Dealing with an Oliphant USA collection on your credit report is a gut punch. Your immediate reaction may be to call the number on the report and settle this as fast as you can.

While that is an understandable response, it is exactly what you should not do. It is exactly what companies like Oliphant USA want you to do. The consumer credit reporting system has a set of rules that dictate what can and cannot be on your credit report, but most people do not learn about those rules until a negative entry appears on their report.

Learning how Oliphant USA and other debt collectors skirt those rules is the first step in protecting yourself from their abuse. What you do in the next few days matters far more than what you owe.

Oliphant USA is a debt collection agency based in Austin, Texas. They buy and collect on outstanding debts that other companies have written off. Oliphant USA operates under several business names, including Oliphant Financial, LLC, and Oliphant Funding, LLC. Their contact information is as follows:

Who is Oliphant USA?

In October 2021, Oliphant USA was sold to investment companies Skypeak Fund I and International Capital Access Group. That is important to remember because these debt collection companies are investment funds. They exist to squeeze as much money as possible out of the debts they buy.

A probe into Oliphant USA reveals a history of regulatory infractions and consumer complaints. The Connecticut Department of Banking issued a consent order to Oliphant Financial, LLC for acting as a consumer collection agency in Connecticut without a license from January 1, 2018, through May 2, 2022. That is more than 4 years of unlicensed debt collection in a single state.

