Have you recently pulled your credit report and found that it contains an account from Ability Recovery Services that you don't recognize? It's not uncommon for debtors to find collection accounts on their credit reports that don't belong to them.

So what can you do to get Ability Recovery Services off your back? Continue reading to learn about this collection agency and the steps you can take to get a legitimate account removed from your credit report or to get Ability Recovery Services to stop harassing you if the account doesn't belong to you.

About Ability Recovery Services

Ability Recovery Services is a debt collection agency based in northeastern Pennsylvania. They collect primarily medical debts, higher education accounts, telecommunications balances, and utility bills. Their contact information is as follows:

The company is a family-owned business and is a member of ACA International, the Association of Credit and Collection Professionals. They have four locations throughout Pennsylvania and collect debts nationwide in all 50 states.

Consumer Complaints Against Ability Recovery Services

There are over 2,000 complaints filed against Ability Recovery Services in the Consumer Financial Protection Bureau (CFPB) database. So if you are experiencing issues with this collection agency, you are not alone.

Over 1,000 of the CFPB complaints filed against the company contain a narrative. We analyzed these complaints to find the most common issues that debtors experienced with the company. The most common issues reported by consumers were:

Credit reporting disputes

Debt verification issues

Problematic communication tactics

Attempts to collect debt that the consumer didn't owe

Allegations of attempting to collect on a debt that the consumer had already paid

