charges to a $10,000 student loan debt. The consumer was unaware of the additional charges and claims to have never agreed to them. The total amount due was over $17,000, which the consumer claims is double the original amount.

This is an example of why consumers should communicate only in writing and why they should retain the services of a professional to aid in resolving unknown debts.

ARS Solutions, LLC has many complaints filed against them for their collection practices. Before paying an unknown collection account or communicating with this agency, confirm that the information on your report is accurate and complete. If it is not or if you are unsure; consider hiring a professional to aid in resolving the debt.