If you have a collection from Professional Finance Company (PFC) on your credit report, you probably don’t want it. You may not even want it to be on your credit report at all.

Many people do the worst thing possible when they see a collection on their report from a debt collector like Professional Finance Company (PFC), and then wish they had not.

The debt collection industry makes a living from you not knowing your rights. Professional Finance Company is no different. In this article, we will go over the mistakes you should avoid when dealing with Professional Finance Company, and how to get your credit report the best it can be.

Who Is Professional Finance Company?

PFC, also known as PFC USA, is a third-party debt collection agency. They specialize in collecting medical debt and healthcare receivables. Their address is 5754 West 11th Street, Suite 100, Greeley, CO 80634-4811. Here is some more information about PFC.

What We Know About This Debt Collection Company

While PFC has an A+ rating with the BBB, there are other things you should know about this debt collection company. In 2022, Professional Finance Company agreed to pay $2.5 million to settle a class action after a ransomware attack exposed the personal and medical data of nearly 1.9 million patients. The data included social security numbers, details of medical treatment, and financial data across 657 healthcare provider clients.

In 2016, a federal judge found in Bledsoe v. Professional Finance Company, Inc. that Professional Finance Company’s standard collection letter was materially deceptive and misleading and violated several sections of the Fair Debt Collection Practices Act. The company had included boilerplate language warning of interest and late charges that did not apply to the debts they were collecting.

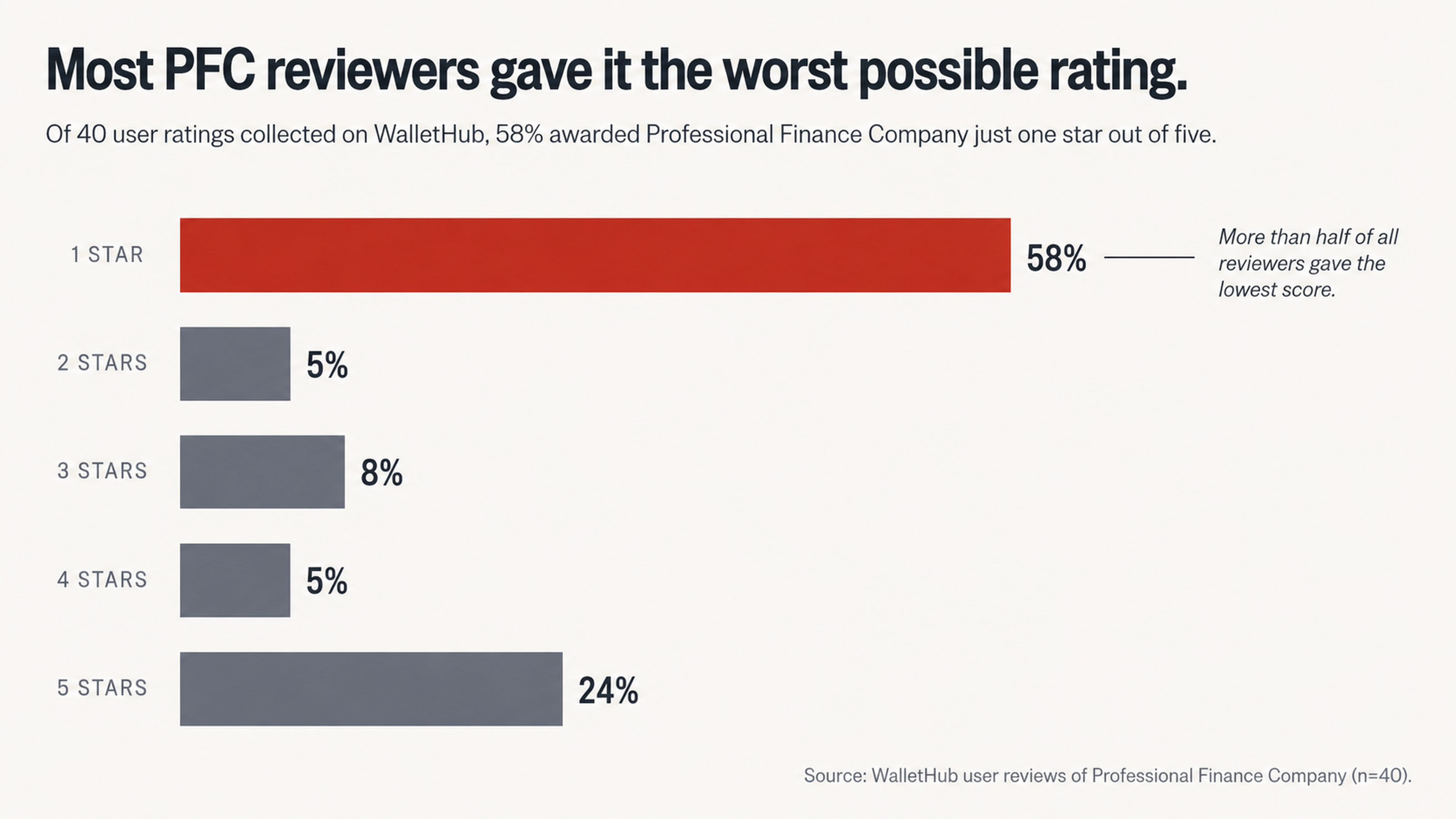

The average customer review of Professional Finance Company is 2 out of 5 stars. 58% of the reviewers on WalletHub gave them only 1 star. The Consumer Financial Protection Bureau has recorded 68 complaints against PFC that are now closed. The most common complaints were attempting to collect a debt that was not owed, failure to validate a debt, and incorrect credit reporting.