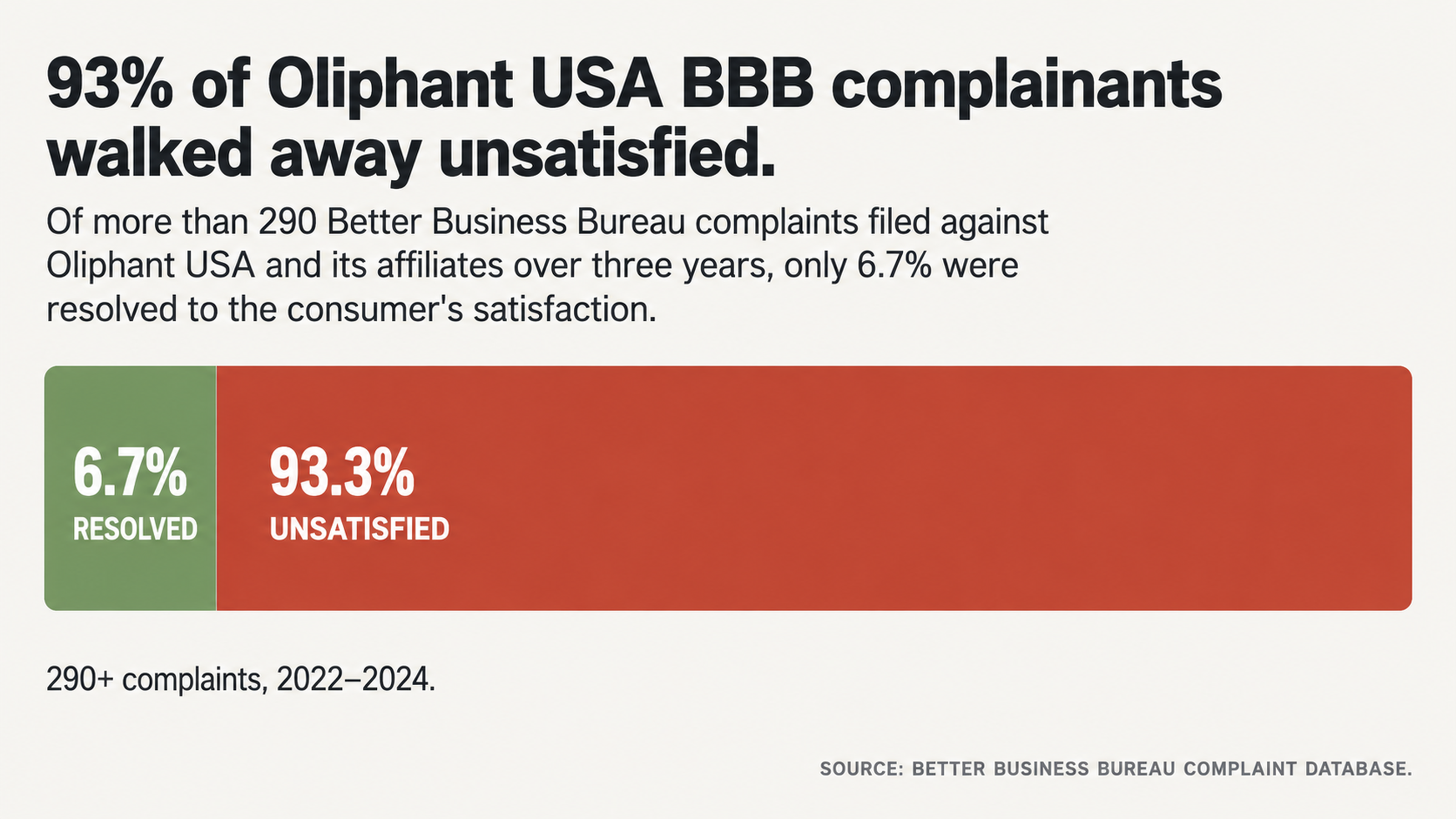

Over the past 3 years, Oliphant USA and related companies have amassed over 290 complaints with the Better Business Bureau. Only 6.7 percent of those complaints were resolved to the satisfaction of the consumer. The remaining 93 percent of complainants found the response from Oliphant USA unsatisfactory.

Oliphant USA has been named in over 130 federal lawsuits regarding its debt collection practices. Multiple class action lawsuits have claimed that the company violated the Fair Debt Collection Practices Act on a systematic level. In at least one California class action, a judge refused Oliphant’s motion compelling arbitration.

Why Do Debt Collectors Want You to Call?

Debt collectors want you to call because they make pennies on the dollar when they buy debts. They have to collect successfully on as many of those debts as they can in order to stay in business. Everything they do is a tactic to get you to pay as much as you can as quickly as you can.

The telephone is their favorite tool because it leaves no paper trail. Once you are on the phone, anything you say can be used to:

Confirm your identity

Confirm your address

Admit that you owe the debt

Restart a statute of limitations clock

One consumer complaint said Oliphant USA made a verbal settlement offer but would not put it in writing. The representative told her the company would send the paperwork after she paid.

The psychology of the call works entirely in favor of the debt collector. They have a script. They have training. They have your file right in front of them. All you have is shock, stress, and no way to prove what they said.

The Urgency Game

Debt collectors use urgency and fear because those emotions push rational thought out of your brain. One of the BBB complaints against Oliphant USA described receiving multiple daily calls. The messages included deceptive claims about “promotional offers” to prompt a return call. The goal is to keep you reacting instead of thinking.

Most consumers’ knee-jerk reaction to a collection call is to pay the debt because it seems like the right thing to do. Once you pay a collection, however, its status changes from unpaid to paid. The derogatory mark remains on your credit report for years to come. Paying for the removal of a derogatory mark rarely results in the promised improvement to your credit score.

Why You Can’t Trust Credit Reports

79 Percent of Credit Reports Are Wrong

A study by U.S. PIRGs found that 79 percent of credit reports contain errors or inaccuracies. That is not a rounding error. That means that most credit reports are wrong. When nearly 4 out of 5 credit reports have some kind of mistake, it is statistically foolish to assume that the Oliphant USA collection on your report is accurate.

Instead of assuming you have to disprove the debt, why not make the debt collector prove that the debt is valid, that they have the paperwork to prove it, and that the debt is legally collectible?

The Lack of Documentation

Debt buyers like Oliphant USA have a problem. When debts are sold from the original creditor to a debt collector, the paperwork frequently does not make the journey. The Texas Court of Appeals dismissed a case brought by Oliphant Financial because the company could not produce the original contract or calculate the correct amount of interest.

Consumer complaints regularly note that when they ask Oliphant USA to validate the debt, representatives tell them they do not have to provide proof. That may be against federal law. Under the Fair Debt Collection Practices Act, a debt collector must verify a debt when a consumer requests validation in writing.

Several of the lawsuits brought against Oliphant USA alleged that the company’s collection letters failed to clearly identify the current owner of the debt. That is a chain-of-title issue, and it is common when dealing with debt buyers.

The Power of Remaining Silent

What Silence Gets You

In a debt collection scenario, silence is golden. Any information you provide to a debt collector can and will be used against you. Any information you refuse to provide means the debt collector must prove their case without your help.

If you communicate in writing, you have a paper trail that protects you. If you communicate by phone, you create an opportunity for miscommunication, manipulation, or misrepresentation.

One consumer complaint included the recording of an Oliphant USA representative who mocked her, misgendered her multiple times, and told her that if she marked the account as disputed he might note it later because he works from home and can do what he wants.