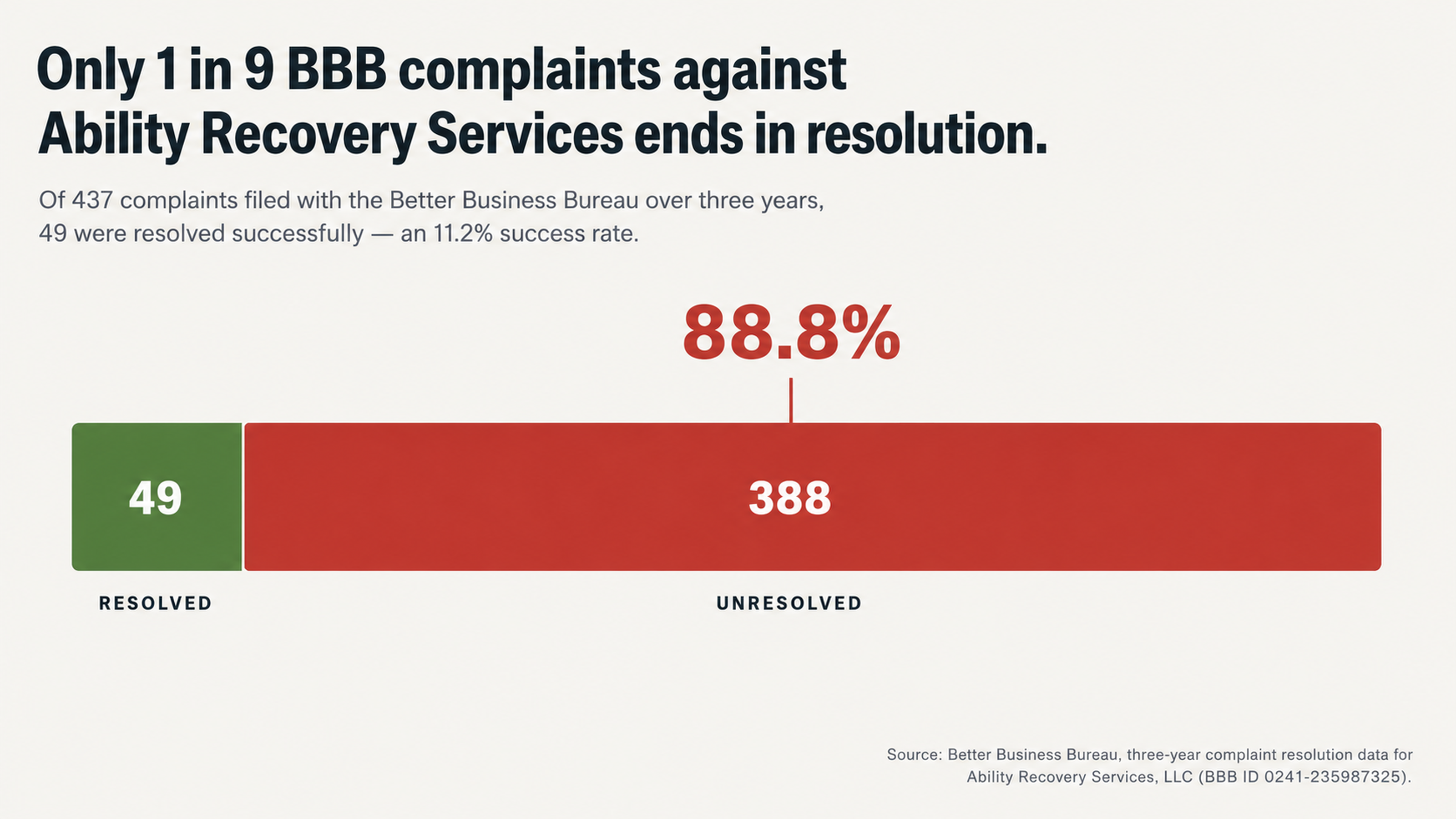

Better Business Bureau Complaints

Over the past three years, there have been 437 complaints filed against Ability Recovery Services with the Better Business Bureau (BBB). Only 49 of these complaints were resolved successfully. This is an 11.2% success rate, meaning that 88.8% of complainants were not satisfied with the company's response to their complaints.

Federal Lawsuits

There have been over 100 lawsuits filed against Ability Recovery Services in federal court alleging violations of federal consumer protection laws.

In August 2021, a default judgement of $21,000 was entered against the company in the case of Aljahmi v. Ability Recovery Services. The consumer was denied a student loan and had to withdraw from nursing school due to damage to her credit report caused by an unsubstantiated debt that the company had failed to investigate properly in response to a dispute letter from the consumer.

Debt Validation

Under federal law, you have the right to send a written request to a debt collection agency asking for it to verify your debt. This is called a debt validation request. When you send a debt validation request to a collection agency, it must stop all collection activities until it provides you with written documentation showing that the debt is valid and that you owe it.

Your Rights Under Federal Law

Federal law provides consumers with many rights and protections from abusive debt collection practices. The primary federal laws that govern the actions of debt collection agencies are the Fair Debt Collection Practices Act (FDCPA) and the Fair Credit Reporting Act (FCRA).

The Fair Debt Collection Practices Act (FDCPA)

The FDCPA is a law that prohibits debt collection agencies from engaging in certain practices when collecting debts. Some examples of prohibited practices include:

Harassing a consumer

Threatening to have a consumer arrested or jailed

Misrepresenting oneself as a government official or attorney when they are not

Consumers have the right under the FDCPA to request that a debt collection agency validate a debt. You must send your request in writing and you must send it to the agency within 30 days of receiving the initial written communication from the agency. During this time, the agency must suspend all collection activities until it sends you written documentation that proves the debt is valid and that you owe it.

Many of the complaints filed against Ability Recovery Services with the CFPB involved alleged violations of the FDCPA. These violations include:

Failure to validate a debt when requested

Failure to mark a debt as disputed on the consumer's credit report

Continuing to contact a consumer after the consumer requests that they cease and desist

Calling a consumer at work after the consumer has requested that they stop doing so

One consumer filed a complaint with the CFPB stating that Ability Recovery Services calls her every day, multiple times a day, and has called her employer as well as her friends and family, despite her request that they communicate with her by mail.

The Fair Credit Reporting Act (FCRA)

The FCRA is a law that governs how credit reporting agencies maintain and update credit reports. One of the protections provided to consumers by the FCRA is the right to dispute information on their credit reports that they believe is inaccurate or incomplete. When you file a dispute with a credit reporting agency, it must conduct an investigation and verify the information. If it cannot verify the information, it must remove the information from your credit report.

Many of the complaints filed against Ability Recovery Services with the CFPB involve credit reporting issues. Some consumers have reported that they discovered collection accounts from Ability Recovery Services on their credit reports even though the company never contacted them prior to placing the accounts on their reports. Other consumers reported that the company removed disputed accounts from their credit reports only to place them back on their reports a few months later.