The 2 Worst Things Consumers Do When Dealing With PFC

Mistake #1: Making a Payment Right Away

Many consumers see a collection on their report and immediately pay it. While this is an understandable reaction, it is probably the worst thing you can do. If you pay a collection, it does not mean that the collection is removed from your report. It simply means that the status of the collection changes from unpaid to paid, and it will remain on your report for 7 years from the date it originally became delinquent.

This is what collection agencies like Professional Finance Company want you to do. They may use threatening language to make you feel like you have to pay them immediately. This is not the case. You have the right to request validation of the debt before you do anything.

You should request validation of the debt. Under federal law, you can request proof that the debt is yours, the correct amount, and proof that the debt collection agency has the right to collect the debt. Many collection debts are errors, and a study by U.S. PIRGs found that 79% of credit reports contained errors or serious errors.

Mistake #2: Calling the Debt Collection Agency

Most consumers see a collection on their report and immediately call the phone number listed. This seems like the right thing to do, but you should think twice before calling. Phone calls are not recorded. There is no paper trail. There is no way to prove what you said and what they said. What you say can be used against you.

When you talk to a debt collector on the phone, anything you say may be used as proof that the debt is valid. In some states, this may renew the statute of limitations on a debt that otherwise may have expired.

Debt collectors are professionals. They are trained in what to say to get consumers to pay debts or acknowledge them. You are not trained. Don’t put yourself at a disadvantage.

You should communicate with the debt collector in writing. Written letters provide a paper trail. Written letters can help establish what they said and what you said. Once you mail a letter, they must validate the debt and cannot attempt to collect until they provide that information.

Understanding The Fair Debt Collection Practices Act

The Fair Debt Collection Practices Act (FDCPA) is a federal law that provides consumers protection from debt collectors who engage in abusive and harassing behavior.

Some of the provisions of the FDCPA are: The debt collector must send you written notice of the debt within 5 days of contacting you. The notice must include the amount of the debt, the name of the original creditor, and a statement of your right to dispute the debt. If you dispute the debt within 30 days, the debt collector may not continue to attempt to collect until they send you verification of the debt.

As mentioned above, PFC was found to have violated the FDCPA for their collection letters. Any communication you receive from PFC should be analyzed to determine if they are complying with the FDCPA. Debt collectors who violate the FDCPA are liable for any actual damages you incur, up to $1,000 for each case, and attorney fees.

Many of the complaints against PFC were for failure to validate debts. One consumer reported that the representative she talked to at PFC “refused and hung up when I asked for verification.”

Understanding The Fair Credit Reporting Act

The Fair Credit Reporting Act (FCRA) is a federal law that provides consumers certain rights with regards to the information that appears on their credit reports.

Under the FCRA, consumers have the right to dispute any information on their credit report that they believe is inaccurate, incomplete, or unverifiable. When a consumer disputes information, the credit reporting agency must investigate the dispute within 30 days and remove the information if they cannot verify it.

This is a very important right. Many times, collection agencies do not have the documentation to verify the debt.

Debt collection agencies operate on volume. They probably have thousands of debts they are collecting. They probably do not have the documentation for most of them.

The debt collection industry is built on buying debts for pennies on the dollar. When a debt is sold from company to company, the original contract and history may get lost. If PFC cannot verify the information they placed on your credit report, the information must be removed.

Having a collection removed is the best possible outcome when dealing with a debt collector. It means the negative item will be completely removed and will not count against your credit score.

Why Disputing First Is the Smarter Strategy

Collectors Often Fail to Meet Their Obligations

The debt collection industry is a volume business. Firms such as Professional Finance Company collect so many accounts that they are not equipped to handle every dispute correctly. If a dispute is properly done and supported, many times the collectors find it cheaper to just move on to the next file rather than comply with your request.

When you read some of the reviews from consumers dealing with PFC, you begin to see some of these habits. “Every time I have called I get a different balance and story”, or “PFC has been trying to collect a debt from someone else and when I inform them that it is not me they still continue to try and collect the debt”.

If their documentation is not up to par, consumers who know the process have the upper hand. If they can’t produce the original contract, a correct payment history, and chain of ownership documents, they will not be able to verify the account on the credit bureaus.

The Math Favors Patient Consumers

Many consumers fear a dispute will result in a lawsuit.