Written Dispute Letters

If you dispute a debt in writing, federal law requires debt collectors to follow certain procedures. The Fair Credit Reporting Act and the Fair Debt Collection Practices Act are dense with strategies, nuances, and technicalities that you probably do not know about.

In February 2025, a consumer filed a lawsuit against Oliphant USA, claiming the company unlawfully updated her credit report tradeline to “in collection” and failed to report that the account was disputed. That is a violation of a very specific federal statute, and it is grounds to file a lawsuit.

Using Documented Infractions as Leverage

A History of Regulatory Infractions

The Connecticut Department of Banking issued a consent order against Oliphant Financial, LLC, for operating as a consumer collection agency in Connecticut without a license. The period of non-compliance stretched from January 1, 2018, through May 2, 2022. That is more than 4 years of illegal debt collection in a single state.

Any consumer contacted by Oliphant USA in Connecticut between 2018 and 2022 may have grounds to dispute not just the debt but the legitimacy of the contact itself. Connecticut can impose fines of up to $100,000 per violation.

Oliphant USA signed the consent order without admitting or denying any violations. That is a standard practice when debt collectors settle claims with regulators. It means Oliphant USA is not admitting anything that could be used against it in future litigation.

Patterns of Class Actions

The class actions against Oliphant USA are telling. They indicate patterns of behavior rather than one-off incidents.

A Wisconsin federal court certified a settlement class in the case of Frankenreiter v. Oliphant Financial, LLC. The court found Oliphant USA had sent defective collection letters to the class members. The letters violated the Fair Debt Collection Practices Act.

In the lawsuit Dombrowski v. Oliphant Financial, LLC, the plaintiff claimed that Oliphant USA’s collection letter did not clearly identify the alleged creditor and confused the relationship between Oliphant USA and the alleged debt in the eyes of the unsophisticated consumer. The plaintiff claimed to have been misled, deceived, and confused by the communication.

When a California appellate court reviewed Fleming v. Oliphant Financial, LLC in 2023, it found that Oliphant USA did not meet its burden of proving the existence of a valid agreement to arbitrate. There was nothing in the record to suggest that the consumer may have agreed to arbitrate the dispute, so the class action could continue.

How to Remove an Oliphant USA Collection from Your Report

You can get a collection deleted from your credit report if the information is inaccurate, erroneous, fraudulent, or if the collector cannot verify it within a reasonable amount of time. The trick is knowing how to navigate the technical requirements for disputing a debt and which pressure points to apply to which collector.

Credit repair specialists understand the minutiae of the FCRA and FDCPA because they have dealt with so many disputes. They know which words trigger verification and which documentation loopholes collectors cannot climb out of.

Oliphant USA has a history of failing to verify debts, operating without a license, and settling class actions. A credit repair specialist would know how to use those failures to your advantage. The company has only a 6.7 percent success rate of resolving BBB complaints in a way that satisfies the consumer. That means 93 percent of the time Oliphant USA does not respond adequately when confronted.

Things to Keep in Mind Before You Proceed

If you try to deal with a debt collector on your own, you are likely to make a mistake. A phone call to ask questions can become an admission. A payment to put the issue behind you can reset the clock on the credit reporting period. A letter that is not properly formatted under federal law will not get the response you need.

The debt collection business relies on consumers not knowing their rights. Debt collectors get paid for the difference between what the law requires of them and what consumers know the law requires of them. The only way to change that is through education or by hiring someone who has already been educated in the FCRA and FDCPA.

What to Do Next

The history of infractions, settlements, and unresolved complaints is enough for you to draw your own conclusions about Oliphant USA. Before you pay or call the company, consider that their history shows a pattern of regulatory infractions, including operating without a license, failing to validate debts, and losing in court because it cannot produce the necessary documentation.

The consumer credit reporting system puts the onus on you to challenge inaccuracies, but it also gives you the tools to succeed if you know how to use them. If almost 4 out of 5 credit reports contain errors, the question is not whether you should dispute the Oliphant USA collection. The question is how you should dispute it.

Right now, you have a collection on your credit report from a company that has a history of violating federal regulations. Do not call Oliphant USA. Do not pay them without knowing how it will affect you. And do not assume you owe them just because they say you do.

FightCollections.com helps consumers fight debt collectors by disputing credit report collections. We understand the specific weaknesses of Oliphant USA and many other debt collectors, and we know how to turn those weaknesses into leverage for our clients. Contact us today for a free consultation, and let us help you understand your situation and develop a plan to address it.

Debt collectors have their playbook. Now it is time for you to have yours.