One consumer reported that Ability Recovery Services was attempting to collect a debt from them that they did not owe. The consumer requested proof of the debt from the company several times, but it only sent them an invoice and not a copy of a letter that showed that the consumer acknowledged that they owed the debt. The consumer stated that they refused to pay for something that they didn't do.

Why You Shouldn't Pay Ability Recovery Services Without Verifying the Debt

If you discover a collection account from Ability Recovery Services on your credit report that you don't recognize, it's important that you don't jump to conclusions and assume that it's your fault for forgetting about the debt. Research by U.S. Public Interest Research Groups found that 79% of credit reports contain either mistakes or serious errors.

If you see an unfamiliar collection account on your credit report, the odds are in your favor that the account contains an error.

Many of the consumer reviews of Ability Recovery Services reflect this reality. The company has a rating of 1.9 stars on WalletHub, where 73% of its reviews are one-star reviews. Many consumers reported being contacted by the company for debts that they don't recognize.

One consumer reported that she contacted the company because she didn't recognize a $2,661 debt that it was attempting to collect from her. The representative she spoke with gave her an incorrect birthdate and told her that the company would mail her a statement. After 30 days, the consumer contacted the original creditor because she still hadn't received a statement. The original creditor informed her that she had never used its services.

If you are unsure whether an unfamiliar collection account on your credit report is valid, requesting debt validation from the collection agency or filing a dispute with the credit reporting agency is the best way to protect yourself from potentially paying a debt that isn't yours or from paying an incorrect balance.

Paying a Collection Account Can Hurt Your Credit

Additionally, you should be aware that paying a collection account can potentially cause it to remain on your credit report longer than if you were to dispute it or request debt validation. When you pay a collection account, it doesn't simply disappear from your credit report. Instead, credit reporting agencies will update the status of the account to reflect that it is paid.

This means that you will still have a collection account on your credit report, but instead of being listed as unpaid, it will be listed as paid. Having a paid collection on your credit report is still very damaging to your credit score.

If you have an unpaid collection account on your credit report and you're considering paying it, you should be aware that it will remain on your report for seven years from the original delinquency date. So if you pay an old collection account, it will still be on your report for the remainder of the seven-year period even though it is paid.

Paying a Collection Account Can Revive the Statute of Limitations

Another reason that you shouldn't pay a collection account without requesting debt validation or filing a dispute is that it could potentially cause you to renew the statute of limitations on the debt.

One of the class action lawsuits filed against Ability Recovery Services in federal court alleged that the company attempted to collect time-barred medical debts from 2012 and offered a 50% settlement without disclosing to the consumer that if they paid the settlement, it would revive the statute of limitations, allowing the creditor to sue them for the full amount of the debt.

Before you pay a collection account, it's important that you verify that it is valid, that you owe it, and that the balance is accurate. Additionally, you should verify how old the debt is and whether it is within the statute of limitations in your state. Paying an old debt that is not within the statute of limitations can potentially revive it and cause the creditor to be able to sue you for the debt.

Understanding The Dispute Process: The Initial Steps

Disputing a debt is about knowing when to share information and what information you should share. You have a right to request proof that the collector can collect the debt. You don't have the obligation to give them information that will help them do so.

Keep a Record

Everything is a record. Keep a copy of every letter you send and receive. Use a log to keep track of every phone call, including the date and time of the call. If the collector breaks a rule in the FDCPA, the information you log is evidence. The $21,000 awarded to the plaintiff in the case against Ability Recovery Services is proof that this works. The judge determined that the company broke the law when it failed to respond to a dispute letter and did not mark the debt as disputed on credit reports.

Your record should include:

Original collection notice

A copy of the dispute letter sent via certified mail with return receipt.

Any response received from the collector.

Screen shots of how the account currently appears on your credit reports.

This trail of paper can help you if you end up in court and serves as a paper trail for your interactions.