Truthfully, very few debts are ever pursued in court because it is not cost-effective. The filing fees, attorneys’ fees, and time and money for court appearances can exceed the debt amount being collected. Most medical debts are very small, so it would be especially uneconomical to pursue these debts in court. Every file is run through some type of cost-benefit analysis to determine whether the account is worth the time, effort, and money. In most cases, the answer is no.

Therefore, time is actually on the side of consumers in many instances.

Credit repair is a marathon, not a sprint. Given that items only report for seven years, it is likely that if you just wait, the account will fall off of your credit report even if you never pay. Knowing that timeline can help you make better decisions rather than reactive ones based on fear.

What Professional Credit Repair Can Do

Why DIY Approaches Often Fall Short

The typical DIY credit repair approach might not get the best results for a couple of reasons.

For one, it’s hard to match the expertise that a professional firm would bring. Credit reporting is a technical field, and unless you make it your business to know all the ins and outs of the relevant laws and credit reporting practices, you are likely to miss some details.

Beyond the lack of technical knowledge, there is also the issue of resources. While you may dedicate however many hours you need to your dispute, there is also the question of what the other side is bringing to the table.

If you are disputing with a credit bureau or collection agency, you’re going up against an organization that handles these issues all day, every day. If you are dealing with an especially stubborn credit reporting error, you may find yourself outgunned.

The Advantage of Professional Intervention

Working with a credit repair firm like FightCollections.com offers a number of potential benefits, especially in the right situation. For one, they bring a lot of expertise to the table. Credit repair professionals understand the relevant laws, as well as how they are typically applied. This means they can identify issues that you might have otherwise overlooked, and help ensure that your dispute is handled as efficiently as possible. The learning curve is steep, and mistakes can be costly in terms of time and credit score impact.

Beyond their technical advantages, credit repair companies can also help serve as a kind of emotional buffer between you and the organizations you are disputing with. Disputes can get heated, and it’s easy to get drawn into an emotional back-and-forth. Handing the dispute off to a third party can help you avoid getting drawn into that kind of situation.

Finally, credit repair companies have a lot of experience handling the types of organizations you are disputing with. If you are disputing with a credit bureau or collection agency, they have likely dealt with that company before. This can help you leverage their knowledge of how that the company operates to help get the best outcome for your dispute.

Common Red Flags in PFC Collection Practices

Notification and Communication Issues

One of the biggest areas of concern with Professional Finance Company is in their communication and notification practices. According to the BBB reviews, one consumer reported that the only thing she received was “a vague and suspicious looking text message with a payment link”. That does not sound like the proper written notification that you are supposed to receive from a debt collector.

It is also worth mentioning that in 2022, the company experienced a data breach. The breach was detected on February 26, 2022. However, they did not notify affected healthcare providers until May 5, 2022. It took them over two months to notify the providers and even longer to notify affected individuals. If they are not communicating with providers or consumers in a timely manner, that may speak to a bigger issue.

If you are contacted by PFC, make sure that you are keeping detailed records of who contacted you, how they contacted you, and what was said. Any failure in the notification process can serve as grounds for a dispute.

Debt Validation Failures

We have seen several reviews that mention that PFC has failed to provide the proper validation when requested. In some instances, the consumer reports that they never received anything. In other instances, the consumer indicates that what was received did not adequately validate the debt.

Here is one example: “I asked to validate the debt and the woman told me she couldn’t do that and then she disconnected the call in my ear.” Obviously, we do not know if that is what happened. However, if a collector fails to validate the debt as requested, that is one of the more serious offenses they can commit.

Remember, they need to prove that you owe the debt, that you owe that amount, and that they have the right to collect on the debt. If they fail to do any one of those items, the credit bureaus should remove the account.

Conclusion

Even though PFC has been in business for decades and is certified by some industry organizations, there are a lot of red flags here. The company recently paid a $2.5 million settlement as a result of a data breach. A judge in federal court has already determined that they have violated the FDCPA in at least one instance. Finally, consumers seem to be less than impressed with the service they are providing.

Based on the typical behaviors of consumers in this situation, it seems clear that the best course of action here is almost always going to be to file a dispute.

Whether you are going to dispute directly with PFC or with the credit bureaus, a dispute can often help get the best results here. Do not make the mistake of immediately calling the collector and making a payment without exploring your other options first. You are not obligated to talk to the debt collector on their terms. In fact, it is in your best interest not to.

If you do speak with them, make sure you have a good record of who you spoke to and what was discussed. Ultimately, your goal is going to be to get a complete removal of the collection account from your credit report, not just to pay it.

Take Action Today

Are you on this list of debtors and need help? When it comes to dealing with collection agencies like Professional Finance Company, it is essential to know your rights as a consumer and how to use them to your advantage.

At FightCollections.com, our team of experts will help you dispute errors in your credit report and advocate on your behalf to achieve the best outcome possible for your situation. Contact us today for a free consultation.