The pattern that appears in the BBB complaints and the CFPB complaints and the federal complaints filed against this company is not just a warning sign to other consumers. It is a pattern that shows a systemic problem that you can use to your advantage when you dispute the debt. If the company has a history of not validating debts, then use that history to dispute any debt they are reporting.

What You Say Matters

A collection agency will push you to talk on the phone because this is how they get the information they need. They may use what you say against you to find assets, verify your employment, and to verify your identity. This is why it is always best to communicate through the mail. If you say nothing, they cannot use it against you.

When they try to force you into paying a debt immediately, this is a tactic. They want you to pay before you have a chance to verify the debt. According to complaints filed with the BBB and the CFPB, the company may:

Call you daily.

Make multiple phone calls per day.

Call your employer.

Call your family.

This is all designed to pressure you into paying. It is not because the situation is urgent.

When you do communicate with the company, do it with as few words as possible and always in writing. Ask for verification of the debt. Tell them you are disputing the debt if there is an error. Do not tell them where you work, the name of your bank, or whether you intend to pay the debt. Let the burden of proof stay where it is: with the collector.

What to Expect

The dispute process can be daunting, but it helps to know what to expect. There are rules that the credit reporting agencies must follow when you file a dispute, and the clock starts ticking the minute they receive your dispute.

The Credit Reporting Agency's Role

When you dispute an item on your report, the credit reporting agency must contact the entity who made the report and ask them to verify the information. The entity has 30 days to respond. If they verify the information, it stays on your report. If they fail to respond, the credit reporting agency must delete or modify the information. This is not a suggestion. This is the law.

The word to pay attention to here is "verify." This means the collector cannot simply write back and tell the credit reporting agency that you owe the debt. They must provide proof of the debt and the amount.

Given the fact that only 11.2 percent of BBB complaints filed against Ability Recovery Services resulted in relief for the consumer, it is reasonable to question whether the responses the company provides in response to verification requests are truly adequate.

What happens when the credit reporting agency deletes the item but it reappears on your report?

You have rights. According to the FCRA, if an item that you previously disputed and was removed is re-reported, the credit reporting agency must notify you within five business days. They must also give you the name, address, and phone number of the entity who reported the item. If they re-report the item without notifying you, this is another violation.

Time Is on Your Side

Most debts can only stay on your credit report for seven years. This is true whether you pay it or not. This is true even when you dispute it. In many cases, the statute of limitations has run out, which means the collector cannot file a lawsuit against you even if you owe the debt.

The threat of a lawsuit is a very real one for consumers, but in most cases, it is an idle threat. While it is true that Ability Recovery Services may file a lawsuit against consumers, a review of court records shows the company has been a defendant in more than 100 cases, but they reportedly collect on thousands of debts every year. The likelihood that they will file a lawsuit against you for a debt is relatively low. If you have a low balance debt or if the debt is several years old, the likelihood is even lower.

This doesn't mean you should ignore a collection notice. It means you should not panic and pay a debt because you are afraid a collector will file a lawsuit. In many cases, filing a dispute and allowing the process to unfold is a better strategy than paying immediately.

Bottom Line

Receiving a notice that Ability Recovery Services is now collecting one of your debts is not a reason to panic. It is a reason to understand your rights under a law that was written specifically for consumers like you.

The history of complaints against this company and the low percentage of disputes that get resolved in favor of the consumer are reasons to file a dispute and see what happens. This is also true of the judgments awarded against the company when they break the law.

When a debt collector wants you to panic, you are giving up power. When a debt collector wants you to pay without asking questions, you are giving up power. The law is on your side to help you keep your power and protect your credit report.

Now What?

The dispute process can be complex, and when the stakes are high, it may help to have a professional in your corner. While some consumers navigate the dispute process on their own with success, others find it helpful to work with a partner who has experience with the FCRA and debt collection.

FightCollections.com helps consumers dispute collection accounts and understand their rights when it comes to federal law. If you believe Ability Recovery Services has incorrectly reported information to your credit report and you need help disputing it, contact us for a free consultation.

You don't have to go this alone, and you certainly don't have to pay a debt that may not be valid. You have rights under the law. Learning what those rights are is the first step. Exercising those rights is the next.